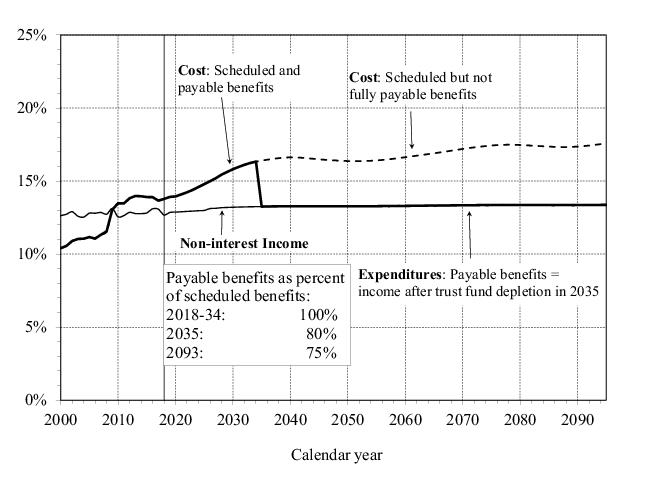

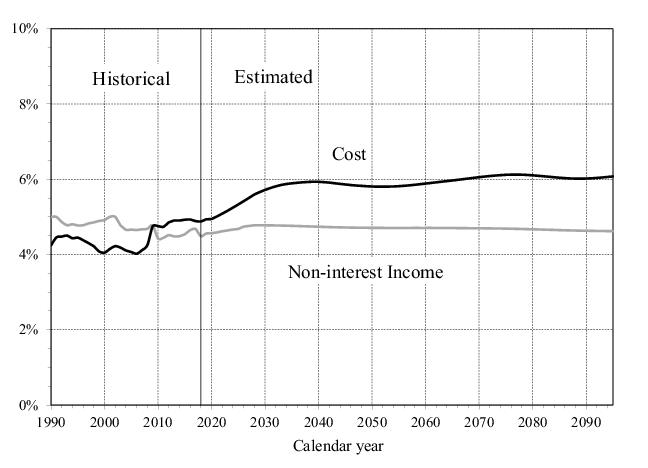

Figure II.D2 illustrates the year-by-year relationship among OASDI income (excluding interest), cost (including scheduled benefits), and expenditures (including payable benefits) for the full 75-year period (2019 through 2093). The figure shows all values as percentages of taxable payroll. Under the intermediate assumptions, demographic factors would by themselves cause the projected cost rate to rise rapidly for the next two decades before leveling off in about 2040. However, the most recent recession temporarily depressed taxable earnings and increased the number of beneficiaries, which in turn sharply, but temporarily, increased the cost rate starting in 2009. From a peak in 2013, the cost rate declined through 2017 under the economic recovery and thereafter returns to a gradually rising trend. The projected income rate is stable at about 13 percent throughout the 75-year period.

Annual OASDI cost has exceeded non-interest income every year beginning with 2010. The Trustees project that cost will continue to exceed non-interest income throughout the 75-year valuation period. Beginning in 2020, cost is projected to exceed total income, and combined OASI and DI Trust Fund reserves diminish until they become depleted in 2035. After trust fund reserve depletion, continuing income is sufficient to support expenditures at a level of 80 percent of program cost for the rest of 2035, declining to 75 percent for 2093. Figure

II.D2 depicts OASDI operations as a combined whole. However, under current law, the differences between scheduled and payable benefits would begin at different times for the program’s two trust funds: in 2034 for OASI and in 2052 for DI.

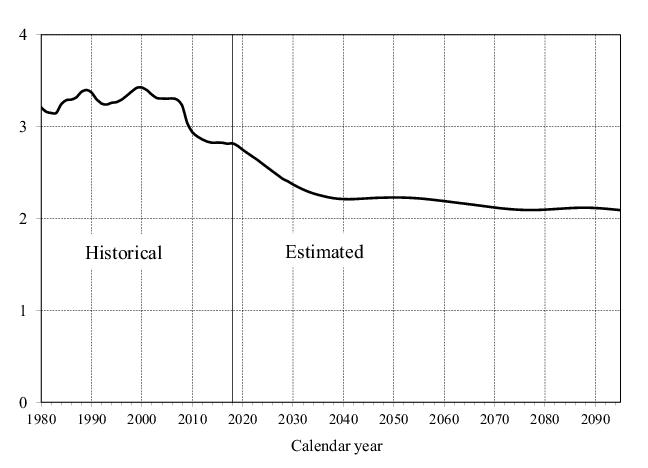

Figure II.D3 shows the estimated number of covered workers per OASDI beneficiary. Figures

II.D2 and

II.D3 illustrate the inverse relationship between cost rates and the number of workers per beneficiary. In particular, the projected future increase in the cost rate reflects a projected decline in the number of covered workers per beneficiary. There were about 2.8 workers for every OASDI beneficiary in 2018. This ratio had been stable, remaining between 3.2 and 3.4 from 1974 through 2008, and has declined since then due to the most recent economic recession and the beginning of the demographic shift that will continue to drive this ratio down over the next 20 years. The ratio of workers to beneficiaries will continue to decline due to this demographic shift , as workers of lower-birth-rate generations replace workers of the baby-boom generation. The ratio of workers to beneficiaries reaches 2.2 by 2035 when the baby-boom generation will have largely retired, and will generally decline very gradually thereafter due to increasing longevity.

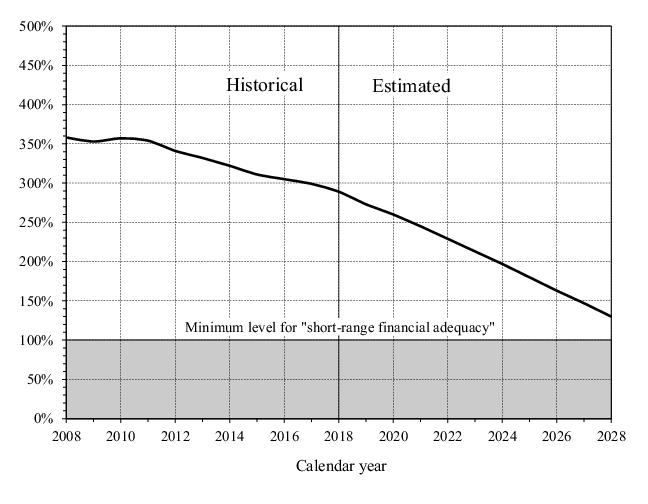

The trust fund ratio is defined as the asset reserves at the beginning of a year expressed as a percentage of the cost during the year. The trust fund ratio thus represents the proportion of a year’s cost which could be paid solely with the reserves at the beginning of the year. Table II.D1 displays the projected maximum trust fund ratios during the long-range period for the OASI, DI, and combined OASI and DI funds. The table also shows the year of maximum projected trust fund ratio during the long-range projection period (2019 through 2093) and the year of trust fund asset reserve depletion. Trust fund ratios for OASI and OASDI are projected to decline from their current levels until reserve depletion. For DI, the trust fund ratio is projected to rise to 91 in 2037, then decline until reserve depletion.

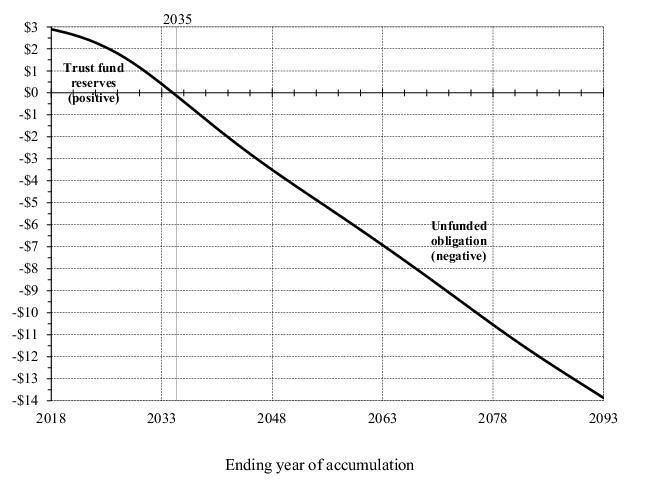

Another way to illustrate the projected financial shortfall of the OASDI program is to examine the cumulative present value of scheduled income less cost. Figure II.D5 shows the present value of cumulative OASDI income less cost from the inception of the program through each of the years from 2018 to 2093. A positive value represents the present value of trust fund reserves at the end of the selected year. A negative value is the unfunded obligation through the selected year. The asset reserves of the combined trust funds were $2.9 trillion at the end of 2018. The combined trust fund reserves decline on a present value basis after 2018, but remain positive through 2034. However, after 2034 this cumulative amount becomes negative, which means that the combined OASI and DI Trust Funds have a net unfunded obligation through each year after 2034. Through the end of 2093, the combined funds have a present-value unfunded obligation of $13.9 trillion. If the assumptions, methods, starting values, and the law had all remained unchanged from last year, the unfunded obligation would have risen to about $13.7 trillion due to the change in the valuation date.

Figures II.D2,

II.D4, and

II.D5 show that the program’s financial condition is worsening at the end of the projection period. Trends in annual balances and cumulative values toward the end of the 75-year period provide an indication of the program’s ability to maintain solvency beyond 75 years. Consideration of summary measures alone for a 75‑year period can lead to incorrect perceptions and to policy prescriptions that do not achieve sustainable solvency.

1

Appendix F presents summary measures over the infinite horizon. The infinite horizon values provide an additional indication of Social Security’s financial condition for the period beginning with the inception of the program and extending indefinitely into the future, but results are subject to much greater uncertainty. Extending the horizon beyond 75 years increases the measured unfunded obligation. Through the infinite horizon, the unfunded obligation, or shortfall, is equivalent to 4.1 percent of future taxable payroll or 1.4 percent of future GDP.

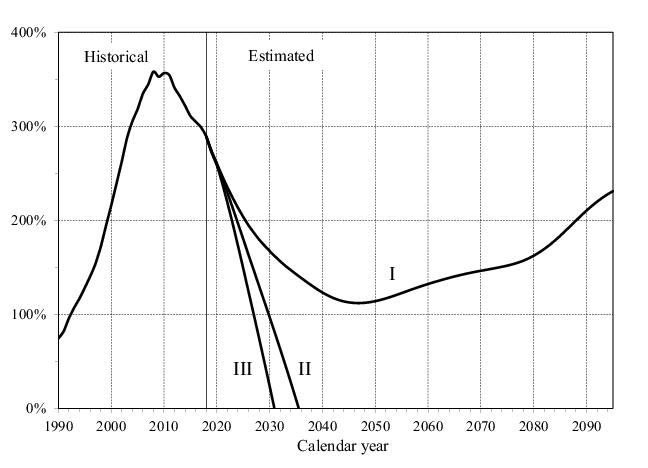

A first approach uses alternative scenarios reflecting low-cost (alternative I) and high-cost (alternative III) sets of assumptions. Figure II.D6 shows the projected trust fund ratios for the combined OASI and DI Trust Funds under the intermediate, low-cost, and high-cost assumptions. The figure indicates that the combined trust funds are projected to become depleted in 2035 under the intermediate alternative, remain above 100 percent of annual cost throughout the projection period under the low-cost alternative, and become depleted in 2030 under the high-cost alternative. The low-cost alternative includes a higher ultimate total fertility rate, slower improvement in mortality, a higher real-wage differential, a higher ultimate real interest rate, a higher ultimate annual change in the CPI, and a lower unemployment rate. The high-cost alternative, in contrast, includes a lower ultimate total fertility rate, more rapid improvement in mortality, a lower real-wage differential, a lower ultimate real interest rate, a lower ultimate annual change in the CPI, and a higher unemployment rate. These alternatives are not intended to suggest that all parameters would be likely to differ from the intermediate values in the specified directions, but are intended to illustrate the effect of clearly defined scenarios that are, on balance, very favorable or unfavorable for the program’s financial status. Actual future costs are unlikely to be as extreme as those portrayed by the low-cost or high-cost projections. The method for constructing the low-cost and high-cost projections does not lend itself to estimating the probability that actual experience will lie within or outside the range they define.

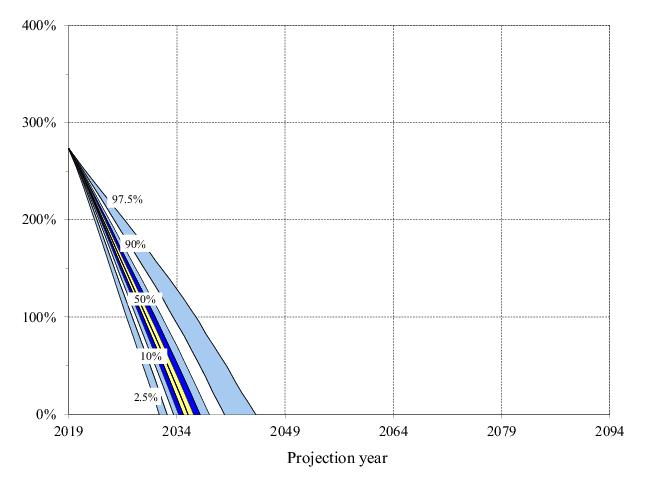

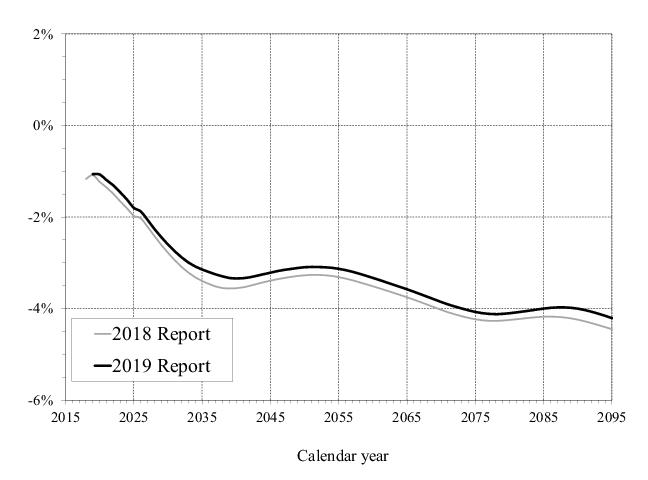

Figure II.D8 compares this year’s projections of annual balances (non-interest income minus cost) to those in last year’s report. The annual balances in this year’s report are higher (less negative) throughout the 75-year projection period. For the full 75-year projection period, the annual balances average 0.18 percentage point higher. See

page 78 for details.