Fifty Years of Social Security

|

||||||||||||||||||

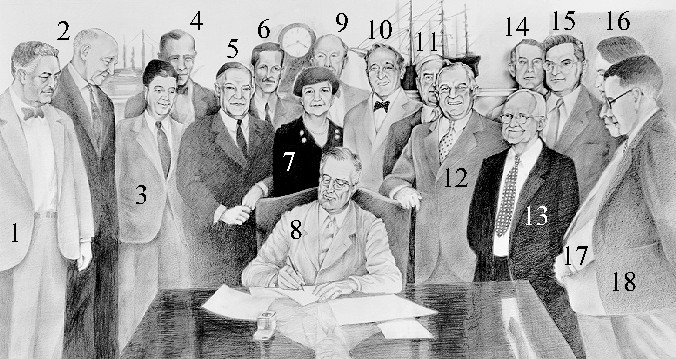

August 14, 1935-- President Roosevelt signs the Social Security Bill into law |

||||||||||||||||||

Fifty Years of Social Security

The author wishes to acknowledge the assistance provided by the following members of the Social Security Administration's Office of Legislative and Regulatory Policy: Peggy S. Fisher, Director, and Timothy K. Evans, and Richard L. Griffiths, staff, of the Division of Retirement and Survivors Benefits.

Today, we celebrate the 50th anniversary of the Federal social insurance program, now known simply as "Social Security," that emerged in 1935 as part of the Nation's response to the plight of its elderly. The Social Security program of the 1980's is the direct descendent of the limited program of contributory old-age benefits enacted in 1935. The program, which today covers virtually all jobs, continues to have certain basic characteristics found in the original program; that is, eligibility is earned through work in covered jobs, participation is generally compulsory, the amount of the benefits is related to covered earnings, the program is intended to provide a base of protection, and benefits are financed primarily through dedicated payroll taxes paid by workers and their employers. Yet, while the program fundamentals have remained the same over 5 decades, much has changed. As American work and life patterns have changed, so too Social Security has been adapted to meet current expectations. The legislative history of the program, described briefly below, shows clearly how Social Security has retained its essential characteristics as it has evolved to keep pace with the times. Foundations of Change By the end of the First World War, a primarily agrarian American society had become a primarily urban, industrialized one. Thus, on the eve of the Great Depression of the 1930's, a larger proportion of the American people were dependent on cash wages for their support than ever before. By 1932, however, unemployment reached 34 percent of the nonagricultural workforce. Between 1929 and 1932, national income dropped by 43 percent, per capita income by 19 percent. By the mid-1930's, the lifetime savings of millions of people had been wiped out. For vast numbers of aged people, and people nearing old age, the loss of their savings brought with it the prospect of living their remaining years in destitution. At the height of the Depression, many old people were literally penniless. One-third to one-half of the aged were dependent on family or friends for support. The poor houses and other relief agencies that existed at the time to assist people who had fallen on hard times were financed mainly from charity and local funds. They could not begin--either financially or conceptually--to respond adequately to the special needs of the aged brought about by the cataclysmic events of the Depression.

Although by 1934, 30 States had responded by providing pensions for the needy aged, total expenditures for State programs for the aged that year were $31 million--an average of $19.74 a month per aged person. As the Depression worsened, benefits to individuals were cut further to enable States to spread available funds among as many people as possible. Various national schemes to provide income to the aged received substantial attention. These included the Townsend Old-Age Revolving Pension Plan and a plan called "Share the Wealth" advanced by Louisiana Senator Huey P. Long. Under the Townsend plan, every American over age 60 was to get a monthly pension, provided he or she did not work and promised to spend the entire payment during the month. Under Long's plan, large personal fortunes would be liquidated to finance (1) pensions for the aged and (2) cash payments to every family sufficient to buy a home, a car, and radio. Due in large part to the public and congressional pressures for some Federal response to the chaotic conditions of the time, in June 1934, a Committee on Economic Security was established by Executive Order of President Franklin Roosevelt. This Cabinet-level Committee, chaired by Frances Perkins, the Secretary of Labor, was given the task of developing constructive, long-term proposals for the prevention of all the major causes of economic insecurity. Given the desperate conditions of the time, the Committee's major attention was focused on programs to protect the unemployed. Yet, amid some controversy about the feasibility and constitutionality of such a plan, there developed from the work of the Committee a proposal for compulsory, contributory old-age insurance, which was ultimately enacted as part of the Social Security Act. The Social Security Act, enacted on August 14, 1935, provided a new federally administered system of social insurance for the aged financed through payroll taxes paid by employees and their employers. Under the system, which applied only to workers in commerce and industry, people would earn retirement benefit eligibility as they worked. With some exceptions, benefits would be related to workers' average covered earnings, and workers could not have earnings and still be eligible for benefits. No benefits were provided for spouses or children, and lump-sum refunds were provided to the estates of workers who died before age 65 or before receiving at least the equivalent in benefits of their taxes plus interest. Collection of payroll taxes began in 1937, and benefit payments were scheduled to begin in 1942. The Early Years Even as the Social Security legislation moved through the Congress in the late winter and spring of 1935, it was acknowledged by many supporters that the old-age program then under consideration was but a first step in providing comprehensive protection for American workers against loss of earnings. President Roosevelt, in signing the Social Security Bill into law noted that "This law, too, represents a cornerstone in a structure which is being built but is by no means complete." In May 1937 the month in which the old-age program survived a crucial constitutional test in the landmark Helvering v. Davis case (in which the employer Social Security payroll tax was found constitutional), the Senate Committee on Finance and the Social Security Board jointly appointed an Advisory Council on Social Security. This outside advisory group, which would be the first of many to study and make recommendations concerning Social Security over the years,* was instructed to study possible ways of making the program more fully effective sooner than contemplated under the 1935 law. (* Appointment of outside advisory bodies has long been institutionalized as a tradition in Social Security policymaking. Numerous advisory bodies have met over the years, and most of the changes made in Social Security have been based in large part on their studies and recommendations. The law has since 1956 required periodic appointment of Advisory Councils.) The Council's fundamental finding was an endorsement of contributory old-age insurance as a way of preventing dependency in old age and thereby reducing reliance on needs-tested assistance. Further, the Council recommended a benefit structure that, in addition to basic benefits for workers, would provide protection for aged wives, widows, and surviving children starting in 1940. Based on the Advisory Council's recommendations and recognizing the heavy dependence of most families on the male wage earner at that time, the Congress, in 1939, enacted legislation that eliminated lump-sum payroll tax refunds and provided benefits for aged wives and widows, young children of retired and deceased workers, young widows caring for a child beneficiary, and dependent parents of retired and deceased workers.

The Committee on Ways and Means of the House of Representatives and the Senate Committee on Finance, in their reports on the 1939 amendments, reasoned that "Under a social-insurance plan the primary purpose is to pay benefits in accordance with the probable needs of the beneficiaries rather than to make payments to the estate of a deceased person regardless of whether or not he leaves dependents." The 1939 legislation also provided a new method of computing benefits, based on average monthly earnings instead of on cumulative wages. The net effect of the 1939 amendments was to increase the annual cost of benefits payable during the early years and to decrease the annual cost of benefits payable during later years. Over the long range, the average annual cost of benefits remained about the same as under prior law. In addition to these changes in benefits, the 1939 amendments made basic changes in the financing of the Social Security program by establishing the Old-Age and Survivors Insurance Trust Fund and by changing the size of the financial reserves held by the program. The provisions of prior law would have resulted in the accumulation of a huge reserve fund over the years, similar to the reserves built up by private pension plans. The new legislation was designed to constrain the accumulation of reserves and, in effect, to move the financing of the program toward "pay-as-you-go" financing. This change in the reserve concept allowed the immediate payment of benefits to retired workers and to their dependents and survivors without increasing Social Security tax rates. This change in financing also permitted a 3-year postponement of the increases in the Social Security tax rate that had been scheduled for 1940. Other recommendations of the 1938 Council that were enacted in 1939 included:

Following implementation of the 1939 amendments, the basic Social Security program was in place. It would remain essentially unchanged over the 1940's as the Nation concentrated its efforts on fighting World War II and toward building a healthy post-war economy. Social Security legislation enacted during these years included further postponement of tax rate increases, minor changes in coverage, and provision for coordinating the survivor benefits payable under the Social Security and Railroad Retirement Acts. Nevertheless, Social Security grew in importance both to the aged and to the economy. The number of beneficiaries grew from about 222,000 at the end of 1940 to over 3 million in 1949. Average monthly benefits grew only slightly, however--from $22.60 for a retired worker in 1940 to $26 at the end of the decade-- less than the rate of inflation.

To help it determine the appropriate ongoing role of social insurance in the Nation's income support system, in 1947, the Senate Committee on Finance named an Advisory Council on Social Security. The findings of this Council formed a major milestone in the history of Social Security by reaffirming in the post-Depression era the social insurance principles established in the 1930's. In the Introduction to its report, the Council said:

With respect to the existing old-age and survivors insurance (OASI) program, the Council was unanimous in finding three major deficiencies: inadequate coverage; unduly restrictive eligibility requirements for older workers; and inadequate benefits. To remedy these problems, the Council recommended a general benefit increase; a doubling of the minimum benefit; provision of benefits for additional dependents and survivors; and extension of coverage beyond the original boundaries of commerce and industry to self-employed workers, farm and domestic workers, Federal civilian employees not under a retirement system, State and local governmental employees, and employees of nonprofit organizations. In order to provide more adequate benefits to workers in these groups who were already middle-aged or older when their jobs were first covered, the Council recommended a "new-start" benefit computation. The 1948 Advisory Council also strongly recommended extension of the social insurance approach to provide a program of cash benefits to the permanently and totally disabled. The program recommended by the Council would pay benefits after a 6-month waiting period only to those with severe and long-lasting disabilities, would provide for expenditures of Social Security funds for rehabilitation of disabled workers, and would terminate benefits to workers who refused to accept physical examinations or rehabilitation. As its first order of business, in 1950, the Congress addressed the erosion in the value of Social Security benefits due to the inflation that had occurred since the inception of the program. The 1950 amendments provided for general benefit increases and increases in the minimum benefit that amounted to an across-the-board increase of about 77 percent. Echoing the view of the 1948 Advisory Council with respect to the ongoing role for the Social Security system, the Senate Committee on Finance said in its report of the 1950 amendments:

To finance this substantial benefit increase and other program improvements, the 1950 amendments increased the contribution and benefit base (the amount of annual wages subject to Social Security taxes and creditable for benefits) from $3,000 to $3,600 and provided a revised schedule of gradually increasing tax rates for employers, employees, and the newly covered self-employed. The new law also repealed a never-used provision which authorized appropriations to the program from general revenues if they were needed. These changes made clear the Congress' rejection of Federal general revenues as a major source of Social Security financing and underscored its view that Social Security should be self-supporting in both the short range and the long range. The Congress also began in 1950 to focus on the coverage deficiencies identified by the 1948 Council. These deficiencies, of course, had previously been recognized by the framers of the original law. At the inception of Social Security, there had been virtually unanimous agreement among supporters of the social insurance concept that, in order to assure adequate protection to the greatest number of workers, coverage should be both compulsory and as nearly universal as possible. Universal, compulsory coverage was also looked upon as the best means of spreading the cost of the program over the largest possible group, and thus avoiding problems of adverse selection and windfall benefits. As noted earlier, the 1935 Act provided compulsory coverage for workers in commerce and industry; initially, about 6 in 10 jobs were covered. Coverage was not extended to other jobs for a number of reasons. Administrative considerations prevented quick development of methods of collecting taxes and providing coverage for the self-employed and for farm workers. Some groups, primarily railroad workers and Federal employees, already had retirement systems. In addition, legal and constitutional concerns involving taxation of States and localities prevented immediate extension of coverage to employees of State and local governments. By 1950, with a decade of experience under the Social Security program behind them, the Congress concluded that many of the obstacles to universal coverage were not as formidable as they had appeared at the beginning. Thus, legislation enacted in 1950 extended coverage to several major categories of workers, including regularly employed farm and domestic workers; non-farm self-employed persons (except professionals); Federal civilian workers; and, at the election of employees and employers, State and local government employees not covered under another retirement program and employees of nonprofit organizations other than ministers. Because many of the workers newly covered under the 1950 amendments were already middle-aged or older, the principle of enabling newly covered older workers to become insured more easily and making their benefits more comparable to those of other covered workers with similar earnings was established. The 1950 amendments included a so-called new-start benefit computation that based benefit amounts on earnings after 1950 and companion provisions for measuring insured status in terms of work after 1950. Four years later (in 1954), another 10 million workers' jobs were covered; in 1956, another million were added. Social Security legislation enacted in 1954 and 1956 extended coverage to (among others) the farm self-employed, certain groups of professional self-employed (generally with the exception of physicians), members of the uniformed services, and State and local government employees under a retirement system, under various conditions. Thus, by the mid-1950's, some 20 years after enactment of Social Security, the protection offered under the program was available to 90 percent of workers. During the 1950's, the Congress also undertook lengthy consideration of another of the 1948 Advisory Council's recommendations--extension of Social Security protection to disabled workers. The House-passed version of the 1950 Social Security Amendments would have provided for a program of disability insurance along the lines recommended by the Council, but the final bill made no such provision. Instead, the 1950 amendments provided for extension of the State-Federal public assistance program to the permanently and totally disabled, as had been urged by a minority of the Advisory Council's members. Later, in 1954, the Congress enacted a disability "freeze" provision. No cash disability benefits were payable under this provision, but workers who were permanently and totally disabled and who also met insured status tests could have their Social Security earnings records frozen as of the date of their disability. Through the "freeze" provision, disabled workers could prevent their retirement benefits from being diluted by many years of no earnings. Other provisions of the 1954 amendments provided for expansion of State vocational rehabilitation programs to address the difficult problem of rehabilitating the severely disabled. Eight years after the 1948 Advisory Council had recommended it, Congress in 1956 established a cash disability insurance program--with benefits first payable in 1957--with essentially the same eligibility requirements passed by the House in 1950. Because of concern about the high costs of a disability program and potential abuse, however, benefits were payable only to workers who were at least 50 years old. These amendments established basic principles under which the disability program continues to operate today:

In 1958, the insured status requirements for disability benefits were relaxed through elimination of the currently insured status requirement and benefits were extended to spouses and children of disabled workers. Two years later, the minimum age requirement for disabled workers was eliminated and a trial work period provision added to encourage disabled workers to return to work. The 1960's By 1960, then, the old-age, survivors, and disability insurance (OASDI) programs were essentially in place as we know them today. Coverage under the program had been made nearly universal, so that virtually all people reaching retirement age in the decades to come would be able to establish benefit eligibility. Over the 1960's, the OASDI programs were refined through legislation to create new categories of beneficiaries, to increase benefits so as to maintain their purchasing power, and to adjust tax rates to assure adequate program financing. Moreover, legislation enacted in 1961 lowered the age of benefit eligibility for men. When the Social Security program was established, benefits were made available to men and women at age 65. The Social Security Amendments of 1956 had provided benefits for women as early as age 62. Benefits received prior to age 65 were reduced to take account of the longer period over which they would be received. The 1961 amendments extended eligibility for reduced benefits to include men. In its examination of the adequacy of Social Security protection for the aged and the disabled, the 1965 Advisory Council came to the conclusion "that cash benefits alone are not enough." In its report, the Council said that:

The Council found in part that, while health care expenditures for the aged were twice as high as those of younger people, the great majority of the aged were neither well-off nor had adequate health insurance. Further, they found that, by the 1960's, the inability of the aged to meet health care costs had become the single most important reason that older people applied for public assistance. Based on these findings, the Council recommended establishment of a program to provide, through a contributory social insurance mechanism, protection against the costs of hospital and related inpatient services for aged and disabled. In order to protect people who were already old, the Council recommended that hospital insurance protection be provided initially without regard to insured status; that is, that people at or near retirement age be grand-fathered into the new program. Even as the Council was meeting, the Congress was actively considering proposals to provide health insurance benefits. In 1965, the Congress passed "Medicare" legislation, which, while it essentially embodied the Advisory Council's recommendations, differed in two major respects. First, in addition to providing protection against hospital costs through a payroll tax financed hospital insurance (HI) program, the plan enacted also included a voluntary program to be financed through monthly premiums and Federal general revenues. This supplementary medical insurance (SMI) program was designed to meet the costs of physicians' services and other outpatient care. Second, only people aged 65 and over, rather than both the aged and disabled, would be eligible for Medicare. (A few years later, in 1972, Medicare protection was extended to people who had been receiving cash disability benefits for 24 months or more.) The Last 15 Years With the advent of Medicare, the body of programs which we refer to today as "Social Security" was complete. Yet, while there have been no major additions to the system over the last 15 years or so, there has been continuing public and congressional reassessment of the ongoing role of Social Security in the Nation's income support structure. For example, the 1975 Advisory Council on Social Security firmly endorsed the basic purposes and principles of the program, noting that:

With respect to the OASDI programs, legislative considerations over these years have focused on three fundamental issues:

As noted earlier, the Congress acted to increase benefits from time to time during the 1950's and 1960's. Nevertheless, there was concern that during the intervals between these ad hoc benefit increases, inflation eroded the purchasing power of benefits. The 1971 Advisory Council examined this issue and recommended that Social Security benefits be adjusted automatically to keep pace with increases in prices. The Council said:

In order to assure that Social Security would provide a consistent level of protection to workers over time as earnings levels rose, and to restrain payroll tax rates as benefit levels increased, the Council further recommended that the contribution and benefit base be increased automatically to reflect earnings growth. In conjunction with these recommendations, the Council also recommended that actuarial cost estimates for the program be based on assumptions that earnings levels would rise over time.* The Council also reaffirmed the view of prior Councils that the program should be financed on a current-cost basis in the near term and advocated frank recognition of this policy in longer-range financial planning. (* Before 1972, actuarial estimates of program costs over the long range were based on level cost assumptions--that is, it was assumed that wage and price levels, as well as benefit levels, would remain unchanged over the 75-year valuation period. As wages did in fact increase, surpluses accumulated that could be and were used to finance benefit increases.) In 1972, the Congress approved legislation that established automatic cost-of-living adjustments (COLA's) in benefits based on price increases as measured by the Consumer Price Index and provided for automatically increasing the maximum amount of earnings covered under the system. Moreover, the payroll tax schedule adopted in 1972 reflected the 1971 Council's recommendations with respect to both the basis for 75-year cost estimates and current-cost financing. Soon after the automatic COLA provision took effect, it became evident that combining the automatic-indexing procedures with the existing benefit table resulted in a computation procedure that, because it took into account both wage and price increases, unduly increased benefits for workers who would retire in the future. This overcompensation resulted in cost projections which showed that the tax rates scheduled in the law would be inadequate to meet the long-range costs of the program. Based on the recommendations of the 1975 Advisory Council, the Congress in 1977 addressed the problems by establishing a new "decoupled" benefit-computation formula for workers becoming newly eligible or dying after 1978. Under the new formula, which replaced the benefit table in the law, initial benefits are increased to reflect increases in average wages before workers reach retirement age, and the purchasing power of benefits is guaranteed after retirement through cost-of-living increases. At the time that the 1977 amendments were enacted, it was thought that, due to the lower long-range costs resulting from the new benefit formula, changes the Congress made in the tax rate schedule would be adequate to finance benefit payments well into the next century. However, over the next few years, the Nation experienced a period of spiraling inflation and high unemployment along with low or negative real wage growth. These worse-than-expected economic conditions created a two-pronged drain on Social Security in the short term.

In addition, new long-range projections showed that the decline in the birth rate and the likelihood of increased life expectancy would both have negative effects on Social Security; in the 21st century, fewer workers would be paying taxes and retirees would be receiving benefits longer. Due to these problems, it soon became clear that without significant further congressional action, the OASI Trust Fund would be unable to pay benefits on time by some point in the 1980's. Thus, in December 1981, President Reagan announced the formation of the National Commission on Social Security Reform (NCSSR) "to work with the President and the Congress to reach two specific goals: propose realistic, long-term reform to put social security back on a sound financial footing and forge a working bipartisan consensus so that the necessary reforms will be passed into law." The NCSSR reported on January 20, 1983. Based on the recommendations of the NCSSR, the Congress enacted the so-called "bipartisan compromise" 1983 amendments. This package of provisions was designed to resolve the financing crisis by sharing the burden among affected groups, present and future. Among the major provisions of the 1983 legislation that became effective in the near term were:

In the long range, in recognition of improvements in longevity, the 1983 amendments provided for gradually increasing the age of eligibility for unreduced retirement benefits. Workers born after 1937 will be the first to be affected by this change; the provision will be fully effective for workers born after 1959, for whom unreduced benefits will be available at age 67. Benefits will continue to be available at age 62, but the reduction in benefits at age 62 will increase as the age of eligibility for unreduced benefits increases. As a result of enactment of the 1983 legislation, OASDI benefits can be paid on time in the short run and well into the next century on the basis of even the most pessimistic economic and demographic assumptions used by the Social Security Trustees in making projections. During the 1990's, current projections show, substantial excesses of income over outgo will replenish program reserves and build up substantial trust funds. After the turn of the century, program costs will rise substantially as the baby boom generation reaches retirement age, and use of trust fund assets will be necessary. With the enactment of the 1983 amendments, which assured the soundness of the Social Security system both through the 1980's and well into the 21st century, the Congress once again reaffirmed its commitment to the use of the social insurance mechanism as the Nation's first line of defense against dependency in old age, disability, or upon the death of a worker. During the past decade and a half, the disability insurance program has also undergone substantial change. During the early 1970's, the disability insurance (DI) program began to experience tremendous growth. As the decade unfolded, it became clear that continuing rapid growth in the DI program was beginning to pose a serious threat to the DI Trust Fund. Studies aimed at discovering the causes of the unexpected growth in the disability program suggested that (1) the beneficiary rolls included many ineligibles, and (2) the program structure tended to discourage people who might be able to return to work from doing so. The Social Security Disability Amendments of 1980 included a limit on monthly family disability benefits, additional work incentive provisions, and administrative improvements, including mandatory reviews, at least once every 3 years, of the continuing eligibility of disabled beneficiaries whose disabilities are not necessarily permanent. On the basis of these amendments, the financial solvency of the DI Trust Fund was restored, and, in fact, the trust fund was projected to increase rapidly after 1981. Shortly after implementation of the 1980 amendments, however, the periodic review provision began to be criticized by the public and Congress. Although, beginning in 1982, the Social Security Administration and the Department of Health and Human Services made many administrative changes to deal with these criticisms, public and congressional attention remained fixed on the DI program, as advocacy groups for the disabled petitioned Congress for legislative relief. Throughout 1982 and 1983, amidst great controversy, the Congress considered a variety of reforms to mitigate the effects of the periodic review process. These efforts culminated in the enactment of the Social Security Disability Benefits Reform Act of 1984. The major provisions are mandatory application of a medical improvement standard in continuing disability reviews, continuation of disability benefit payments during appeal of termination decisions, and a moratorium on reviews of cases involving mental impairments pending development of revised review criteria. Conclusion Today, 37 million people get Social Security benefits of more than $15 billion a month; OASDI benefits this year will total $188 billion. In 1985, about 122 million people will work in employment covered under Social Security, which applies today to 95 percent of all jobs in our economy. As a Nation, we can take particular pride in having made the Social Security program the most successful domestic program in our history. Over the years, Social Security has been a vital contributor to the security of virtually all Americans. Today, 50 years after its inception, it remains the foundation of well-being for us in our later years or if we are disabled and for our families if we die before retirement.

|

||||||||||||||||||