1948 Advisory Council

1948 Advisory Council

Report--

RECOMMENDATIONS ON COVERAGE 1. Self-Employment Self-employed persons such as business and professional people, farmers, and others who work on their own account should be brought under coverage of the old-age and survivors insurance system. Their contributions should be payable on their net income from self-employment, and their contribution rate should be 1.5 times the rate payable by employees. Persons who earn very low incomes from self-employment should for the present remain excluded The self-employed--business and professional people, farmers, and others who work on their own account--represent more than one-third of all persons in jobs now excluded from coverage and constitute by far the largest single group denied the protection of the system. They include about 6 million persons in urban self-employment and perhaps 5 million farmers, though the number of individuals actively engaged in farm operation as a business is probably only about 3.5 million. {2}

The fact that almost all full-time and a large proportion of part-time self-employed persons have for the last few years been required to file income-tax returns has radically changed the outlook for extending coverage to this group. It has been demonstrated that income reports can be obtained from the great majority of the self-employed, and it is now apparent that the coverage of the insurance system can be extended to them by tying in a self-reporting system for social insurance with the income tax. Certain items now reported for income-tax purposes can be used as the contribution base for old-age and survivors insurance and entered on a social-security report form. In the main, these items are net income from a business, profession, or farm (schedule C of the Federal income-tax return), and from partnerships, syndicates, etc. (schedule E). If the contribution base for the self-employed is to be strictly comparable to that for the groups now covered, only the net income from self-employment attributable to personal services should be taxable. We believe, however, that this refinement would be administratively impossible. The contribution base for the self-employed can readily exclude certain types of income which are obviously not work-connected, such as dividends, interest, annuities, capital gains and losses, and some types such as rental income from real property that largely arise from capital investment. Each dollar of income from typical self-employment such as retail trade or a profession or farming, however, is income derived partly from personal services and partly from capital investment, combined in such a way as to make any separation virtually impossible. For many persons with relatively high income from a business, profession, or farming, the failure to make the distinction between income from personal services and income from investment will be of little significance, since that part of their income (the first $4,200 a year of net income) on which they will pay contributions may be presumed to be derived from personal services. Self-employed persons with lower incomes who yet have substantial capital invested in their business, however, will get higher benefits and pay more in contributions than they would if it were possible to tax only their income from personal services. One of the reasons for our recommending that self-employed persons contribute at a rate of 1.5 times the employee-contribution rate rather than at the combined rate for employer and employee is the fact that some of them will be paying on income from capital investment as well as on income from personal services. Moreover, if they were required to pay twice the normal employee rate, the high-income self-employed persons who contributed over a long period might be "overcharged" for their coverage in relation to what they would have to pay for comparable protection under private insurance. The later retirement age which characterizes the self-employed will lengthen their contribution period; reduce the number of years they receive retirement benefits, and result in savings to the trust fund. As a reasonable compromise, we recommend that the self-employed person--who is at once his own employer and employee--should contribute at 1.5 times the employee rate. The Council believes that, at the outset, extension of coverage to the self-employed should be limited to those at income levels to which the requirement for filing Federal income-tax returns has applied, i.e., those with gross annual incomes of at least $500. We therefore recommend exclusion of those whose self-employment yields gross income of less than $500 or a net income of less than $200. Setting a minimum net income for coverage in addition to a minimum gross income will prevent a large volume of returns from persons who earn so little from self-employment that they could not qualify for benefits. This exclusion will avoid reporting with respect to inconsequential amounts of income and will avoid collecting contributions at an expense out of all proportion to the benefits afforded. We advocate limiting coverage to those who have been required to file income-tax returns in the past. The coverage of the old-age and survivors insurance system should not vary with changes in the income-tax exemption. The Treasury Department should require returns for social-security purposes from anyone who has a gross income of $500 or more and net income of at least $200, regardless of changes in income-tax requirements. The application of a retirement test for the self-employed presents special and difficult problems. This is one of the reasons for the recommendation in proposal 19 that benefits be paid at age 70 or over without reduction for earnings. Since many self-employed persons remain at work until at or near age 70, the application of the retirement test only to beneficiaries under that age will avoid the need to make many of the more difficult administrative determinations connected with such a test. The work clause for those between 65 and 70 will, of course, have to be modified for the self-employed in view of the fact that their income will be reported annually.

2. Farm Workers Coverage of the old-age and survivors insurance system should be extended to farm employees During the course of a year about 3.5 million agricultural workers are excluded from old-age and survivors insurance. The social desirability of extending coverage to these workers has long been a matter of common agreement, and it is now evident that administrative considerations no longer constitute an important barrier to their receiving the protection of the system. The Treasury Department and the Social Security Administration have developed plans which the Council believes are workable, although reporting problems may be difficult in the early years. The Treasury Department in cooperation with the Social Security Administration should be left free to select the method of collecting contributions for these workers. Although we believe that either the stamp system or some modification of the present reporting plan would be practicable, we believe that it would be a mistake at this point to stipulate the exact method to be used and thus preclude further study by the agencies concerned. Wages credited toward benefits should include wages-in-kind, when substantial. Without credits for wages-in-kind, many farm workers would be ineligible for benefits, and the benefit amounts for which many others could qualify would be very small. Although evaluating wages-in-kind may prove difficult at the outset, the same type of problem is now being met satisfactorily for groups covered under the present system. Wage credits of workers in restaurants, hotels, and cafeterias and of maritime workers' building superintendents, and resident managers, among others, already include wages-in-kind. Minimum presumptive schedules setting the value of the more important types of wages-in-kind, such as regular meals and lodging, might be of assistance to farm workers and their employers in reporting wages. Inconsequential facilities or privileges, which might create a reporting nuisance out of all proportion to their significance, should be excluded.

3. Household Workers Coverage of the old-age and survivors insurance system should be extended to household workers The 2.5 million persons who work in household employment during the course of a year should be covered under old-age and survivors insurance. They need social insurance protection fully as much as does any other group, and the Council believes that it is now administratively feasible to extend protection to them. Though there was ample reason at the outset to postpone undertaking the special problems of including household workers in the system, the administrative agencies are now in a position to deal adequately with these problems. A strong argument for the delay was the difficulty anticipated in collecting wage reports and contributions from the employers of domestic workers. Since employers may be expected to outnumber employees in this area, the relatively high costs and administrative problems generally associated with obtaining reports from small employers will be heavily concentrated here. The Social Security Administration and the Treasury Department, however, have now had 11 years of experience in collecting wage reports and contributions from small employers, and the administrative machinery of the insurance system functions satisfactorily for these small establishments. In the first quarter of 1946, for example, employers with only one employee represented one-fourth of the total number who reported for purposes of old-age and survivors insurance. In the early years of coverage for household workers, some difficulties may arise from delinquency in the payment of contributions and from incomplete understanding of the program by household workers and their employers. We believe, however, that these problems can be solved fully as effectively and quickly as were the very considerable problems met when the present program was started. As we indicated with respect to farm workers, we believe that, for household workers, substantial wages-in-kind in the form of meals and lodging should be reported and recorded as wage credits, but that wages-in-kind of relatively small value should be disregarded. As in the case of farm workers, also, the administrative agencies concerned should be left free to decide on the methods to be used for collecting wage information and contributions. 4. Employees of Nonprofit Institutions Employment for non~profit institutions now excluded from coverage under the old-age and survivors insurance program should be brought under the program, except that clergymen and members of religious orders should continue to be excluded {3} {3} Two members of the Council favor extension of coverage to the nonprofit group on an elective basis for reasons given in appendix I-E. Approximately a million employees of nonprofit organizations are at present denied the protection of the old-age and survivors insurance program. Almost half are in the service of charitable organizations, one-fourth are in educational institutions, and another fourth work in religious institutions. These employees include not only professional persons such as nurses, teachers, and clergymen, but also office workers, laboratory assistants, janitors, and maids. The extension of coverage to employees of nonprofit organizations presents no administrative difficulties and the need for old-age and survivors insurance protection of these workers and their families is as great as for workers who are now covered. Especially when they work in nonprofessional jobs, the tasks and earnings of employees of nonprofit organizations, as well as the extent to which they move from one job to another, are equally characteristic of industrial and commercial workers. Probably not more than two-fifths of the employees of nonprofit organizations are covered by any formal retirement plan and very few of such plans extend protection to survivors. Moreover, in general, the right to pensions from the private plans is contingent on long periods of service, hence, persons who transfer from one nonprofit organization to another or between nonprofit and other organizations, may forfeit all retirement rights. Although many clergymen are covered by retirement programs, in some denominations the lower-paid clergymen do not participate, while benefits for those who do are often inadequate; more serious, however, is the fact that few lay employees of churches have any assurance of economic security in their old age through staff pension plans. Not more than half the college teachers of the Nation actually participate in retirement systems, and in private colleges most such systems do not cover non-teaching personnel. Coverage under old-age and survivors insurance can and should be effected for teachers, employees of charitable and scientific organizations, and lay employees of churches, without impairing any of the rights which individuals may have built up under private systems. Leaders of religious, charitable, scientific, and educational organizations apparently agree on the desirability of providing protection under old-age and survivors insurance for employees of these institutions. Some, however, have feared that an extension of the compulsory insurance system to employment for religious institutions might impair religious freedom by undermining the principle of the separation of church and state. Others evidently feel that a tax on employers under the Federal Insurance Contributions Act would tend to weaken the traditional tax-exempt status of such institutions. The members of the Council are unanimous in believing that freedom of religion should be protected, but we are convinced that a tax on employment--a function which employers in the nonprofit area have in common with all others--for the special purpose of giving equal social insurance protection to all employees would in no way imply or lead to Government control over the performance of the religious function. To make it absolutely clear that the legislation is not concerned with the performance of religious duties, we recommend that persons directly engaged in religious duties, such as clergymen and members of religious orders, remain exempt from coverage under the program. Our recommendation would extend coverage only to lay personnel who perform services which are secular in character. We also believe that public encouragement of religious, charitable, scientific, and educational enterprise should be continued through preservation of the traditional tax-exempt status of such institutions. That encouragement, however, would be better expressed, we believe, by extending social insurance protection to their employees than by continuing to deny it. Employers in the nonprofit field are at a considerable disadvantage in the labor market because they cannot offer retirement and survivorship protection, hence, coverage exclusion handicaps these organizations and fails to promote their services to the community. Religious, charitable, scientific, and educational organizations, which have been traditionally exempt from taxation on income and property dedicated to the purposes which the community wishes to promote, can and should continue to enjoy their traditional tax exemption when the old-age and survivors insurance program is extended to their employees. It has long been customary to require such institutions to pay certain types of special assessments for property improvement, to pay Federal excise taxes, and in some States to pay the local and State taxes on commodities which they use. Even in some States with exclusive State funds, they have been required to carry workmen's compensation insurance. The use of Government compulsion in connection with these special taxes and levies has not led to taxation on the property and general income of these institutions. Moreover, many organizations such as trade-unions, trade associations, fraternal and beneficial organizations, and the like, which are exempt from the Federal income tax and certain other taxes, pay the old-age and survivors insurance contribution without appearing to be in danger of losing their exemptions under other laws. Old-age and survivors insurance levies a special-purpose tax on the function of employment. The proceeds are automatically appropriated to a trust fund dedicated to benefits for those who have contributed. It has always been clear that it is a special kind of tax which should not serve as a precedent for other forms of taxation any more than would a special assessment levied by a local government. We believe, however, that Congress should indicate its intent that the taxation of nonprofit organizations for old-age and survivors insurance in no way implies a departure from the principle of promoting the function of these organizations through tax exemption, and that a major reason for extending protection to this area of employment is to assist these institutions in fulfilling their purpose. 5. Federal Civilian Employees Note.--The enactment of Public Law 426 by the Eightieth Congress has strengthened and improved the Civil Service Retirement Act. Some 500,000 Federal workers {4} remain outside the coverage of any retirement system, however, and neither retirement nor survivorship protection is afforded Federal employees with less than 5 years of service. Estimates developed from prewar employment figures indicate that, in general, only about 60 percent of all persons entering Federal service remain for 5 years or more. {4} This figure includes an unknown number of foreign nationals. Persons who leave Federal service after having been employed for as much as 5 years but less than 20 years may elect to withdraw their contributions instead of accepting a deferred annuity. When they so elect, they lose all retirement protection under the Civil Service Retirement Act. Whatever survivorship protection an individual may have acquired under the civil-service plan lapses as soon as he leaves the Federal service. Old-age and survivors insurance coverage should be extended immediately to the employees of the Federal Government and its instrumentalities who are now excluded from the civil-service retirement system. As a temporary measure designed to give protection to the short-term Government worker, the wage credits of all those who die or leave Federal employment with less than 5 years' service should be transferred to old-age and survivors insurance. The Congress should direct the Social Security Administration and the agencies administering the various Federal retirement programs to develop a permanent plan for extending old-age and survivors insurance to all Federal civilian employees, whereby the benefits and contributions of the Federal retirement systems would supplement the protection of old-age and survivors insurance and provide combined benefits at least equal to those now payable under special retirement systems The Advisory Council believes that the civil-service retirement system--which now covers about 1.5 million workers--should be maintained as a supplementary retirement system because of its importance in furthering the efficient conduct of the business of government. The civil-service retirement system performs the function of a private staff-pension plan. For this function to be performed successfully and for the Government to meet the obligations created by its compulsory retirement of its employees, benefits larger than those payable under the general old-age and survivors insurance system must be provided. Hence, nothing should be done to weaken the Federal civil-service retirement system. We are convinced, however, that extension of the coverage of old-age and survivors insurance to all Federal civilian employees (including those, other than foreign nationals, who are employed outside the United States) would strengthen rather than weaken the civil-service system. Such extension would remedy three major defects in the protection now afforded Federal employees--the lack of adequate survivorship protection, the lack of continuity of protection for those who move in and out of Government service, and the exclusion of many Federal workers from any Government retirement system. The survivor benefits provided by Public Law 426 (80th Cong., 2d sess.), while of considerable value for long-term workers, are quite inadequate for the survivors of workers with relatively short periods of Federal service. First, no monthly survivor benefits are payable unless the employee has had at least 5 years' service. Second, survivor benefits are very small if the employee has had only a short period of service and annual wages at about the current average. Thus, the widow of a Federal employee who had 5 years of service and an average annual salary of $3,000 would receive a monthly payment of about $11, and his child's monthly payment would be about $6. The Federal employee, like all others, needs survivorship protection based on the insurance principle of full protection for the young worker as well as for the older age groups. As noted above, persons who leave Federal employment with less than 5 years' service receive only a refund of their contributions to the civil-service retirement system, while those who leave after 5 years but before 20 years of service have the option of receiving either a refund of their contributions or a deferred annuity. Almost 20 percent of all Federal employees leave in their first year of Government employment and another 10 percent leave during the second year. According to data developed from prewar histories, only about one-third stay on to retirement. The time spent in Federal employment, moreover, reduces the possibility of obtaining adequate protection under old-age and survivors insurance. Extension of old-age and survivors insurance coverage to Federal employment would provide continuing protection for these short-time workers as well as for career employees. The 500,000 persons who are now working for the Federal Government in civilian jobs and who are not covered by any Federal retirement program represent nearly one-fourth of the total of all Federal employees. The group includes some postal workers, and certain temporary, part-time, contract, and piecework employees. Pending the development of a suitable plan, recommended by the agencies concerned, for extending old-age and survivors insurance coverage to all employees (except foreign nationals) and congressional action on such general extension, coverage should be extended immediately to the employees of the Federal Government and its instrumentalities who are not now covered under any system. Old-age and survivors insurance coverage would be particularly valuable to many employees in this group because they are temporary or part-time workers who may ordinarily work in employment now covered under old-age and survivors insurance. In addition, we advocate some immediate provision for the employee whose Federal service is too short to furnish protection under the civil-service retirement system, even though he is covered by that system. Accordingly, as a temporary measure, pending complete extension of coverage to all Federal workers, we recommend that-- when separated from Federal service, whether by death, resignation, or dismissal before having served for 5 years--the Federal employee receive appropriate wage credits under old-age and survivors insurance for his Federal service. When the employee leaves the service, he should receive a refund of his contributions to the civil-service retirement system, less an amount equal to the employee contribution which he would have paid on his wage credits if he had been contributing toward old-age and survivors insurance. The latter amount should be transferred to the Federal Old-Age and Survivors Insurance Trust Fund, and this transfer of credits and contributions should be irrevocable. In addition, the Federal Government, through an annual appropriation by the Congress, should pay the old-age and survivors insurance trust fund the employer's share of the contributions which would have been collected for old-age and survivors insurance with respect to the wage credits given for Federal service. To be eligible for full civil-service retirement benefits if he later returns to Federal service, the employee should be required, after completing 5 years of total service, to redeposit the full amount of his previous contributions to the civil service retirement and disability fund. In some such instances, he will thus have duplicate credits for the same period of service. In a temporary plan, however, this duplication does not seem serious, since the employee will have paid for his credits under each program. When the employee dies during his first 5 years of service, the old-age and survivors insurance trust fund should be reimbursed for the cost of that part of the benefits payable to his survivors which is attributable to his civil-service wages. This reimbursement should be based on recommendations by the Civil Service Commission and Social Security Administration as to the most equitable method for such reimbursement. This proposal falls short of an adequate permanent solution to the problem. It does nothing, for example, for persons who, on leaving Federal service after 5 years, elect to take an immediate refund rather than a deferred annuity; it also fails to provide survivorship protection for those who leave Federal service. A temporary measure obviously cannot avoid all possible situations in which hardship may develop. The measures we propose are a stopgap to prevent the most glaring anomalies, until such time as complete old-age and survivors insurance coverage of Federal employees, with appropriate supplementation by the civil-service retirement system, can be adopted.

6. Railroad Employees Note.--Like the civil-service retirement system, the Railroad Retirement Act has recently been substantially revised. The amendments of 1946 (Public Law 572, 79th Cong.) established survivorship protection for railroad workers based on a combination of their earnings in the railroad industry and in employment covered by old-age and survivors insurance, under eligibility and benefit provisions closely resembling those of old-age and survivors insurance. No such coordination, however, is provided for retirement protection under the two programs, hence workers with earnings from both railroad employment and employment covered by old-age and survivors insurance, but with only a relatively few years in either one, may receive considerably lower retirement benefit in relation to their contributions than they would if all their employment had been covered under one program or the other. The extent of shifting between the two employment areas is substantial. The Congress should direct the Social Security Administration and the Railroad Retirement Board to undertake a study to determine the most practicable and equitable method of making the railroad retirement system supplementary to the basic old-age and survivors insurance program. Benefits and contributions of the railroad retirement system should be adjusted to supplement the basic protection afforded by old-age and survivors insurance, so that the combined protection of the two programs would at least equal that under the Railroad Retirement Act The railroad retirement system developed out of special conditions on the railroads and has a distinctive history. It grew out of, and superseded, many private pension plans which had existed in the railroad industry, and through its adoption the protection which formerly had been afforded to only a limited number of railroad workers was made available to all. The protection against old age and premature death provided by the railroad retirement program is generally more liberal than that provided under old-age and survivors insurance, and long-service railroad workers are insured against the risk of permanent and total disability. Moreover, the contributions of the railroad program are considerably larger than those now payable under old-age and survivors insurance. While the railroad program provides adequately for the workers who remain in the industry during their entire working lifetimes, inadequate protection is given in some instances to those who move between railroad and other employment. That this movement is very large is indicated by a comparison of the total number of workers employed by the railroads during a year with the average number at work at any one time. While average railroad employment in 1945 was nearly 1.7 million, about 3.1 million individuals had some railroad earnings during the year. Thus, for every 100 railroad employees working at a given time in 1945, 183 acquired railroad-retirement credits in that year; in 1940 this ratio was 100 to 140. During 1937-46 probably about 4,000,000 persons had wage credits under both railroad retirement and old-age and survivors insurance; this group represents more than half the workers (approximately 7,000,000) with wage credits under the Railroad Retirement Act during the 10-year period. Extension of old-age and survivors insurance to railroad employees would prevent losses in protection that may now result from these shifts in employment. It would also prevent the disproportionately high total of benefits which may result from shifting employment in some cases. Such cases arise when a higher-paid worker employed for the most part in the railroad industry, and so eligible for substantial railroad benefits, acquires enough credit under old-age and survivors insurance to qualify for benefits under that program also and receives the advantage of the weighting in the benefit formula of the latter program which is intended to favor lower-paid workers. The railroad-retirement program gives railroad workers vested rights in retirement benefits regardless of the length of time they are employed. Thus, unlike Government employees, employees of nonprofit organizations, and members of the armed forces, railroad workers are certain to qualify for at least some benefits under at least one retirement system. Nevertheless, we believe that employees who spend all or part of their working lives in the railroad industry should have all their employment credited under the old-age and survivors insurance program; otherwise, some railroad workers will contribute substantially toward that program without qualifying for its benefits. Furthermore, during the early years of the old-age and survivors insurance program, some persons who work for only a few years in railroad employment will have less in combined protection than they would if they had been under old-age and survivors insurance continuously. If the basic protection of old-age and survivors insurance were extended to railroad employment, supplementary benefits under the railroad program would be needed to prevent railroad workers from receiving less retirement and disability protection than is now available to them. If the survivor benefits of old-age and survivors insurance are increased as we propose, they would be higher than survivors benefits under the present Railroad Retirement Act. We believe that the basic differences between the structures of the retirement benefits under old-age and survivors insurance and the Railroad Retirement Act preclude any coordination short of extending old-age and survivors insurance coverage to railroad workers and making the Railroad Retirement Act a supplementary program. In our opinion, a satisfactory plan can be developed for extending old-age and survivors insurance to all railroad employees and thus strengthening the protection now afforded railroad workers. A report on such a plan should be made to Congress at the earliest practicable date. Extension of old-age and survivors insurance to railroad employees and making the railroad system supplementary to old-age and survivors insurance would result in lower pay-roll contributions by railroad workers and their employers for the same protection as at present if, as we propose, old-age and survivors insurance is ultimately financed in part by appropriations from general revenues. 7. Members of the Armed Forces Old-age and survivors insurance coverage should be extended to members of the armed forces, including those stationed outside the United States Although the career serviceman is eligible for retirement benefits after 20 years of service, the person who spends a shorter period in the armed forces is seriously handicapped by the fact that his military or naval service is not covered under old-age and survivors insurance. At his death his survivors may not be eligible for any benefits, since protection of peacetime servicemen under the programs for veterans ceases immediately on discharge from service; while if he lives to retirement age, he may fail to be eligible for retirement benefits under either old-age and survivors insurance or one of the special retirement plans. In other cases, benefits will be payable only under old-age and survivors insurance and at a greatly reduced rate because of the time spent in the armed forces. Extension of old-age and survivors insurance to the armed forces will give continuous basic protection both to the career serviceman and to those with shorter periods of military or naval service. We believe that an adequate staff system affording retirement and survivorship protection for peacetime servicemen is essential to maintaining a strong and efficient military establishment. Although benefits payable under service retirement systems and the programs for veterans should be adjusted to supplement the basic benefits payable under old-age and survivors insurance, nothing should be done to weaken the military staff retirement system. The combined protection under the various programs should at least equal that afforded servicemen at present. Wage credits under old-age and survivors insurance for personnel of the armed forces should represent the amount of remuneration actually received, including the cash value of perquisites and the amount of allowances to the extent that such perquisites and allowances can be regarded as remuneration for services performed. Perquisites furnished and allowances paid solely in consideration of the serviceman's dependents, however, probably cannot be so regarded, since they do not vary with the grade of the serviceman or the type of services performed. The Federal Government, as the employer, should pay the equivalent of the employer tax under the Federal Insurance Contributions Act, and the servicemen themselves should bear the cost of the employee contribution. Servicemen should have the same interest and stake in the system that other covered workers have, and the contributory character of the basic insurance program should be maintained. 8. Employees of State and Local Governments The Federal Government should enter into voluntary agreements with the States for the extension of old-age and survivors insurance to the employees of State and local governments, except that employees engaged in proprietary activities should be covered compulsorily Voluntary coverage of a limited group under an otherwise compulsory social insurance system is ordinarily undesirable and unwise. Under a system such as old-age and survivors insurance, in which benefits are not directly related to the value of the contributions paid, voluntary participation is likely to result in disproportionately large benefits for those who elect coverage. Even if voluntary participation is limited to entire groups of workers, the organizations that elect coverage are likely to be those in which most employees are persons nearing retirement age or men with large families. The smaller the organization, of course, the greater the danger of this "adverse selection." Because of the apparent constitutional barrier against Federal taxation of the States, however, coverage of the employees of State and local governments, except for those engaged in proprietary functions, will have to be on a voluntary basis unless these government employees are to be denied the protection of the Federal program. Because of this fact, and because a clear need exists for old-age and survivors insurance protection of these employees, the Council believes that a voluntary plan should be offered to State and local governments in their capacity as employers. Coverage can and should be extended on a compulsory basis to government employees engaged in proprietary--as opposed to government--functions of the employing units. Proprietary activities include, for example, State liquor stores, municipal subway systems, and other public utilities that are owned and operated by the government unit. Compulsory extension of coverage to these groups appears to raise no constitutional questions and would immediately give 150,000 to 200,000 workers the advantages of basic social insurance protection. Under a voluntary system, adverse selection occurs when coverage is elected by only a part of the total employee group and that part is not representative of the entire group. Such selection can be controlled to some extent by restricting the employer's latitude of choice in determining coverage of the plan. The Council, therefore, recommends that coverage be permitted only when elected for all employees within an occupational or departmental group. Thus, when coverage is extended to a government department, bureau, or other administrative division of the State or of a locality, all employees of the department would have to be covered. If coverage is extended to an occupational group, all employees of a State or of a local government unit who are engaged in the specified type of work (such as teachers, typists, truck drivers, janitors) would have to be covered. As further assurance that the covered group will contain a reasonably representative distribution of risks, coverage should be permitted only if one-fourth of the employees of the State or local government (such as a county, township, municipality, or school district) are brought into the program. This requirement would probably be adequate for the larger local government units, but a more restrictive one is recommended for localities with less than 400 employees. If the locality has less than 400 but more than 100 employees, coverage would have to be elected for at least 100 employees. If the local government unit has 100 or fewer employees, all would have to be covered. It is recommended that agreements be entered into only with States, although political subdivisions of the State should be permitted to participate. A State entering into an agreement would assume the responsibilities of an employer under old-age and survivors insurance; that is, the State, both for itself and for those of its political subdivisions which participate in the agreement, would collect and transmit to the Federal Government wage information and contributions. The fact that the Federal Government would deal only with the States would greatly reduce an otherwise heavy administrative burden. Since the agreements would be voluntary, no question of the Federal right to levy a tax on States and localities would be raised. As of April 1947, nearly 4,000,000 employees of States, political subdivisions of States, and instrumentalities of State and local governments were excluded from old-age and survivors insurance. The average earnings of these employees as a rule are somewhat lower than those in private industry. The average monthly salary during April 1947 was $160 for non-school employees and $185 for school employees as compared with an average monthly wage of about $205 in manufacturing industries. Almost half the total number of State and local employees are not covered under any retirement system, and of those who are so covered, probably about four-fifths lack adequate survivorship protection. The need of this group for the protection of the old-age and survivors insurance program is clear. An equally important reason for extending old-age and survivors insurance to employees of State and local governments is to give public workers continuous protection when they shift from one government unit to another, or between government units and private industry. Existing State and local staff retirement systems are designed primarily for those who continue in the service of the particular unit until their retirement; the majority of those who leave the service before retirement age normally forfeit any rights to retirement benefits they may have acquired. Similarly, persons who enter government employment from private industry may lose all or part of the protection they have acquired under old-age and survivors insurance. Although jobs in State and local government agencies are more stable than in many areas of private industry, there is nevertheless a substantial turn-over. In April 1946, a typical month, 3.4 million persons were employed by State and local governments, while during the whole year about 4.3 million were so employed. Thus, several hundred thousand had temporary employment in these units, or shifted from permanent government jobs to work in other fields. In 1944, about one-seventh of all non-school employment for State and local government units was on a part-time basis and about one-eighth of all State and local employment was temporary. Even for the permanent, full-time jobs, the annual turn-over probably ranges from 4 to 7 percent. Many proposals previously advanced for covering these workers have advocated excluding, on either a permissive or a mandatory basis, various limited groups of State and local employees, apparently in fear that coverage under old-age and survivors insurance would weaken or even completely destroy their State and local retirement system. As pointed out in the Council's recommendations for coverage of Federal and railroad employees, retirement systems supplementary to old-age and survivors insurance perform a valuable and necessary function. When coverage is extended to State and local employees who are members of staff retirement systems, those systems can be adjusted to supplement the basic old-age and survivors insurance benefits. Private employers have demonstrated that such adjustments can be made satisfactorily and without any loss in total retirement protection. The Council believes that in light of (a) the incontrovertible merit of the retention and development of supplementary plans, (b) the fact that employees under industrial pension systems did not suffer losses in benefits attributable to adjustment to the old-age and survivors insurance program, and (c) the fact that State and local governments have recognized the need for, and taken action to provide, retirement protection for their employees, any fear that the availability of old-age and survivors insurance will lead government units to reduce the total protection afforded their employees is unjustified.

9. A Study of Social Security Protection for the Possessions of the United States A commission should be established to determine the kind of social security protection appropriate to the possessions of the United States The social insurance and public assistance provisions of the Social Security Act do not at present apply to Puerto Rico, the Virgin Islands, Guam, or other possessions of the United States, even though the livelihood and security of the people of such possessions are bound up with the United States economy. The kind of social security protection to be afforded to these people should be based on detailed studies of economic and social conditions in the islands. Matters that require investigation include wage rates, regularity of employment, extent of unemployment, incidence of illness, and the nature of public assistance and public-health provisions now administered by the insular governments. The extended inquiry which would be called for, particularly since areas outside the continental United States are involved, is believed by the Council to be beyond its function. For this reason the Council proposes that a special commission be established to make such inquiry and recommend appropriate social security legislation. The commission should represent the general public, including residents of the possessions, as well as agencies such as the Federal Security Agency and the Departments of Labor, Agriculture, Interior, Commerce, and Treasury, which either have a special interest in the islands or would normally concern themselves with the problems at issue.

10. Inclusion of Tips in the Definition of Wages The definition of wages as contained in section 209 (a) of the Social Security Act, as amended, and section 1426 (a) of subchapter A of chapter 9 of the Internal Revenue Code should be amended to specify that such wages shall include all tips or gratuities customarily received by an employee from a customer of an employer Tips or gratuities paid directly to an employee by a customer of an employer, but not "accounted for" by the employee to the employer, are not now included in wages as defined for benefit and contribution purposes. Only a small part of all tips are now accounted for. Consequently, substantial numbers of workers in such service industries as hotels, restaurants, barber shops, and beauty parlors are denied the degree of protection they would acquire if all such payments were included in their wage records. Some workers may fail to qualify for benefits because, except for tips, their remuneration is inconsequential. This condition is especially illogical since tips are frequently contemplated in the wage contract, are earned in the service of the employer, and are received for services generally recognized as performed in the interest of the employer. Tips are included in taxable income under the Federal income-tax law. Moreover, in about half the States, such payments are reported under the State unemployment insurance laws on a more inclusive basis than under the program of old-age and survivors insurance Estimates indicate that full inclusion of tips and gratuities would sharply increase the wage credits of approximately a million workers now covered by the old-age and survivors insurance program. The increase for roughly two-thirds of that number would amount to about 40 percent of their wages as reported under present interpretation of the law. According to Department of Commerce estimates, $183,000,000 was paid in tips in 1939; $196,000,000 in 1940; $238,000,000 in 1941; $308,000,000 in 1942; and $336,000,000 in 1943. If a similar rate of increase continued after 1943, as seems likely during years of high prices, the total amount now paid in tips might well exceed half a billion dollars a year. The inclusion of such additional sums in the wage credits of approximately a million workers in covered service industries would clearly have an important effect on their benefits rights and their contributions to the trust fund. In the absence of an exact reporting of tips by persons receiving them, it would be possible to permit employers to report a reasonable estimate of the tips received by their employees, as is now done under some of the State unemployment insurance laws. In making such estimates, the employer would take into account the volume of business handled by the employee, the tips reported by other employees, the type of establishment, and any other pertinent factors. The employer should not be held responsible for any inaccurate reporting of tips by his employees, however, and should be protected from penalties on this account. Procedural and administrative questions could be settled by appropriate regulations designed to implement the intent of the law. Adoption of this recommendation, the Council believes, would bring the contributions paid and the benefits received by a large number of people more nearly in line with their actual earnings, thus ending an inequity to persons whose employment is covered by the program but who receive much of their remuneration for such employment in a form not now considered wages. It would also result in greater uniformity in interpretation of wages in laws relating to income taxes, unemployment insurance, and old-age and survivors insurance.

RECOMMENDATIONS ON ELIGIBILITY 11. Insured Status To permit a larger proportion of older workers, particularly those newly covered, to qualify for benefits, the requirements for fully insured status should be 1 quarter of coverage {5} for each 2 calendar quarters elapsing after 1948 or after the quarter in which the individual attains the age of 21, whichever is later, and before the quarter in which he attains the age of 66 (60 for women) or dies. Quarters of coverage earned at any time after 1936 should count toward meeting this requirement. A minimum of 6 quarters of coverage should be required and a worker should be fully and permanently insured if he has 40 quarters of coverage. In cases of death before January 1, 1949, the requirement should continue to be 1 quarter of coverage for each 2 calendar quarters elapsing after 1956 or after the quarter in which the age of 21 was attained, whichever is later, and before the quarter in which the individual attained the age of 65 or died {5} As under the present program, a calendar quarter in which the worker has $50 or more in earnings from covered employment. The Council recommends a "new start" in the eligibility requirements which will require the same qualifying period for an older worker now as was required for a person who was the same age when the system began operation. All workers who will have attained age 62 before the middle of 1949 would be insured with the minimum of 6 quarters of coverage, just as workers of the same age in 1937 could be insured with the minimum number. A major reason for the fact that the old-age and survivors insurance program has been slow in replacing public assistance as the chief method of meeting income loss in old age is the difficulty which older people face in meeting the present eligibility requirements. Eleven years after the inauguration of the program only about 20 percent of the population aged 65 and over is either insured under the program or receiving benefits. Eligibility requirements for the older workers as difficult to meet as those of the present program (24 quarters of coverage will be required under present provisions for those attaining age 65 in the first quarter of 1949) mean an unwarranted postponement of the effectiveness of the insurance method in furnishing income for the aged. In a contributory social insurance system, as in a private pension plan, workers already old when the program is started should have their past service taken into account. The unavailability of records of past service prevents giving actual credits under old-age and survivors insurance for employment and wages before the coverage becomes effective, but eligibility requirements and the benefit formula can and should take prior service into account presumptively. To pay benefits to all the current aged--including those who have not worked at all since the inauguration of the system might endanger the character of the benefit based on contributions and work records, but in getting the system started, it is important to make due allowance for those who, because of age, will probably continue at work for only a short period. All persons who reached age 62 before the middle of the year in which the system began to operate (1937) could be fully insured under the present act if they acquired six quarters of coverage. Those who attained age 62 in the third or fourth quarters of 1937 needed 7 quarters, and so on, while, as indicated above, those attaining age 65 in the first quarter of 1949 will need to have had 24 quarters. After 1956, under the present provisions, all persons who had attained age 21 before 1937 will need the maximum requirement of 40 quarters. Unless the present provisions are modified, all persons covered for the first time in January 1949 who are less than 57 years old will have to have 10 years of coverage before they can become eligible for retirement benefits, while even those aged 65 will need six more years of steady employment before they can receive benefits. A "new start," treating those newly covered workers in the same way that the program treated other occupational groups when they were first covered, seems reasonable and fair. While it would theoretically be possible to liberalize requirements only for newly covered workers and to retain the present provisions for all others, this is not a practical or desirable solution. Shifts between covered and non-covered employment are so common that it would be all but impossible to establish a fair criterion for determining, for the purpose of special eligibility requirements, which individuals should be treated as belonging to a newly covered occupation. Any liberalization designed to reduce the handicap of newly covered workers must be a generally applicable provision. The Council recommends that the liberalization of eligibility requirements should apply only to individuals living at the date of coverage extension. This proposal is consistent with the treatment accorded survivors under the 1939 amendments when the provisions for survivor benefits were made applicable only in cases of death after December 31, 1939. Considerable administrative difficulty would arise if the eligibility for benefits of individuals who died before the amendment of the law were reconsidered Of the various possible methods of adjusting the fully insured status requirement for newly covered workers, the one we recommend seems to us to offer the advantages of uniformity and simplicity and at the same time to provide a much-needed liberalization in the requirements for all older workers. It would also reduce the disadvantages which many workers normally in covered employment now face because of their work during the war in Government shipyards, munitions plants, emergency Government agencies, and other non-covered occupations. The new-start method would be impractical if extension is on a piecemeal basis. More than one "new start," we believe, would be indefensible and would tend to weaken public confidence in the program. It would be possible to use the new-start plan, however, even though coverage is not extended to Federal and railroad workers until later, since available records of past employment and wages for these workers would permit crediting their back wages. Under such an arrangement, amounts equivalent to the contributions which would have been collected if the workers had previously been covered under old-age and survivors insurance could be transferred to the old-age and survivors insurance trust fund from the trust funds for their separate Federal retirement systems. The "new start" would result in payment of retirement benefits to a much higher proportion of the aged during the early years of the system, but it would not increase beneficiary rolls and costs in the later years since the eligibility requirements would remain the same for workers now young.

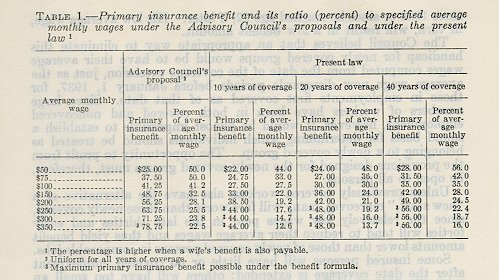

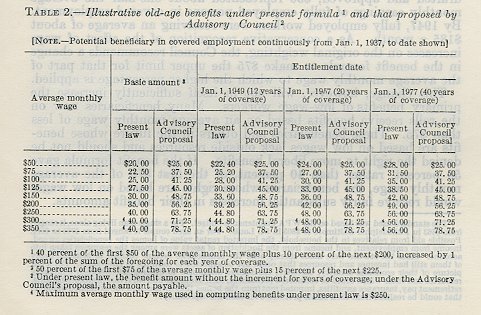

RECOMMENDATIONS ON BENEFITS 12. Maximum Base for Contributions and Benefits To take into account increased wage levels and costs of living, the upper limit on earnings subject to contributions and credited for benefits should be raised from 3,000 to $4,200. The maximum average monthly wage used in the calculation of benefits should be increased from $250 to $350 {6} {6} While the majority of the Council favor increasing the upper limit to $4,200, some favor keeping the limit at $3,000 and some favor increasing it to $4,800. The reasons for these two positions are given in appendix I-F. A social insurance program must be adjusted periodically to basic economic changes. In a dynamic economy, provisions which were appropriate at the time they became effective inevitably become outmoded. This is what has happened to the limitation placed on the amount of wages subject to contributions and allowed as wage credits. In 1939, when the $3,000 maximum wage base was established, nearly 97 percent of all workers in covered employment had wages of less than $3,000 a year, and thus they were required to pay contributions on their total wages and could have their total wages counted toward benefits. Even among workers who were steadily employed throughout 1939, fewer than 5 percent received wages of more than $3,000 a year. With the general rise in wage levels since 1939, however, the $3,000 limitation has tended to exclude from taxation and use in benefit computations part of the wages of a substantial proportion of covered workers. In 1945 about 14 percent of all covered workers had wages exceeding $3,000, and among workers who were steadily employed throughout the year, about 24 percent had wages in excess of that amount. The wage base for contributions and benefits under the program should be higher not only because of increases in the level of wages but also because of price increases. Since the base has not kept pace with rising prices, benefits now supply a smaller proportion of the costs of maintaining the beneficiary's previous standard of living than they did in 1939. Today for example, $4,200 a year represents a somewhat lower standard of living than $3,000 a year could purchase a decade ago. Raising the upper limit on wages is necessary if the relationship between benefits and standards of living which was intended in the 1939 amendments is to be maintained. To take full account of the increase in wages and prices, the limitation on taxable wages would have to be raised to somewhat more than $4,800. The Council, however, recommends that a part of this increase in wages be disregarded by changing the limitation to $4,200 as a conservative adjustment to the rise in wage and price levels which has occurred since the $3,000 figure was adopted. With a wage base of $4,200, about 95 percent of the workers in covered employment in 1945 would have had all their wages from covered employment available for benefit purposes. If the old-age and survivors insurance program is to fulfill its function, benefits for all insured workers must be increased. Since the American system of relating benefits to past wages rests on the principle that considerations of individual security and individual incentive require a relationship between benefits and the previous standard of living of the retired person, benefits must be increased for higher-paid wage earners as well as for workers in the lower income brackets. Comparisons between the primary insurance benefits payable under the plan proposed by the Advisory Council and those payable under the present program appear in table l. As those figures show, we recommend that a worker with an average monthly wage of $350 (the maximum) shall have the potential protection of a primary insurance benefit representing 22.5 percent of his average monthly wage. Under the present program, that percentage represents the primary insurance benefit of a worker who has earned $3,000 or more a year and who has had 40 years of coverage.

An objective of the present law is to have workers in the highest wage brackets covered by the system pay the costs of their own benefits over a full working lifetime. Under the benefit formula we have recommended, benefits for the $4,200-a-year man bear approximately the same relation to his contributions as benefits under the present law bear to the contributions of the $3,000-a-year man. With the increased base, the high-paid person will have somewhat higher benefits than he would have had if only the formula were changed, but he will in the long run, pay for nearly all the increase in the cost of his benefits. If the wage base is not increased, those in the higher wage brackets will have higher benefits without having contributed toward the cost of the increases.

13. Average Monthly Wage The average monthly wage should he computed as under the present law, except that any worker who has had wage credits of $60 or more in each of six or more quarters after 1948 should have his average wage based either on the wages and elapsed time computed as under the present law or on the wages and elapsed time after 1958, whichever gives the higher result Persons whose occupations have been excluded from coverage under the present program will suffer serious disadvantage after coverage is extended, unless an alternative is permitted for the present method of calculating the average monthly wage. Under the present law, benefit amounts are based on an average computed, in general, by adding all wage credits a worker has received for covered employment and dividing that sum by all the months elapsing since 1936, except for quarters before the worker reached age 22 in which he received less than $50. On this basis, a worker who has been in an employment hitherto excluded from coverage will always be penalized for his former lack of coverage, since, in effect, his wages from newly covered employment will be averaged over all the months elapsed since 1936 or since he reached age 22, if later. His low average wage, in turn, will result in a low benefit amount. The Council believes that an appropriate way to eliminate this handicap for newly covered groups would be to have their average wages computed from the date of the coverage extension, just as the average wage now disregards periods before January 1, 1937, for those in employments first covered as of that date. Since large numbers of workers have been in both covered and non-covered employment, however, it would be almost impossible to establish a sound basis for determining which individuals should be treated as belonging to a newly covered group. The opportunity to profit from the provisions designed for the newly covered groups must, therefore, be open to all persons. Unless previously covered workers also have the alternative of a "new start," moreover, many will fare worse than those newly covered, since the relatively low wages paid in the late thirties and early forties will tend to reduce their average wages and thus yield benefit amounts lower than those of newly covered persons in comparable jobs. Some insured persons will have little or no covered employment after the date coverage is extended; others will have too small an amount to form a fair basis for determining an average; and others may have employment after the "new start" at wages much lower than their previous earnings. The starting point of January 1937 specified in the present law should, therefore, be retained as an alternative and the individual worker's average wage computed from that date if it gives a higher amount than would the "new start." The new start for all, on an alternative basis, appears to be the only equitable plan, but for the reasons pointed out in the recommendation for a new start on insured status (recommendation 11, p. 29) we do not recommend a new start unless coverage is extended broadly as of one date. 14. Benefit Formula To provide adequate benefits immediately and to remove the present penalty imposed on workers who lack a lifetime of coverage under old-age and survivors insurance, the primary insurance benefit should be 50 percent of the first $75 of the average monthly wage plus 15 percent of the remainder up to $275. {7} Present beneficiaries, as well as those who become entitled in the future, should receive benefits computed according to this new formula for all months after the effective date of the amendments {7} The members of the Council who favor retaining $3,000 as the maximum annual wage credit and taxable wages would retain $250 as the maximum average monthly wage. They advocate a primary insurance benefit representing 50 percent of the first $75 of that monthly wage plus 15 percent of the remainder up $175. The benefit formula of the present program, with its automatic increase of 1 percent for each year of coverage, in effect postpones payment of the full rate of benefits for more than 40 years from the time the system began to operate. Under such provisions, if the benefit amount of a retired worker after he has had a lifetime of coverage represents a reasonable proportion of his average wage, that for older workers who have been in the system for only a few years and for the survivors of younger workers will almost of necessity be inadequate. Thus, the survivors of a man who began working at age 20 and dies at age 30 will have rights to benefits only about three-fourths as large as those which the same average monthly wage would have provided if he had lived to age 65. Yet the worker who dies at an early age has had less opportunity than have older workers to accumulate savings and other resources to supplement the benefits payable to his survivors. The Advisory Council believes that adequate benefits should be paid immediately to retired beneficiaries and survivors of insured workers but considers it unwise to commit the system to automatic increases in the benefit for each year of covered employment. Benefits payable under old-age and survivors insurance, with the beneficiaries' other permanent resources, should suffice to supply at least the basic necessities of life for the great majority of beneficiaries. The present program does not achieve this objective. Field studies made by the Bureau of Old-Age and Survivors Insurance in 1941 and 1942 in seven cities showed that one-third of the primary beneficiaries surveyed had insufficient non-relief income, assets, and possible help from relatives in their household for a maintenance level of living and that, taking account of their own permanent resources only, nearly two-thirds of the beneficiaries had less than was required for a maintenance budget. {8} {8} The standard used was based on the WPA maintenance budget. For a single man living alone it ranged from $463 in Philadelphia-Baltimore to $505 in St. Louis. For an aged couple it ranged from $,773 to $814. Possible aid from relatives in the household, the imputed rental value of homes the beneficiaries owned, income from employment, and income from the liquidation of assets were among the resources taken into account. Since the studies were made shortly after the beneficiaries became entitled to benefits, many of them still had incomes and resources that could not be expected to continue in later years. For a fair picture of their economic security, therefore, the studies attempted to differentiate between temporary resources and those which could be considered permanent, such as old-age and survivors insurance benefits, retirement pay, insurance annuities, imputed rent from the homes they owned, and the estimated amounts that could be realized from their assets prorated over their life expectancy. Inadequate as benefits were in 1941-42, they are even less adequate now that costs of living have increased by at least 60 percent. The average primary benefit now being paid is only about 10 percent higher than that paid in 1940. The table in appendix I-D shows the distribution of benefits being paid under the present program at the end of 1947. The inadequacy of these benefits is self-evident. The benefit formula in the present Social Security Act provides a primary benefit representing 40 percent of the first $50 of the average monthly wage and 10 percent of the next $200. It is thus weighted in favor of workers whose average wages are low. As a result of increases in wage rates, the effect of the original weighting, however, has been substantially reduced. In 1939, when the program was drafted and approved, $50 represented about one-half the average monthly earnings of fully employed persons in covered employment. By 1947, fully employed workers were receiving an average of about $185 a month. As a conservative recognition of the effect of wage increases on the original weighting, the Council recommends a change in the benefit formula to make $75 the upper limit for that part of the average monthly wage to which the higher percentage is applied. This change, however, will not in itself sufficiently increase the primary benefits of low-wage workers. Many beneficiaries now on the rolls receive benefits based on an average monthly wage of less than $75. These beneficiaries and others in the future whose benefits are based on low wages lack outside resources and should not be denied the right to more liberal benefits. If the benefit formula gave 50 percent, rather than 40 percent, of the first $75 of the average monthly wage, the beneficiaries whose rights are based on low wages would receive fairly substantial increases in their benefit amounts. We also propose that the percentage applied to the portion of the average wage above $75 be increased to 15 percent. If that percentage remains fixed at 10 percent, there will be too little spread between the benefit amounts of low-income. and high-income workers. Thus, for an average monthly wage of $100, the primary benefit would be only $10 less than that for an average wage of $200, a differential that we believe is insufficient for the wage interval of $100-$200, which now includes the great majority of workers in covered employment. We believe that benefits should be related to the continuity of the worker's coverage by and contributions to the system, as well as to the amount of his earnings. Under our recommendations, accordingly, benefits will continue to vary--as they now do--with both these factors. Thus, in figuring the average monthly wage (recommendation 13, p.33), a worker's total wage credits are--and would continue to be--divided by the total number of months that he might have been contributing to the system. His average wage, and consequently his primary benefit, will therefore be the smaller for each month lacking in his record of covered employment. In our opinion, this method of adjusting benefits permits sufficient differentiation between workers who are steadily employed in covered jobs and those whose covered employment is only brief or intermittent. Thus, an increment is not needed for the purpose of such differentiation With coverage broadly extended, the increment would serve largely to reward younger workers for their greater contributions by paying them higher retirement benefits than those paid to persons who were old when the system started. To us, such discrimination seems undesirable. The older worker should not be penalized for the fact that he could not contribute throughout his life. We propose, in effect, that, as in many private pension plans, the older worker receive credit for his past service and acquire rights to the full rate of benefits now.

A major draw-back in liberalizing a benefit formula that contains an increment lies in the danger that benefits in future years will be excessively high. By eliminating the increment, the benefits paid now can be more adequate than would seem feasible if the level of benefits were also to be raised automatically in future years by the application of an increment in the formula.

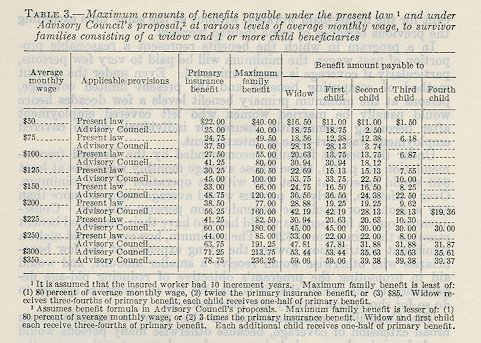

15. Increased Survivor Benefit To increase the protection for a worker's dependents, survivor benefits for a family should be at the rate of three-fourths of the primary insurance benefit for one child and one-half for each additional child, rather than one-half for all children as at present. The parent's benefit should also be increased from one-half to three-fourths. Widows' benefits should remain at three-fourths of the primary insurance benefit Adoption of this recommendation would serve mainly to provide higher benefits for children of deceased workers, since few parents of insured workers are eligible for benefits. Families consisting of young children and widowed mothers would benefit particularly from this recommendation. Studies made by the Bureau of Old-Age and Survivors Insurance in 1940-42 indicate that this beneficiary group is the one most in need of benefit increases. Of the widows with entitled children, 44 percent--a 1arger percentage than for any other beneficiary type--were found to have insufficient income for a maintenance level of living {9} and had net assets of less than $2,500. Of the widows with three or more children, 73 percent had to live below this maintenance level.

There is no good reason for these differentials in benefit rates. The Council's recommendation would result in a uniform ratio to the primary benefit for all survivor benefits paid to a sole beneficiary and for all two-person and three-person beneficiary groups, except for those consisting only of children.