Appendix C of the 1983 Greenspan Commission on Social Security Reform

Chapter 2

FINDINGS AND RECOMMENDATIONS

The National Commission was assigned the critical job of assessing whether the OASDI program has financing problems in the short run and over the long-range future (as represented by the 75-year valuation period) and, if so, recommending how such problems could be resolved.

The National Commission has agreed that there is a financing problem for the OASDI program for both the short run, 1983-89 (as measured using pessimistic economic assumptions) and the long range, 1983-2056 (as measured by an intermediate cost estimate) and that action should be taken to strengthen the financial status of the program.(1) The National Commission recognized that, under the intermediate cost estimate, the financial status of the OASDI program in the 1990s and early 2000s will be favorable (i.e., income will significantly exceed outgo) -- see Table 7A in Appendix K. The National Commission also recognized that, under the intermediate cost estimate, the financial status of the HI program becomes increasingly unfavorable from 1990 until the end of the period for which the estimates are made -- see Table 7B in Appendix K.

(1) The assumptions underlying these cost estimates are summarized in Tables 12 and 13 of Appendix K.

The National Commission makes the following recommendations unanimously:

(1) The members of the National Commission believe that the Congress, in its deliberations on financing proposals, should not alter the fundamental structure of the Social Security program or undermine its fundamental principles.* The National Commission considered, but rejected, proposals to make the Social Security program a voluntary ones or to transform it into a program under which benefits are a product exclusively of the contributions paid, or to convert it into a fully-funded program, or to change it to a program under which benefits are conditioned on the showing of financial need.**

* See additional views of Commissioner Archer in Chapter 4.

** See additional views (with regard to the last point) of Commissioners Archer, Fuller, and Waggonner in Chapter 4.

(2) The National Commission recommends that, for purposes of considering the short-range financial status of the OASDI Trust Funds, $150-200 billion in either additional income or in decreased outgo (or a combination of both) should be- provided for the OASDI Trust Funds in calendar years 1983-89.

(3) The National Commission finds that, for purposes of considering the long-range financial status of the OASDI Trust Funds, its actuarial imbalance for the 75-year valuation period is an average of 1.80% of taxable payroll.(2)

(2) This figure is the actuarial lack of balance according to the intermediate (Alternative II-B) cost estimate in the 1982 Trustees Report, after adjustment for the effects of legislation and the actual benefit increase for June 1982.

The National Commission was able to reach a consensus for meeting the short-range and long-range financial requirements, by a vote of 12 to 3. The 12 members voting in favor of the "consensus" package were Commissioners Ball, Beck, Conable, Dole, Fuller, Greenspan, Heinz, Keys, Kirkland, Moynihan, Pepper, and Trowbridge; the 3 members voting against the "consensus" package were Commissioners Archer, Armstrong, and Waggonner.

The 12 members of the National Commission voting in favor of the "consensus" package agreed to a single set of proposals to meet the short-range deficit (with Commissioner Kirkland dissenting on the proposal to cover newly hired Federal employees). They further agreed that the long-range deficit should be reduced to approximately zero. The single set of recommendations would meet about two-thirds of the long-range financial requirements. Seven of the 12 members agreed that the remaining one-third of the long-range financial requirements should be met by a deferred, gradual increase in the normal retirement age, while the other 5 members agreed to an increase in the contribution rates in 2010 of slightly less than one-half percent (0.46%) of covered earnings on the employer and the same amount on the employee, with the employee's share of the increase offset by a refundable income-tax credit (see the statements in Chapter 4 for a presentation of these approaches).

Various possible short-range and long-range financing options are displayed in the Commission's Background Book entitled Old-Age, Survivors, and Disability Insurance and Hospital Insurance Programs -- Actuarial Cost Estimates for OASDI and HI and for Various Possible Changes in OASDI and Historical Data for OASDI and HI, revised version, December 1982 (which is included in this report as Appendix K). The derivation and underlying basis of the additional financial resources needed in 1983-89, as stated in item (2), are described in detail on pages 16-21 of Appendix J.

Provisions of "Consensus" Package

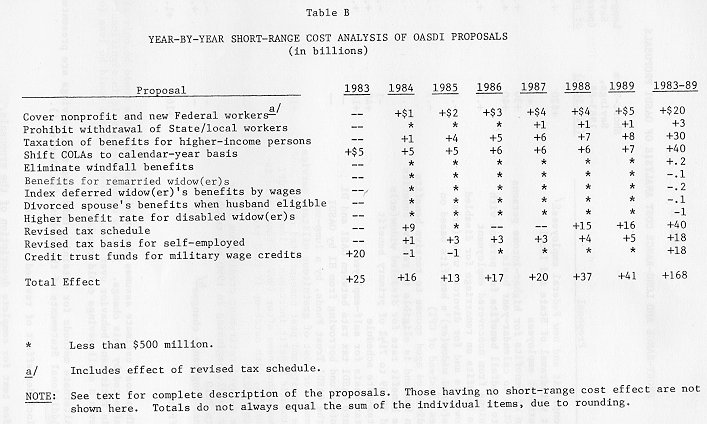

Recommendations Nos. (4) to (16) describe the provisions of the "consensus" package. Table A presents the actuarial cost data for this package for both the short range (1983-89 in the aggregate) and the long range (the 75-year valuation period, ending with 2056). Table B gives the year-by-year actuarial cost data for the short-range period. The cost estimates underlying these figures are based on economic assumptions which have been developed in recent weeks and which assume significantly lower levels of both price and wage inflation than does the Alternative III estimate in the 1982 OASDI Trustees Report (and even somewhat lower than in the Alternative II-B estimate).

Table A: SHORT-RANGE AND LONG-RANGE COST ANALYSIS OF OASDI PROPOSALS |

||

Proposal |

Short-Term Savings, 1983-89 (billions) |

Long-Range Savings (percentage of payroll) |

Cover nonprofit and new Federal employees (c) |

+$20 |

+.30% |

Prohibit withdrawal of State and local government employees |

+3 |

-- |

Taxation of benefits for higher-income persons |

+30 |

+.60 |

Shift COLAs to calendar-year basis |

+40 |

+.27 |

Eliminate windfall benefits for persons with pensions from noncovered employment |

+.2 |

+.01 |

Continue benefits on remarriage for disabled widow(er)s and for divorced widow(er)s |

-.1 |

-- |

Index deferred widow(er)'s benefits based on wages (instead of CPI) |

-.2 |

-.05 |

Permit divorced aged spouse to receive benefits when husband is eligible to receive benefits |

-.1 |

-.01 |

Increase benefit rate for disabled widow(er)s aged 50-59 to 71 1/2% of primary benefit |

-1 |

-.01 |

Revise tax-rate schedule |

+40 |

+.02 |

Revise tax basis for self-employed |

+18 |

+.19 |

Reallocate OASDI tax rate between OASI and DI |

-- |

-- |

Allow inter-fund borrowing from HI by OASDI |

-- |

-- |

Credit the OASDI Trust Funds, by a lump-sum payment for cost of gratuitous military service wage credits and past unnegotiated checks |

+18 |

-- |

Base automatic benefit increases on lower of CPI or wage increases after 1987 if fund ratio is under 20%, with catch-up if fund ratio exceeds 32% |

-- |

-- |

Increase delayed retirement credit from 3% per year to 8%, beginning in 1990 and reaching 8% in 2010 |

-- |

-.10(a) |

Additional long-range changes (b) |

-- |

+.58 |

Total Effect |

+168 |

+1.80 |

(a) This cost estimate assumes that retirement patterns would be only slightly affected by this change. If this change does result in significant changes in retirement behavior over time, the cost increase would be less (or possibly even a small savings could result). (b) Alternate methods for obtaining this long-range savings are presented in the Additional Statements of the members (in Chapter 4). (c) Includes effect of revised tax schedule. NOTE: See text for complete description of the proposals. |

||

The "consensus" package would provide an estimated $168 billion in additional financial resources to the OASDI program in calendar years 1983-89. This amount is very close to the midpoint of the $150-200 billion range stated in Recommendation No. 2. Actually, because the economic assumptions which are used for this package involve a lower inflation rate as to both prices and wages than those which had been used earlier in the deliberations, the resulting $168 billion of additional financial resources is really relatively near the upper end of the desired range.

(4) The National Commission recommends that coverage under the OASDI program should be extended on a mandatory basis, as of January 1, 1984, to all newly hired civilian employees of the Federal Government.(3)/* The National Commission also recommends that OASDI-HI coverage should be extended on a mandatory basis, as of January 1, 1984, to all employees of nonprofit organizations.

It is important to note that covering additional groups of workers such as those specified in this recommendation not only results in a favorable cash-flow situation in the short run, but also has a favorable long-range effect. The additional OASDI taxes paid on behalf of the newly-covered workers over the long run will exceed, on the average, the additional benefits which result from such employment(4), assuming that the program is in long-range actuarial balance.

(3) Under present law, temporary Federal civilian employees are covered by the OASDI-HI program, and all other Federal civilian employees are covered under the HI program, beginning January 1, 1983. All persons in the armed forces are covered by the OASDI-HI program.

* See additional views of Commissioner Archer and additional views of Commissioner Kirkland in dissent, in Chapter 4.

The National Commission believes that an independent supplemental retirement plan should be developed for the Federal new hires, which would be part of the Civil Service Retirement system (just as private employers have plans supplementing the OASDI program). It is important to note that present Federal employees will not be affected by this recommendation (and that the financing of their benefits over the long run will not be adversely affected).

(5) The National Commission recommends that State and local governments which have elected coverage for their employees under the OASDI-HI program should not be permitted to terminate such coverage in the future -- specifically, termination notices now pending would be invalid if the process of termination is not completed(5) by the enactment date of the new legislation.

(4) The vast majority of the individuals involved would have qualified for sizable OASDI benefits as a result of other employment even if coverage were not extended to these two categories of workers. Also, they tend to have higher-than-average wages and, therefore, are entitled to less-heavily weighted benefits.

(5) Current law provides that withdrawal can occur, after advance notice of at least 2 years, at the end of the calendar year specified in the withdrawal notice. For example, a withdrawal notice filed in February 1981 would (if not withdrawn earlier by the State or local government entity) result in the process of termination being completed on January 1, 1984.

(6) The National Commission is concerned about the relatively large OASDI benefits that can accrue to individuals who spend most of their working careers in noncovered employment from which they derive pension rights, but who also become eligible for OASDI benefits as a result of relatively short periods in covered employment with other employers. Accordingly, the National Commission recommends that the method of computing benefits should be revised for persons who first become eligible for pensions from non-covered employment, after 1983, so as to eliminate "windfall" benefits.

The result of such a work history is to produce OASDI benefits that contain "windfall" elements -- the benefits payable are relatively high compared to the proportion of time spent and the OASDI taxes paid during covered employment. This results from the weighted benefit formula, which treats these individuals in the same manner as if they were long-service, low-earnings workers. Specifically, the National Commission believes that these individuals should receive benefits which are more nearly of a proportionate basis than the heavily-weighted benefits now provided.

There are various methods of eliminating the "windfall" portion of benefits (while still providing equitable, proportional benefits). One method would be to modify the benefit formula for determining the Primary Insurance Amount by making the second percentage factor (32%) be applicable to the lowest band of Average Indexed Monthly Earnings (instead of the 90% factor), but the reduction in benefits would not be larger than the pension from non-covered employment. Another method would be to apply the present benefit formula to an earnings record which combines both covered earnings and also non-covered earnings in the future for the purpose of determining a replacement rate (i.e., the ratio of the benefit initially payable to previous earnings); then, that replacement rate would be applied to the average earnings based solely on covered employment. The short-range cost effect of these proposals -- applied only prospectively for new eligibles -- would be relatively small. The long-range cost effect would depend on the procedure used and on whether the recommended extension of coverage is adopted.

(7) The National Commission recommends that, beginning with 1984, 50% of OASDI benefits should be considered as taxable income for income-tax purposes for persons with Adjusted Gross Income (before including therein any OASDI benefits) of $20,000 if single and $25,000 if married. The proceeds from such taxation, as estimated by the Treasury Department, would be credited to the OASDI Trust Funds under a permanent appropriation.*

* See additional views of Commissioner Archer in Chapter 4.

It is estimated that about 10% of OASDI beneficiaries would be affected by this provision. The National Commission noted that a "notch" is present in this provision in that those with Adjusted Gross Income of just under the limit of $20,000/$25,000 would have a larger total income (including OASDI benefits) than those with Adjusted Gross Income just over the limit. The National Commission points out the presence of this "notch" and trusts that it will be rectified in the legislative process.

(8) The National Commission recommends that the automatic cost-of-living adjustments of OASDI benefits should, beginning in 1983, be made applicable to the December benefit checks (payable early in January), rather than being first applicable to the June payments. The National Commission also recommends that the amount of the disregard of OASDI benefits for purposes of determining Supplemental Security Income payment levels should be increased from $20 a month to $50.

The increase in the CPI for purposes of the automatic adjustments for any particular year is currently measured from the first quarter of the previous year to the first quarter of that particular year. This procedure should continue to apply for the adjustment in benefit amounts for 1983 (payable in early January 1984). However, for subsequent years, the comparison should be made on a "third quarter to third quarter" basis.

The recommended increase in the amount of the disregard of OASDI benefits for SSI purposes is estimated to have an initial cost of about 5750 million per year.

(9) The National Commission recommends that the following changes in benefit provisions which affect mainly women should be made:

(a) Present law permits the continuation of benefits for surviving spouses who remarry after age 60. This would also be done for (1) disabled surviving spouses aged 50-59, (2) disabled divorced surviving spouses aged 50-59, and (3) divorced surviving spouses aged 60 or over.

(b) Spouse benefits for divorced spouses would be payable at age 62 or over (subject to the requirement that the divorce has lasted for a significant period) if the former spouse is eligible for retirement benefits, whether or not they have been claimed (or they have been suspended because of substantial employment).

(c) Deferred surviving-spouse benefits would continue to be indexed as under present law, except that the indexing would be based on the increases in wages after the death of the worker (instead of by the increases in the CPI, as under present law).

(d) The benefit rate for disabled widows and widowers aged 50-59 at disablement would be the same as that for non-disabled widows and widowers first claiming benefits at age 60 (i.e., 71~2% of the Primary Insurance Amount), instead of the lower rates under present law (gradually rising from 50% at age 50 to 71 1/2% for disablement at age 60). Such change would not only be applicable to new cases, but would also be applicable to beneficiaries of this category who are on the rolls on the effective date of the provision.

(10) The National Commission recommends that the OASDI tax schedule should be revised so that the 1985 rate would be moved to 1984, the 1985-87 rates would remain as scheduled under present law, part of the 1990 rate would be moved to 1988, and the rate for 1990 and after would remain unchanged. The HI tax rates for all years would remain unchanged. The resulting tax schedule would be as follows:

Employer and Employee Rate (each) |

||||

OASDI |

OASDI-HI |

|||

Year |

Present Law |

Proposal |

Present Law |

Proposal |

1983 |

5.4% |

5.4% |

6.7% |

6.7% |

1984 |

5.4 |

5.7 |

6.7 |

7.0 |

1985 |

5.7 |

5.7 |

7.05 |

7.05 |

1986 |

5.7 |

5.7 |

7.15 |

7.15 |

1987 |

5.7 |

5.7 |

7.15 |

7.15 |

1988-89 |

5.7 |

6.06 |

7.15 |

7.51 |

1990 and after |

6.2 |

6.2 |

7.65 |

7.65 |

For 1984, a refundable income tax credit would be provided against the individual's Federal income-tax liability in the amount of the increase in the employee taxes over what would have been payable under present law.*

* See additional views of Commissioner Archer in Chapter 4.

(11) The National Commission recommends that the OASDI tax rates for self-employed persons should, beginning in 1984, be equal to the combined employer-employee rates. One-half of the OASDI taxes paid by self-employed persons should then be considered as a business expense for income-tax purposes (but not for purposes of determining the OASDI-HI tax).*

* See additional views of Commissioner Archer in Chapter 4.

Under present law, self-employed persons pay an OASDI tax rate which is approximately equal to 75% of the combined employer-employee rate (exactly 75% for 1985 and after) and an HI tax rate which is 50% of the combined employer-employee rate. Also, under present law, self-employed persons cannot deduct, as business expenses, any OASDI-HI taxes paid. The reduction in income taxes payable by the self-employed during 1984-89 as a result of considering one-half of their OASDI taxes as a business expense is estimated to be about $12 billion.

(12) The National Commission recommends that the proposed OASDI tax rates should be allocated between the OASI and DI Trust Funds in a manner different from present law, in order that both funds will have about the same fund ratios.

(13) The National Commission recommends that the authority for inter-fund borrowing by the OASDI Trust Funds from the HI Trust Fund be authorized for 1983-87.

(14) The National Commission recommends that a lump-sum payment should be made to the OASDI Trust Funds from the General Fund of the Treasury for the following items:

(a) The present value of the estimated additional benefits arising from the gratuitous military service wage credits for service before 1957 (subject to subsequent adjustments if the experience deviates from the estimates).

(b) The amount of the combined employer-employee OASDI taxes on the gratuitous military service wage credits for service after 1956 and before 1983 (which were granted as a recognition of non-cash remuneration, and the cost of which is met, under present law, when additional benefits derived therefrom are paid). The payment would include interest, but would be reduced for any costs therefor which were paid in the past to the OASDI Trust Funds from the General Fund of the Treasury. In the future, the OASDI Trust Funds would be reimbursed on a current basis for such employer-employee taxes on such wage credits for service after 1982.

(c) The amount of uncashed OASDI checks issued in the past (which were charged against the trust funds at time of issue), estimated at about $300-400 million. (The problem of uncashed checks in the future has been corrected as a result of changed procedures of the Treasury Department with regard to checks which are uncashed for a long time.)

(15) The National Commission recommends that, beginning with 1988, if the fund ratio(6) of the combined OASDI Trust Funds as of the beginning of a year is less than 20.0% (except that, for 1988, the fund ratio to be considered would be that estimated for the end of that year), the automatic cost-of-living (COLA) adjustments of OASDI benefits should be based on the lower of the CPI increase or the increase in wages. If the fund ratio is 32.0% or more at the beginning of a year, payments will be made during the following year as supplements to monthly benefits otherwise payable to make up to individuals for any use of wage increases instead of CPI increases in the past, but only to the extent that sufficient funds are available over those needed to maintain a fund ratio of 32.0%.(7)

(6) The fund ratio is the balance in the fund, exclusive of any outstanding loan from the HI Trust Fund, as a percentage of the estimated outgo from the fund in the year.

(7) When the fund ratio at the beginning of a particular year exceeds the trigger level of 32.0%, there would be a "catch-up" for those individuals on the benefit rolls at the time of the next COLA for whom some benefits in the past had been increased on the basis of wage increases instead of CPI increases. For each such person, the cumulative percentage benefit reduction up to the beginning of that particular year would be recorded. Such percentage reduction would be applicable as a percentage increase for the benefits payable for the first 12 months following the next COLA. If there were not sufficient funds available to provide a complete "catch-up", then the percentage increase in the benefits for the 12-month period would be pro-rated so that the estimated cost of this "catch-up" would equal the funds available.

This provision will serve as a stabilizer against the possibility of exceptionally poor economic performance over a period of time.

The increases in wages would be determined from the "SSA average wage index", the series used by the Social Security Administration in determining such elements of the program as the maximum taxable earnings base and the "bend points" in the formula for the Primary Insurance Amount. As an example, assuming that this new indexing method were applicable for 1995 (for the December checks), the COLA percentage would be the smaller of (1) the percentage increase in the CPI from the third quarter of 1994, to the third quarter of 1995 or (2) the percentage increase in the "SSA average wage index" from 1993 to 1994.

(16) The National Commission recommends that the Delayed-Retirement Credit should be increased from the present 3% (for persons who attained age 65 after 1981) to 8%, to be phased in over the period 1990-2010.

Under present law, persons who do not receive benefits after age 65 (essentially because of substantial employment of any kind) receive increases in their benefit (and in their widowed spouse's benefit, but not in any other auxiliary benefit) at the rate of 3% for each year of delay in receipt of benefits from age 65 through age 71.(8) Under the proposal, the Delayed Retirement Credit for months in 1990 would be at the rate of 3 1/4%, those for 1991 would be at the rate of 3 ½%, etc. until an 8% rate would be reached in 2009 and after.

(8) A technical error in the law results in age 71 being stipulated, rather than age 69; this provision should not be applicable after age 69, because the earnings test no longer applies beyond that age. This error should be corrected when the recommended change is legislated.

Coverage of Payments Under Salary-Reduction Plans

(17) The National Commission recommends that, in the case of salary-reduction plans qualifying under Section 401(k) of the Internal Revenue Code, any salary reduction thereunder shall not be treated as a reduction in the wages subject to OASDI-HI taxes.

Section 401(k) of the Internal Revenue Code permits employers to install "salary-reduction" plans, under which employees may elect to forego a salary increase or have part of their pay set aside in a tax-sheltered fund. Such salary is neither subject to Federal income tax currently, nor is it subject to the OASDI-HI tax. The National Commission believes that, for both OASDI-HI tax and benefit credit purposes, any salary deferred under a plan meeting the requirements of Section 401(k) should be considered in exactly the same manner as cash remuneration.

This proposal will not produce significant additional income to the OASDI and HI programs currently, because not many of these salary-reduction plans have yet been put into effect. However, if the recommendation is not followed, it is quite probable that many such plans will be instituted and that, in the absence of the action recommended, considerable decreases in OASDI-HI tax income to the trust funds and in benefit credits would result.

Fail-Safe Mechanisms

(18) The National Commission believes that, in addition to the stabilizing mechanism of Recommendation (15), a fail-safe mechanism is necessary so that benefits could continue to be paid on time despite unexpectedly adverse conditions which occur with little advance notice.(9) Several types of fail-safe mechanisms are possible other than the one currently being used -- inter-fund borrowing; there is strong disagreement among the members as to which type of mechanism should be used. A combination of these types of mechanisms would, of course, be possible.

A number of mechanisms were considered. One would be to borrow, for a limited period, from the General Fund of the Treasury. Such limitation would prevent this procedure from being a part of the permanent method for financing the program. Another possibility along this line would be to permit the trust funds to issue their own bonds for sale to the general public.

A second mechanism would be to reduce, temporarily, the benefits payable. Alternatively, such a result could be accomplished indirectly, by reducing the amount of the next benefit increase which would occur as a result of the automatic-adjustment provision for benefits in eligibility status.

The third mechanism would be to increase, temporarily, the OASDI tax rates and/or the maximum taxable earnings base.

(9) It is most unlikely that such a situation would, with proper actuarial guidance, happen with shorter notice than a year or so.

------------------------------

The National Commission makes a number of recommendations in addition to those discussed previously. Although these additional recommendations are of importance, they will not likely have any significant financial effects, on the average over the long run.

Investment Procedures

(19) The National Commission recommends that the investment procedures of the OASI, DI, HI, and SMI Trust Funds be revised so that (1) all future special issues would be invested on a month-to-month basis, (i.e., without fixed maturity dates, as under present law), at an interest rate based on the average market rate of all public-debt obligations with a duration of four or more years until maturity (not including "flower bonds''(l0) ); (2) all present special issues would be redeemed at their face amount; (3) all "flower bonds"(10) would be redeemed at their current market values; (4) all other current holdings would be held until maturity (unless disposed of sooner, if needed to meet outgo); and (5) only special issues would be purchased by the trust funds in the future.

There has been widespread public discussion about the investment procedures of the four Social Security trust funds. The view has frequently been expressed that the investments have not been made on a proper basis and that sufficiently high rates of return have not been obtained, because the average rate of return has, in recent years, been far lower than that on newly issued Government obligations. This is not a valid comparison, because it compares the new-issues rate with the average portfolio rate, which includes the effect of the lower interest rates on long-term obligations bought some years ago (at rates which were equitable and proper at that time). The same situation as to a higher

(10) "Flower bonds" are certain series of government bonds that were issued in the past (but which are no longer issued) which contain a provision that if the purchaser holds them for a certain length of time, then for inheritance-tax purposes, they are redeemable at par (regardless of the market value) interest rate on new issues than on the total portfolio, as of recent years, has also been present for private pension funds and insurance companies.

The National Commission believes that the investment procedures followed by the trust funds in the past generally have been proper and appropriate. The monies available have generally been invested appropriately in Government obligations at interest rates which are equitable to both the trust funds and the General Fund of the Treasury and have not -- as is sometimes alleged -- been spent for other purposes outside of the Social Security program.

Nonetheless, the National Commission makes this recommendation in order to improve the level of public understanding of the operations of the trust funds. On the whole, and over the long-range future, it is likely that such a change in investment procedure will have little (if any) effect on the financial status of the Social Security program. It will probably result in a slightly higher average rate of return in the immediate future. The long-range effects are not determinable and, in any case, are not of great significance with regard to the overall financing of the program.

Although the National Commission has not considered the Medicare program in depth, it believes that the same investment procedures should apply for the HI and SMI Trust Funds as for the OASDI Trust Funds.

Public Members on Board of Trustees

(20) The National Commission recommends that two public members be added to the Board of Trustees of the OASDI Trust Funds. The public members would be nominated by the President and confirmed by the Senate. No more than one public member could be from any particular political party.

The National Commission believes that increasing the membership of the Board of Trustees of the OASDI Trust Funds by including two individuals from outside the Executive Branch, on a bi-partisan basis, would be desirable from the standpoint of confidence in the integrity of the trust funds. The presence of such public members would inspire more confidence in the investment procedure (even though it is recommended that the procedure should be placed on a more or less automatic basis, as under the previous recommendation) and would help to assure that the demographic and economic assumptions for the cost estimates of the future operations of the program would continue to be developed in an objective manner. Although the National Commission is not generally making recommendations in connection with the Medicare program, it would seem reasonable that the same procedure of having two public members on the Board of Trustees should also apply for the HI and SMI Trust Funds.

Social Security and the Unified Budget

(21) A majority of the members of the National Commission recommends that the operations of the OASI, DI, HI, and SMI Trust Funds should be removed from the unified budget. Some of those who do not support this recommendation believe that the situation would be adequately handled if the operations of the Social Security program were displayed within the present unified Federal budget as a separate budget function, apart from other income security programs.

Before fiscal year 1969, the operations of the Social Security trust funds were not included in the unified budget of the Federal Government, although they were made available publicly and were combined, for purposes of economic analysis, with the administrative budget in special summary tables included in the annual budget document. Beginning then, the operations of the Social Security trust funds were included in the unified budget. In 1974, Congress implicitly approved the use of a unified budget by including Social Security trust fund operations in the annual budget process. Thus, in years when trust-fund income exceeded outgo, the result was a decrease in any general budget deficit that otherwise would have been shown -- and vice versa.

The National Commission believes that changes in the Social Security program should be made only for programmatic reasons, and not for purposes of balancing the budget. Those who support the removal of the operations of the trust funds from the budget believe that this policy of making changes only for programmatic reasons would be more likely to be carried out if the Social Security program were not in the unified budget. Some members also believe that such a procedure will make clear the effect and presence of any payments from the General Fund of the Treasury to the Social Security program. (Under present procedures, such payments are a "wash" and do not affect the overall budget deficit or surplus).

Those who oppose this recommendation believe that it is essential that the operations of the Social Security program should remain in the unified Federal budget because the program involves such a large proportion of all Federal outlays. Thus, to omit its operations would misrepresent the activities of the Federal Government and their economic impact. Furthermore, it is important to ensure that the financial condition of the Social Security program be constantly visible to the Congress and the public. Highlighting the operations of the Social Security program as a separate line function in the budget would allow its impact thereon to be seen more clearly.

Social Security Administration as an Independent Agency

(22) The majority of the members of the National Commission believes -- as a broad, general principle -- that it would be logical to have the Social Security Administration be a separate independent agency, perhaps headed by a bi-partisan board. The National Commission recommends that a study should be made as to the feasibility of doing this.*

The Social Security Administration is now part of the Department of Health and Human Services. Its fiscal operations and the size of its staff are larger than those of the remainder of the Department combined.

The National Commission has not had the time to look into the various complex issues involved in such an administrative reorganization and, therefore, recommends that a study group should be formed to look into this matter. Issues involved include whether the leadership of such an independent agency should be assigned to a single individual or whether there should be a governing board of several members, selected on a bi-partisan basis, and whether the operations of the Medicare program should be included in such an independent agency, or whether they should remain as a subsidiary agency within the Department of Health and Human Services, as at present.

* See additional views of Commissioners Ball, Keys, Kirkland, Moynihan, and Pepper in Chapter 4.

Coverage of State and Local Government Employees

Although the National Commission believes that coverage of all persons who are in paid employment is desirable, some members do not favor mandatory coverage of employees of State and local governments.

A majority of the members is concerned about the constitutional problem of covering State and local government employees under Social Security on a mandatory basis because the Federal Government may not have the power to compel State and local governments to pay the employer share of the OASDI-HI tax. Other members believe that, regardless of the constitutionality question, the Federal Government should not do so because the two levels of government have equal roles and status. Some members point out that many State and local governments already have adequate, well-financed retirement systems for their employees, so that they do not need OASDI-HI coverage(11); others point out that many State and local systems have serious financing problems and that protection of the benefits under such systems against inflation (and often protection against other risks) is not as adequate as under the OASDI program.

(11) A relatively small number of State and local government employees do not have either OASDI-HI coverage or public-employee retirement systems.

Benefit Provisions Primarily Affecting Women

In recent years, there has been widespread discussion as to whether the basic structure of the Social Security program should be altered in view of the changes in the role of women in our society and economy.*

* See additional views of Commissioner Fuller and additional views of Commissioners Ball, Keys, Kirkland, Moynihan, and Pepper, in Chapter 4.

Some members of the National Commission believe that there should be a comprehensive change in the program to reflect the changing role of women, for example, by instituting some form of earnings sharing for purposes of the Social Security earnings record. Simply stated, earnings sharing means that all covered earnings received by a couple during the period of marriage would be pooled and half would be credited to each of their earnings records. Some other members believed that such comprehensive changes were outside of the scope of the charge of the National Commission.

Social Security Cards

The National Commission commends a recent decision of the Social Security Administration to use banknote-quality paper for new and replacement Social Security cards. The Senate Permanent Subcommittee on Investigations estimated in June 1982 that fraud involving identification cards, of which Social Security cards are the vast majority, cost the Federal Government between $15 and $24 billion per year.