This chapter presents the estimates and measures of trust fund financial adequacy for the short-range period (2023 through 2032) first, followed by estimates and measures of

actuarial status for the long-range period (2023 through 2097). Summary measures are also provided for trust fund status over the infinite horizon. As described in chapter

II of this report, these estimates depend upon a broad set of

demographic, economic, and programmatic factors. This chapter presents estimates under three sets of assumptions to show a wide range of possible outcomes, because assumptions related to these factors are subject to uncertainty. The intermediate set of assumptions, designated as

alternative II, reflects the Trustees’ best estimate of future experience; the low-cost

alternative I is significantly more optimistic and the high-cost

alternative III is significantly more pessimistic for the trust funds’ future financial outlook. The tables of this report show the intermediate estimates first, followed by the low-cost and high-cost estimates. Chapter

V describes these three sets of assumptions, along with the actuarial methods used to produce the estimates. Appendix

D and appendix

E present two additional methods to illustrate the uncertainty of the projections. Appendix

D presents sensitivity analyses of the effects of variation in individual factor s and appendix

E presents probability distributions generated by a stochastic model.

The Trustees consider the trust funds to be solvent at any point in time if the funds can pay scheduled benefits in full on a timely basis. A standard measure for assessing solvency is the “

trust fund ratio,” which is the

reserves in a fund at the beginning of a year (not including

advance tax transfers) expressed as a percentage of the cost during the year. A positive trust fund ratio indicates that the trust fund was solvent at the end of the prior year. The trust fund ratio represents the proportion of a year’s cost which the

reserves available at the beginning of that year can cover. The Trustees assume that a trust fund ratio of 100 percent of annual program cost provides a reasonable “contingency reserve.” Maintaining a reasonable contingency reserve is important because the trust funds do not have borrowing authority. After reserves are depleted, the trust funds would be unable to pay scheduled benefits in full on a timely basis if annual revenue were less than annual cost. Unexpected events, such as severe economic recessions, can quickly diminish reserves. In such cases, a reasonable contingency reserve can maintain the ability to pay scheduled benefits while giving lawmakers time to address possible changes to the program.

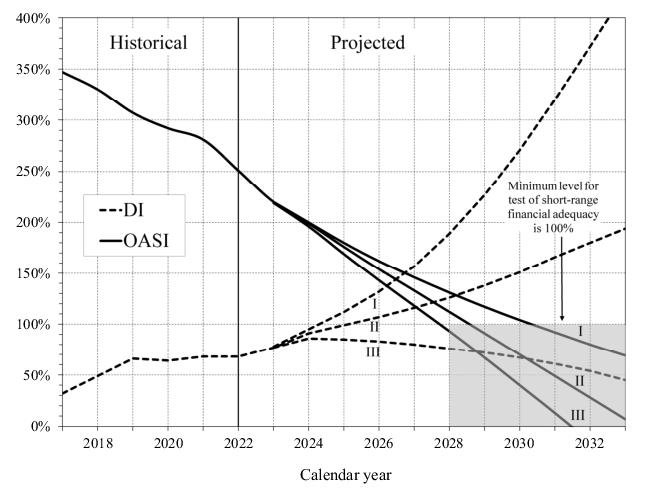

The test of short-range financial adequacy applies to the OASI and DI Trust Funds individually and combined on a hypothetical basis.

1 If the estimated trust fund ratio is at least 100 percent at the beginning of the projection period, the test requires that it remain at or above 100 percent throughout the 10-year period. If the ratio is initially less than 100 percent, then it must reach at least 100 percent within 5 years (without reserve depletion at any time during this period) and then remain at or above 100 percent throughout the remainder of the 10-year period. This test is applied using the estimates based on the intermediate assumptions. If either trust fund fails this test, then program solvency in the next 10 years is in question, and lawmakers should take prompt action to improve short-range financial adequacy.

This subsection presents projections, based on the assumptions described in chapter V, of the operations and financial status of the OASI Trust Fund for the period 2023 through 2032. These estimates assume that there are no further changes in the statutory provisions and regulations under which the OASDI program currently operates beyond the changes since last year’s report indicated in section

III.B.

2

Estimates of the OASI Trust Fund operations presented in table IV.A1 indicate that the asset reserves of the OASI Trust Fund are projected to decrease in years 2023 through 2032 under all three sets of assumptions. Under the intermediate and low-cost assumptions, asset reserves remain positive through the end of the short-range period, but under the high-cost assumptions, asset reserves become depleted in the third quarter of 2031. Trust fund ratios are similarly projected to decline throughout the 10-year projection period under all three sets of assumptions. Based on the intermediate assumptions, the reserves of the OASI Trust Fund drop below 100 percent of annual cost during 2028, to a trust fund ratio of 91 percent at the beginning of 2029, and remain below 100 percent for the remainder of the short-range period. Consequently, the OASI Trust Fund fails the test of short-range financial adequacy. See figure

IV.A1 for an illustration of these results.

The estimated income shown in table IV.A1 increases annually under each set of assumptions throughout the short-range projection period, with the exception of a small decrease in 2024 for the high-cost alternative. The estimated increases in income result primarily from the projected increases in OASDI

taxable payroll. Employment increases in years 2023 through 2032 for all three alternatives, with the exception of small decreases in covered employment in 2023 and 2024 for the high-cost alternative: the number of covered workers increases under alternatives I, II, and III from 181 million during calendar year 2022 to about 192 million, 188 million, and 184 million, respectively, in 2032.

3 The total annual amount of taxable payroll increases in years 2023 through 2032 for each alternative. Total taxable payroll increases from $9,069 billion in 2022 to $16,650 billion, $14,023 billion, and $12,189 billion in 2032, on the basis of alternatives I, II, and III, respectively.

4 These increases in taxable payroll are due primarily to: (1) projected increases in employment levels as the working-age

population increases; (2) trend increases in average earnings in

covered employment (reflecting both real growth and price inflation); (3) increases in the

contribution and benefit base under the automatic-adjustment provisions; and (4) growth in employment and average earnings.

Rising OASI cost from 2022 through 2032 reflects automatic benefit increases each year after initial benefit eligibility and increases each year for those becoming newly eligible based on rising average earnings levels, as well as the upward trend in the number of beneficiaries. The steady growth in the number of OASI beneficiaries in the past and the expected future growth result both from the increase in the aged population and from the increase in the proportion of the population that is insured for benefits.

Table IV.A2 shows the projected operations and financial status of the DI Trust Fund during calendar years 2023 through 2032 under the three sets of assumptions, together with values for actual experience during 2018 through 2022. Non-interest income for DI dropped in 2019 from its level in 2018, due to the temporary payroll tax rate reallocation from OASI to DI in 2016 through 2018. For 2022, non-interest income was higher than DI cost. Non-interest income increases generally throughout the short-range projection period under each alternative, due to most of the same factors described previously for the OASI Trust Fund beginning on page

45. DI cost grows steadily throughout the period under each alternative. Under the

intermediate and low-cost assumptions, DI reserves increase through 2032. Under the high-cost assumptions, DI reserves increase through 2026 and then decline through 2032.

For the future, DI cost is projected to increase in part due to increases in average benefit levels resulting from: (1) automatic benefit increases and (2) projected increases in the amounts of average monthly earnings on which benefits are based. Future changes in DI cost also reflect changes in the number of DI beneficiaries in current-payment status. In 2022, the number of DI beneficiaries in current-payment status continued the declining trend of the prior eight years. Under the intermediate assumptions, that number of DI beneficiaries is projected to drop further through the end of 2024, then increase through the end of 2032 to a level of about 9 million. The rate of increase after 2024 is much slower than was experienced on average from 1990 to 2010, when the population with the highest disability prevalence rates was growing rapidly due to the aging of the baby-boom generation. See section

V.C.5 for further details.

Table IV.A3 shows the projected operations and status of the combined OASI and DI Trust Funds for calendar years 2023 through 2032 under the three alternatives, together with actual experience in 2018 through 2022. Income and cost for the OASI Trust Fund represent over 80 percent of the corresponding amounts for the combined OASI and DI Trust Funds. Under the intermediate and low-cost assumptions, the combined OASI and DI Trust Funds would have sufficient financial resources to pay all scheduled benefits through the end of the short-range period, although it is important to note that under current law, one trust fund cannot share financial resources with another trust fund. Under the high-cost assumptions, combined OASI and DI trust fund reserves deplete in the fourth quarter of 2031. The combined OASI and DI Trust Funds do not satisfy the test of short-range financial adequacy because under the intermediate assumptions, trust fund reserves drop below 100 percent of annual cost during 2028, to a trust fund ratio of 96 percent at the beginning of 2029, and remain below 100 percent for the remainder of the short-range period.

Table IV.A4 presents an analysis of the factors underlying the changes in the intermediate estimates over the short-range projection period for the OASI, DI, and the combined funds from last year’s report to this report.

Table IV.A4 also shows corresponding estimates of the factors underlying the changes in the financial projections for the DI Trust Fund and for the combined OASI and DI Trust Funds. The 35-percentage-point increase in the DI trust fund ratio from the beginning of 2031 in last year’s report to the beginning of 2032 in this year’s report is the net effect of increases and decreases from the factors described above for the OASI Trust Fund, combined with other changes that are significant for DI but not OASI. The large increase of 33 points due to programmatic data and assumptions reflects lower recent disabled-worker application and incidence rates, and a more gradual return of initial disability application rates to their ultimate levels from recent lows.