Public Law 104-193 requires that members of the Social Security Advisory Board be given an opportunity, either individually or jointly, to include their views in the Social Security Administration’s annual report to the President and Congress on the Supplemental Security Income (SSI) program. We have asked the Social Security Administration to include in this year’s annual report the following statement of our views on the resource limit in the Supplemental Security Income program.

Supplemental Security Income (SSI) is a federal public assistance program for low-income people who are age 65 or older, blind, or disabled. The program provides assistance based on need, and it defines need in terms of income and resources. The definition of need draws a line that combined with age, blindness or disability, determines who is and who is not eligible for income assistance from the SSI program. Where that line should be drawn is a public policy question that must be answered by the American people’s representatives in Congress. The answer to that policy question, however, should be based to the extent possible on an empirical base. In this issue brief, we will provide a brief overview of the SSI resource limit, and consider the empirical questions that need to be answered in order to make a sound assessment of whether the rules that govern the resource limit policy are meeting the purpose Congress intended.

The 1972 federal law that established the SSI program included a resource limit as an eligibility factor for SSI benefits. Resources include any of the following owned by an SSI applicant or beneficiary or a spouse: cash, liquid assets, and real or personal property that can be converted to cash to obtain food and shelter.

2 Some resources are counted toward the limit and others are not. Examples of such non-countable (or in SSI terms, excluded) resources are an individual’s principal place of residence; one vehicle, if the beneficiary or a member of the household uses it for transportation; household goods and personal effects; and burial spaces.

3 Resource limits are useful to ensure that public dollars go only to those who really need them. If income alone was used as a marker of need, then it would be possible for individuals and couples to receive SSI benefits as long as their income was below a certain level, regardless of the amount of their savings or other resources.

The SSI program replaced a system of federal financial assistance to state programs that provided aid to the aged, blind, and permanently and totally disabled. Those state systems had asset limits, but there was no uniformity across programs. For example, one state required applicants to use all their liquid assets before becoming eligible; another allowed a cash reserve equal to one month’s cost of living. Six had limits of $300 to $350 in cash reserves. Twenty-five states required an applicant to give the welfare department a lien against his or her house or a claim against his or her estate.

4

The federalization of the former state programs established a needs-based program that had standardized eligibility rules and provided a uniform level of income support no matter where an individual lived throughout the nation. The new program also established national eligibility criteria for resources. Individuals had to have less than $1,500 in countable resources, and couples had to have less than $2,250. Those amounts were increased gradually between 1985 and 1989 to $2,000 for an individual and $3,000 for a couple and have not changed since 1989. Applicants whose resources exceed the limit, by any amount, are generally not eligible for benefits at all.

5

In some cases, other people’s resources can affect the eligibility of a claimant or a beneficiary through a process known as deeming. The term deeming means considering another person’s resources to be available for meeting a claimant or beneficiary’s needs. This happens most often with children and spouses:

|

•

|

If an aged, blind, or disabled individual is living with a spouse who is ineligible for SSI, the resources of the spouse are considered in the determination of eligibility. An individual is considered eligible only if his countable resources, together with the spouse’s countable resources, do not exceed the resource limit for a couple. For example, if an applicant is 65 years old and his spouse is not yet 65 and is not blind or disabled, the combined resources of both spouses would have to be under $3,000 in order for the applicant to be eligible.

|

Once they are on the rolls, beneficiaries whose resources exceed the limit on the first day of any month after they begin receiving payments will likely also lose their eligibility for payments until their resources are again brought down below the resource limit.

As discussed previously in this Statement, Congress has established some exceptions to the limits placed on owning resources.

8 In addition, Congress created three provisions that allow recipients to accumulate resources over $2,000 so they can become more self-sufficient and less reliant on federal assistance.

These are:

|

•

|

SSI applicants are allowed to retain Property Essential for Self Support that generates income, which is then counted in determining the appropriate amount of the monthly SSI check. An example would be a self-employed person’s business account or equipment; or a rancher’s acreage in addition to a homestead, which is rented out to others for grazing land.

|

The conference report on the 1984 legislation that raised the resource limit stated that a major purpose of allowing SSI recipients to have a certain amount of resources was to help them cover major costs of an urgent nature that could not be met from their monthly benefit payments, such as to replace a furnace or make essential household repairs.

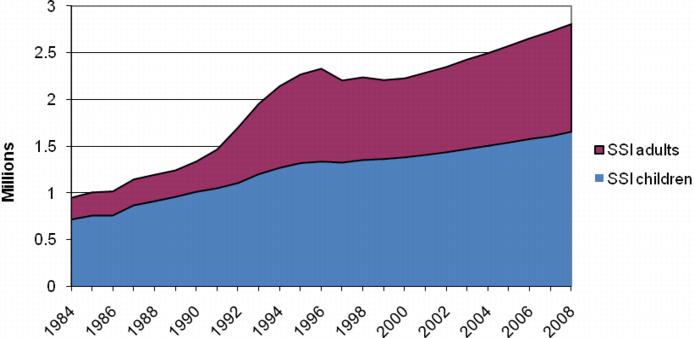

9 Research into congressional intent in 1984 does not show any plan for future increases, nor was there any discussion of indexing at that time. As the following chart shows, if the 1972 amounts had been adjusted for inflation, they would now be nearly $8,000 for an individual and $12,000 for a couple.

10

If it was intended as a minimal fund for emergencies, the resource limit of 1989 can no longer cover the type of emergencies Congress envisioned more than 20 years ago. The questions that arise are should this limit be revisited, and if so, what should be the policy relative to resource accumulation? This is a difficult issue to address particularly at this time given the current state of the economy. One of the objectives of the SSI program is to support the efforts of recipients to (re)gain self-sufficiency. The ability to acquire resources and build assets can be instrumental in achieving this objective. However, raising the resource limits comes at some cost to the taxpayer. If Congress considers this issue, it must be mindful of the need to balance the interests of beneficiaries with the interests of the taxpayers who fund the program.

For SSI recipients, the ability to save more under a higher resource limit would provide added protection against hardships resulting from a drop in income or an increase in expenses. Low-income individuals and families are especially vulnerable to unexpected changes in income or expenses. Because such families are already operating near a subsistence level, with little discretionary spending, unexpected events can result in material deprivation if they do not have savings or other resources to draw on. A recent study looked at the impact of income shocks (for example, loss of a job or reduction of hours, loss of child support or financial support from extended family) and expense shocks (for example, sudden illness or injury, entry of a non-working dependent into the household, or home or automobile repairs). The study found that, among households with non-elderly heads, with incomes in the lowest fifth, 24 percent experienced two or more material hardships (for example, a utility or phone shutoff or a missed housing payment) over a 12-month period. Having liquid assets up to $2,000 reduced the incidence of material hardship by 5 percentage points, and having liquid assets between $2,000 and $10,000 reduced the incidence by 11 percentage points.

Increasing the resource limit would change the incentives for participation in the program, and analysis is needed to estimate the effects of a change in the resource limit on two groups: those made newly eligible by raising the resource limit and those near the limit who might respond to the incentive to become eligible for the program:

|

•

|

Wherever a higher resource limit may be set, there would, by definition, be a somewhat larger group of people with countable resources above the current limit but below the new higher limit, so there is a need to estimate the effect of expanding the group of potential beneficiaries. The cost of the program to taxpayers would tend to increase depending on how many people are made newly eligible, the proportion of those newly eligible who actually apply for SSI, and the proportion of those new applicants who meet the criteria necessary to receive benefits.

|

|

•

|

Wherever the resource limit may be set, it has the potential to induce people near the limit to change their behavior. Raising the resource limit could motivate some people to change their work and savings behavior in such a way as to make them eligible for the program. Knowing that they would need to meet the specified resource limit, they might choose to reduce their accumulation of assets directly and/or choose to reduce their work effort that can lead to resource accumulation. Since changing the resource limit would mean that a different group of people would be near the resource limit, there would be a need to estimate the change in the behavior of that group of people. 12

|

Deliberation on SSI resource limits should consider the natural tension among these considerations: the interests of SSI beneficiaries in increased protection against hardships, the cost to taxpayers, and whether the change in the rules would encourage potential beneficiaries to reduce their work and savings. Empirical research is needed to provide a basis for a sound policy decision and should address such subsidiary questions as:

|

•

|

What would be the effect of an increased resource limit on the work and saving behavior of those potentially eligible? The research should distinguish among the various populations who might seek SSI benefits. The existing research on the impact of raising resource limits on labor-supply focused only on those potentially eligible for SSI because they are age 65 or older, only a quarter of current SSI beneficiaries. The work and savings behavior of those potentially qualifying because of serious health related limitations may well be very different from those who qualify based on age. In addition, the work and savings behavior of the parents of potentially eligible disabled children might well be different from the response of working age adults who would potentially be claiming benefits based on their own disability.

|

For more than 70 years, the Social Security Administration (SSA) has been issuing checks to representative payees who manage the money for beneficiaries who are deemed temporarily or permanently incapable of managing their own benefits. There is an inevitable risk that representative payees will use the benefits for their own purposes.

The representative payee program tends to get overlooked in the press of other business. From time to time there have been scandals in which payees have misused large amounts of money. In 2000 a story on a television newsmagazine about a payee who had misused $213,000 from 146 beneficiaries resulted in congressional hearings (House Ways and Means 2000, Senate Aging 2000). The scandal led to the Social Security Protection Act of 2004. Among other provisions, that act required periodic onsite reviews of certain groups of payees. It also required SSA to conduct a study of how payees were using benefit payments. That study was conducted from 2005 to 2007 by a committee of the National Research Council (NRC).

13

While protecting the interests of its most vulnerable beneficiaries is a part of SSA’s stewardship responsibilities, it is not possible for SSA to ensure that a representative payee will never take advantage of a beneficiary. The challenge for the agency is to protect beneficiaries as effectively as possible, while carrying out its primary mission of making timely and accurate benefit payments. This challenge is especially important in the SSI program, in which 37 percent of beneficiaries have a representative payee.

Six years after the enactment of the Social Security Protection Act, and three years after the NRC report, this issue brief examines ways in which SSA can continue to focus its efforts to meet this challenge. We also present some additional recommendations to strengthen SSA’s protection of beneficiaries. Specifically, we recommend that:

|

•

|

SSA should take steps to improve coordination and establish automated data exchanges with other agencies that also serve SSA’s beneficiaries. There are numerous agencies that use payees or other fiduciaries or that provide protective services. The Veterans Administration, state courts, state Adult Protective Service agencies, Protection and Advocacy agencies for people with disabilities, and state foster care agencies all serve populations that include SSA beneficiaries. Improved coordination and data exchanges can better protect the people that each agency serves.

|

Representative payment began with the Social Security amendments of 1939, which authorized the Social Security Board (as it then was known), to certify payment “to a relative or some other person” for the “use and benefit” of an applicant, when it would serve the interest of an applicant for benefits. Until that time, only retired workers were eligible for benefits. The 1939 amendments added benefits for wives of retired workers and for widows and dependent children of deceased workers. In preparing for the first monthly benefit payments in 1940, the agency saw a need to establish a way to make payments for minor children and for mentally incompetent beneficiaries. It also acknowledged its responsibility for seeing that payees used the benefits properly (Federal Security Agency, 1940).

Beneficiaries who had representative payees have always been the most vulnerable groups of beneficiaries, children and individuals who were unable to manage their own funds. But the rules put in place in 1939 did not contemplate the complexities of today’s world and the broader beneficiary population. The addition of the Disability Insurance and Supplemental Security Income programs added much larger groups of vulnerable beneficiaries. Changes in society, such as the deinstitutionalization of people with mental illness and developmental disabilities, have also changed the beneficiary population. Beneficiaries now include groups that have a variety of special needs and who may be homeless. As a result, the role of the representative payee may cover a much wider range of responsibilities than originally intended. For example a payee, in addition to managing a beneficiary’s funds, may also become involved in helping the beneficiary find shelter or obtain treatment or assist with employment.

Dealing with representative payees in the SSI program is a substantial workload for SSA. About 2.8 million SSI beneficiaries, or about 37 percent of the total, have payees (SSA, SSI Annual Statistical Report, 2009). Over just the last quarter century, the number of SSI beneficiaries with payees has risen by 197 percent, while the total of number of SSI beneficiaries increased by 87 percent (SSA, Annual Statistical Supplements).

The selection and monitoring of such a large number of payees is a daunting task. In FY 2009, SSA spent 1,900 workyears, nearly 3 percent of its total workyears, on representative payee activities, not including those involved in initial claims. That is more time than it spent on Medicare activities and nearly as much time as it spent on overpayments or continuing disability reviews (SSA Workload Trend Report, FY 2009).

The great majority of payees receives no compensation for their services and deserves gratitude for volunteering their time and effort. As the following chart shows, most payees are relatives. But according to SSA it is difficult to even find individuals or organizations that are willing to serve as payees for some beneficiaries and in some geographic areas (National Research Council). SSA tries to balance the need to find payees who are willing to take on this responsibility against the burdens that oversight puts on them. The agency tries to maintain an appropriate level of monitoring without requiring so much of payees that they will avoid taking on the responsibility.

Finding the balance between adequate oversight and not overburdening payees makes monitoring difficult. A payee who is close to the beneficiary and uses the benefits in the beneficiary’s interest may not have the ability to maintain records and report on them. In fact, only about two-thirds of the payees surveyed in a recent study indicated that they kept records of how the benefits they managed were spent (National Research Council). The accounting form used by SSA, as we will describe later, is simple – in fact it has been criticized for being too simple – but it is not understood by many payees who complete it. It is beyond the ability of some payees to complete properly (Kutner, 2007).

The NRC committee performed a valuable service in conducting its study of misuse of benefits, and pointing out new approaches to detect misuse in a more focused manner. The statute defines misuse in this way: “Misuse occurs in any case in which the representative payee receives payment under this title for the use and benefit of another person and converts such payment, or any part thereof, to a use other than for the use and benefit of such other person.”

SSA has stated in the past that misuse is extremely rare and has been found to be less than 0.01 percent of cases (SSA testimony, September 9, 2003). The NRC committee’s in-depth study of misuse found that misusers were about 0.2 percent of individual payees, still a small percentage, but considerably higher than the SSA estimate. Despite the simplicity of the definition of misuse, it is sometimes difficult to determine it in practice. It is difficult to determine misuse in the absence of records, so the fact that the NRC committee also found that only about two-thirds of payees reported keeping records makes estimating the extent of misuse even more problematic.

SSA uses three major methods to detect misuse: reports from beneficiaries or third parties, small random samples conducted by SSA’s Office of the Inspector General, and the annual accounting form. The NRC committee concluded that none of these was effective in detecting misuse.

Before 1983, SSA created an accounting system on its own initiative, as it did not then have a mandate to conduct accountings of funds that payees received on behalf of beneficiaries. In 1983, however, the decision in a class action suit said that all payees should be required to give a full accounting of how they spend and save Title II and Title XVI benefits on behalf of beneficiaries. Subsequently, Congress required that all payees, except state mental institutions participating in the on-site review program, submit an accounting report annually.

The annual accounting form tells payees the amount of benefits paid during the year being accounted for and asks them to state the amount spent on various categories and the amount saved. They are told not to submit receipts, but to retain them for two years. SSA accepts the figures submitted by the payee as long as the total amount spent and saved equals or exceeds 90 percent of the amount received. Sending, collecting, and reviewing this information is a large expenditure of effort that yields little useful result in detecting misuse.

The methods SSA is currently using are not effective in detecting misuse, and new approaches are needed. The NRC committee’s study used data elements from SSA’s records (for example, payee is a non-relative, or payee does not live with beneficiary) to identify payee characteristics that would help target potential misusers. That approach is similar to the profiling that SSA has used for redeterminations and continuing disability reviews to find cases in which erroneous payments were most likely. A study done by SSA’s Office of the Inspector General found that the characteristics identified by NRC should be used to identify representative payees who have a high risk of misuse. The study also found that the characteristics were reliable indicators of poor performance, other than misuse, by payees (SSA, Office of the Inspector General,

Characteristics). SSA has used those characteristics to develop profiles for identifying representative payees with a higher probability of misusing benefits.

We urge SSA to continue its work along these lines and revise its annual accounting form to obtain additional information on payee characteristics that would help evaluate risk factors and payee performance. As the committee wrote, “No form, by itself, is going to detect program misuse. However, if a form can be used to obtain information on characteristics of interest, it could then be combined with a rigorous program of audits.” Other work on financial abuse has stressed the need to examine characteristics of the victims of abuse as well as the perpetrators in an effort to better understand risk factors (Rabiner et al., Hafemeister). We recommend that SSA commit research staff to ongoing work on representative payee issues, including examining characteristics of payees in combination with those of beneficiaries in order to target its selection and monitoring activities in the most efficient way. SSA is working on improving its data systems for representative payees, and doing so will provide more useable data for analysis. It should also test the use of external data sources, such as data exchanges with other agencies, credit bureaus, and criminal justice records.

Once SSA has established criteria for data-driven selection and monitoring, it should carry out its annual accounting in a way that is tailored to different risk groups, monitoring high risk groups more carefully.

Recent reports of exploitation of a group of beneficiaries point out the need for paying special attention to cases in which payees have an interest that conflicts with the best interests of the beneficiary. In February 2009, inquiries by a sister of a beneficiary led to a series of inspections at a boarding facility in Iowa. The fire marshal ordered the facility closed, and the 21 residents were moved to a state-licensed care facility. The men’s employer has become the focus of an investigation involving several state and federal agencies. That investigation has shown that for 34 years, a Texas company sent men with intellectual disabilities from Texas to Iowa to work in a poultry-processing plant. The men were working for about 40 cents an hour and lived in a century-old building that was leased to their employer for $600 per month. Each of the men was reported to be receiving a Social Security disability benefit (SSI and/or SSDI), averaging about $640 per month. These benefit payments were managed by their employer, who was also their payee and their landlord and “care” provider. The employer was reported to charge the men all but $60 to $70 of their total income for room, board and “kind care.” The sister of one of the men stated that he had $80 in the bank after working for 30 years (Kauffman February 8 and 10, 2009; Jones).

SSA’s accounting forms are not designed to uncover this kind of abuse. As long as the figures on the accounting forms showed that the benefits were being used to meet the needs of the beneficiaries, and the figures added up, no further action would be taken. To its credit, however, SSA has taken action to investigate whether there are other situations in which representative payees are also employers and beneficiaries are vulnerable to exploitation. SSA has compiled a database of payees who also employ their beneficiaries. It reviewed 328 such employers in FY 2009 and referred two potential wage violations to the Department of Labor. It also entered into a contract with the National Disability Rights Network to pay for on-site reviews to be conducted by investigators for state Protection and Advocacy agencies. SSA’s Inspector General plans to examine a sample of the reviews to determine whether they complied with SSA’s policies and procedures (Kauffman, December 27, 2009; SSA, Briefing for the Social Security Advisory Board, January 12, 2010; SSA, Office of the Inspector General, Congressional Response Report, May 2010).

There are other situations that call for similar attention. The NRC report pointed out the conflict of interest when a representative payee was also the operator of a group home, foster care home or board and care home, providing food, shelter and, ostensibly, services to the beneficiary while controlling the person’s benefit. Some states monitor and/or license some or all of these facilities and have rules for fiscal management of benefits. In other states, the payee is free to charge any amount and deduct it from the benefit payment. The committee found cases in which the payee charged beneficiaries receiving different benefit amounts the entire benefit amount for room and board. Some of these payees could provide records and were complying with reporting standards, although they may have been exploiting their beneficiaries. In addition they may not have been in compliance with Social Security regulations and policy that address the expectation that payees will also provide for a beneficiary’s personal needs, and clothing, even if that means a facility gets paid a little less than is usual (CFR 20, 404.204 Use of benefit Payments, and POMS, GN00602.001, Use of Benefits, 2. Proper Use of Benefits).

A 2009 study by SSA’s Office of the Inspector General underlined the need to pay greater attention to payees who have a creditor relationship because their beneficiaries reside in a group home that the payee operates. That study examined a sample of payees to determine if some of them operated as group homes. Since current law requires SSA to conduct periodic reviews of individual payees serving 15 or more beneficiaries, OIG looked at payees who served 14 or fewer beneficiaries. To focus more closely on potential group homes, it further restricted its sample to payees with at least three beneficiaries who were not relatives. In a sample of 16 payees, it found 3 group homes, 3 beneficiaries whose clothing or shelter needs were not being met, and 3 payees charging unauthorized fees (SSA, OIG,

Individual Representative Payees Serving Multiple Beneficiaries and

Organizational Representative Payee Serving as an Individual Representative Payee in Philadelphia). Since in this small sample, the OIG study found a substantial percentage of group homes (and therefore creditor relationships that the agency had not been aware of) and violations of SSA policy, SSA should pursue further investigations along these lines.

SSA should increase its monitoring of individual payees, such as operators of group homes, who are also in a creditor relationship with the beneficiary, and should develop performance and reporting standards specifically for this type of payee. Whenever possible, SSA should avoid putting beneficiaries in a position where their payees’ interest conflicts with their own best interest. The agency may have difficulty identifying payees who are also creditors, given the state of its data system, but it is updating that system. It should obtain the data it needs, develop performance and reporting standards, and move toward enforcing them to the best of its ability.

Applicants who want to be selected as representative payees currently complete the application in a face-to-face interview in most cases. SSA’s program instructions direct interviewers to use the interview to determine the applicant’s qualifications and motive for filing to be a payee, to judge the applicant’s ability to carry out the payee’s responsibilities, and to explain the payee’s duties, reporting responsibilities, and liability of non-compliance of reporting (SSA, Program Operations Manual System, GN 00502.113).

The program instructions also state: “SSA is legally required to verify identity and SSN information supplied by payee applicants. Verifying other allegations such as income and custody may also help determine a payee applicant’s suitability.” The instructions also provide payee preference lists. For example, the preference list for minor children begins with a parent with custody, a legal guardian, a parent without custody but who shows strong concern, and goes on through five more categories. The instruction states that the lists are meant only as guidelines and that each payee application must be evaluated to determine the best payee (SSA, Program Operations Manual System, GN 00502,105, GN 00502.117).

Just as data on payee characteristics can help with misuse, as described above, they can also help in payee selection. SSA should use its data on payee characteristics to shape its policies on selection of payees. The data that it is developing, and should continue to develop, on payee characteristics that are linked to misuse should be built into its payee selection. SSA should also take advantage of other data that are available to it, such as credit reports, criminal records, and information from other public agencies. It should use data from these sources as it uses the information on payee characteristics from its own records and analyze it for potential links to payee misuse that can improve its selection and monitoring of payees.

SSA should also avoid giving control of beneficiaries’ funds to someone who is not designated as a payee. SSA’s Office of the Inspector General looked into the use of “in care of” addresses to gain control of benefit payments while avoiding representative payee reporting. It found that 216,000 beneficiaries had addresses “in care of” someone else. OIG auditors visited 21 nursing homes and other facilities. It found that at five of them, the staff acknowledged the beneficiaries retained no control over, or had no access to, SSA payments. Once the “in care of” address changes were made, SSA would mail payments directly to the facility or electronically deposit funds into accounts controlled by the facility. This gave the facility control over the benefits without the responsibility that comes with being representative payee (SSA, OIG,

Beneficiary and Recipient Use of “In Care of” Addresses).

Once they are selected, some payees will need support from SSA. The most common reasons for payees to contact SSA for help have been to clarify the beneficiary’s benefit amount, to understand the payee’s responsibilities, and to request permission to allow the beneficiary to manage his or her own benefits. The NRC’s survey found that, of those who did contact SSA with questions or concerns, nearly a quarter felt somewhat (9.3 percent) or very (14.5 percent) dissatisfied with the help they had received. Payees perform an important service, and many of them may have difficulty understanding or following the instructions they receive when they are appointed. Since the NRC report, SSA has done an assessment of payee needs and plans to evaluate its publications and enhance its website for payees. It has also made it possible for payees to file the annual accounting form online. It should continue to find out what kinds of help payees need and make sure they have the information and support that will help them fulfill their responsibilities to both beneficiaries and SSA.

SSA’s field staff also needs additional support in fulfilling its responsibilities. The NRC committee reported that during its field visits, some field office staff said that they did not have adequate methods to judge whether a prospective new payee was more suitable than the current payee. Field office staff stated that they did not have means to verify information given by prospective payees. The Advisory Board has heard similar comments during its visits to SSA field offices. Since field offices no longer have field representatives who can visit beneficiaries, they are limited in their ability to determine whether benefits are being used to meet the beneficiaries’ needs. SSA has recently conducted training for its field managers and staff on payee issues, and it plans to conduct additional training. SSA should also analyze the needs of its front-line employees in addition to training, and then provide them with the tools they need to do their job well.

The NRC committee’s study of misuse found individual payees who were given fees by a beneficiary for their services, in violation of SSA policy (NRC, 2007). Only organizational payees are allowed to charge a fee. Other researchers have also found that individual payees charge the beneficiary fees (Gallmeier and Levy). Individual payees are not authorized to collect fees, and doing so is misuse. The current accounting form for individual payees does not ask about this. The next revision of the form should ask if the payee charges a fee.

At a Congressional hearing in 2000, SSA’s Inspector General said of representative payee oversight, “This is a workload [at] Social Security, in the field, that gets deferred. It is not addressed because there are other priorities that interfere. We do not have a performance measure in our performance plan that deals with having this process as effective and having the best integrity that it possibly could. And in my opinion, where you do not have a performance measure, normally in life, you do not have much compliance or an incentive. So we think that is probably called for, also.” Later, referring to a large case of representative payee fraud, he said “this particular situation happens when this focus, this stewardship, if you will, of this particular area was not important. What was more important was to get benefits out the door.” (Huse, 2000). A letter from the National Council of Social Security Management Associations, which represents SSA’s front-line management, indicated that payee activities were still backlogged in 2008 and explained, “Suffice it to say that some of these workloads are of low priority or end up backlogged simply because they are not being monitored as closely as others” (NCSSMA).

As an external advisory committee on representative payees recommended to SSA in 1996, SSA should implement a quality review sample to examine the quality of SSA determinations of beneficiaries’ capability to handle benefits, payee selections, and misuse determinations. The quality review should also supplement payee self-reporting with collecting collateral evidence to support the payee’s statements. Such a quality review would indicate to front-line staff that the agency considers representative payee issues an important workload. At the same time, it would collect data and identify trends that might suggest the need for further policy changes. There should also be continued management attention to agency performance of its duties related to representative payees.

The fact that the NRC study was limited to individual payees serving fewer than 15 beneficiaries and non-fee-for-service organizational payees serving fewer than 50 beneficiaries does not mean that the broader organizational payee program is without problems.

The Social Security Protection Act of 2004 required SSA to expand its monitoring of certain representative payees, including organizational payees representing 50 or more beneficiaries (known as volume payees) and all payees authorized to collect a fee for service. SSA’s monitoring program includes reviews of all volume payees and fee-for-service payees and all state mental institutions at least once every three years. SSA also selects a random sample of payees not scheduled for a triennial site review in that year. In addition, SSA conducts targeted reviews as needed if events raise concerns about a payee’s performance. Payee reviews include meetings with representatives from the organizations, assessments of the payees’ recordkeeping, and interviews with beneficiaries.

In FY 2002, a consultant reviewed SSA’s site review process for fee-for-service, large organizational payees serving over 100 beneficiaries, and individual payees serving over 20 beneficiaries. The site review focuses on communicating SSA’s expectations of representative payees, and discussing what payees need from SSA to perform their functions. Site reviewers also examine documentation to check beneficiary resources and ensure that interest on conserved funds is credited to the beneficiary’s account. They also check to ensure that accounting forms have been returned, that conserved funds have been returned if a new payee has been appointed, that any overpayments have been repaid, and that only appropriate fees have been charged. The consultant’s report found that in general the site review process was very effective, but it noted that the site reviews were not financial or accounting audits, and that even a financial audit could not ensure against fraud (Chesapeake Consulting).

More recently, an audit report by SSA’s Office of the Inspector General showed one aspect of the potential for misuse by organizational payees. In 2007, SSA’s Office of the Inspector General examined a sample of 139 organizational payees that received 3 or more benefit payments after the deaths of beneficiaries between January 2000 and May 2006. Of the 139 organizations in its sample, it found that 76 did not timely report the deaths of multiple beneficiaries and/or did not return funds that were incorrectly paid after death, despite SSA’s efforts to recover the benefits. Projecting from its sample, OIG estimated that SSA paid about 2,780 organizational payees $10 million in benefits after the deaths of beneficiaries (SSA, OIG,

Organizational Representative Payees).

In the last ten years, SSA’s Office of the Inspector General has issued audit reports on ten of the approximately 1,200 fee-for-service payees. Among the problems these audits uncovered were: holding large amounts of conserved funds in uninsured, non-interest bearing accounts; accepting incorrect payments after the death of beneficiaries; charging excessive fees; having only limited contact with their beneficiaries; not keeping adequate records showing how funds were spent; commingling other funds with benefit funds; and not returning conserved funds for beneficiaries no longer in the payee’s care.

These OIG audit reports indicate that, while site reviews are helpful, they do not fulfill SSA’s stewardship responsibility to manage benefit payments in a way that maintains the trust of the public it serves. The Office of the Inspector General should conduct annually a review of a sample of site visits and provide feedback to SSA to ensure that future site visits are as effective as possible in preventing misuse and ensuring compliance with SSA policies. Attention should be directed to whether or not beneficiaries actually receive the personal needs money they are supposed to receive, and whether or not what rep payees report on paper about their management of beneficiary funds reflects actual practice.

The payment of fees is another issue that requires attention. Legislation in 1990 first allowed qualified organizations to charge a fee. The fee is deducted from the beneficiary’s payment and is used for expenses incurred by the organization in serving as payee. The maximum fee was originally set at $25 and stayed at that amount through 1996. It was later indexed to the cost of living. Fee-for-service payees are now entitled to collect the lesser of $37 or 10 per cent of the monthly benefit amount per month from each beneficiary whose benefits they manage. Payees for beneficiaries who have a medically determinable substance abuse disorder as a secondary diagnosis are entitled to a higher fee, the lesser of $72 or 10 percent of the monthly benefit amount per month from each beneficiary. Fee-for-service payees are last on SSA’s preference list for selection of payees and are generally selected only when no other suitable payee can be found.

SSA currently has 1,201 fee-for-service payees providing services to 96,096 SSI beneficiaries, of whom 2,172 have a substance abuse disorder as a secondary diagnosis. If each of these payees received the maximum amount, the total of fees paid for a year would be $44 million. In the context of a program that distributes $40 billion per year in Federal benefits, that may not be considered a large amount. On the other hand, for a beneficiary with a Federal benefit rate of $674 per month, a fee of $37 or $72 is a large amount. Since the SSI monthly benefit is below the poverty level to begin with and since it is not the beneficiaries’ choice to have a fee-for-service payee, it seems unreasonable to require beneficiaries to pay the payee’s fee. What we do not know, however, is the impact of the fee on beneficiaries who may be receiving other benefits to help pay the cost of food, shelter, and other necessities. We therefore recommend that OIG examine a sample of beneficiaries with fee-for-service payees to see how the payee’s fee impacts meeting their food, shelter, and personal needs.

The population of representative payees overlaps with populations that are monitored by other agencies, but there is little coordination of oversight, or sharing of information. A 2006 report on guardianship by the Government Accountability Office said, “With few exceptions, courts and federal agencies don’t systematically notify other courts or agencies when they identify someone who is incapacitated, nor do they notify them if they discover that a guardian or a representative payee is abusing the person. This lack of coordination may leave incapacitated people without the protection of responsible guardians and represen

tative payees or, worse, with an identified abuser in charge of their benefit payments.” (GAO, 2006).

In 2006, an AARP Roundtable on Representative Payees and Guardianship, with representatives from the Department of Veterans Affairs (VA) and SSA and state court judges, generated ideas for improving coordination (Karp and Wood):

A recent audit report by SSA’s Inspector General shows the potential for better use of existing information. When a child is placed in a state’s foster care system, authorized state partners can use SSA’s State Verification and Exchange System to find out whether the child is receiving benefits from SSA and can apply to become the child’s representative payee. The Inspector General compared foster care records of the state of Maryland with SSA’s beneficiary records and found that 952 children in Maryland’s foster care programs were receiving SSA benefits for which they had representative payees. Of that number, 402 children had payees who were neither foster care agencies nor the children’s foster care parents. SSA selected 50 of those 402 to assess the suitability of their representative payees. Of those 50, SSA determined that six representative payees had misused and four had possibly misused the children’s benefits (SSA, Office of Inspector General,

Benefit Payments).

The priority here should be to work with VA to establish a way that the agencies can inform one another of problematic payees. SSA should also develop working relationships on payee matters with state adult protective services, the state protection and advocacy agencies, the Area Agencies on Aging, the growing number of Aging and Disability Resource Centers, and state foster care agencies, to determine what information can be shared usefully. To the extent possible, information should be shared through automated data exchanges. All of these agencies have interests that overlap with SSA’s, and exchanges of data would be mutually beneficial in sharing information on payees who have misused benefits and preventing misuse for the clients of all the organizations involved.

SSA has been taking steps to improve its representative payee process. We encourage the agency to continue along these lines, using data to focus its efforts where they will be most useful. Our additional recommendations are:

Chesapeake Consulting, Inc. Social Security Administration Organizational Representative Payee Program Site Review, March 5, 2002.

Federal Security Agency, Fifth Report of the Social Security Board, 1940.

Government Accountability Office, Guardianships: Little Progress in Ensuring Protection for Incapacitated Elderly People, GAO-06-1086T, September 7, 2006

Hafemeister, Thomas L., “Financial Abuse of the Elderly in Domestic Settings,” in Richard J. Bonnie and Robert B. Wallace (eds.),

Elder Mistreatment: Abuse, Neglect, and Exploitation in an Aging America. Washington: National Academies Press, 2002.

Jones, Gregg, “Texas farm that employed mentally disabled faces more scrutiny after Iowa facility's shutdown,” Dallas Morning News, June 7, 2009.

Karp, Naomi and Erica Wood, Guarding the Guardians: Promising Practices for Court Monitoring. AARP Public Policy Institute, 2007.

Kutner, Mark, et al., Literacy in Everyday Life: Results from the 2003 National Assessment of Adult Literacy, U.S. Department of Education, 2007.

National Research Council. Improving the Social Security Representative Payee Program: Serving Beneficiaries and Minimizing Misuse. Committee on Social Security Representative Payees, Division of Behavioral and Social Sciences and Education. Washington: The National Academies Press, 2007.

Social Security Administration. Annual Statistical Supplement to the Social Security Bulletin.

Social Security Administration, Program Operations Manual System.

Social Security Administration. SSI Annual Statistical Report, 2008. September 2009.

Social Security Administration, Office of the Inspector General, Beneficiary and Recipient Use of “In Care of” Addresses, A-06-08-18015, August 2008.

Social Security Administration, Office of the Inspector General, Benefit Payments Managed by Representative Payees of Children in Foster Care, A-13-07-17137, June 2010.

Social Security Administration, Office of the Inspector General, Characteristics of Representative Payees that May Increase the Risk of Benefit Misuse, A-09-08-38055, August 2009.

Social Security Administration, Office of the Inspector General. Congressional Response Report: Representative Payees who Employ Beneficiaries or Provide Employment Services, A-13-10-11013, March 2010.

Social Security Administration, Office of the Inspector General. Congressional Response Report: The Social Security Administration’s Oversight of Employer Representative Payees, A-13-10-20125, May 2010.

Social Security Administration, Office of the Inspector General. Congressional Response Report: The Social Security Administration’s Oversight of Representative Payees, A-13-09-29141, June 2009.

Social Security Administration, Office of the Inspector General. Individual Representative Payees Serving Multiple Beneficiaries. A-13-08-28089, July 2009.

Social Security Administration, Office of the Inspector General, Monitoring Representative Payee Performance: Misuse of Benefits, A-09-96-64203, September 1996.

Social Security Administration, Office of the Inspector General, Organizational Representative Payee Serving as an Individual Representative Payee in Philadelphia, Pennsylvania, A-03-09-29094, September 2009.

Social Security Administration, Office of the Inspector General. Organizational Representative Payees Reporting Beneficiaries’ Deaths, A-01-06-15068, April 2008.

Social Security Administration, Office of the Inspector General. Sunshine Payee Corporation, a Fee-for-Service Representative Payee for the Social Security Administration, A-08-09-29106, February 2010.

SSA, SSI Annual Statistical Report, 2009, tables 12 and 28.