These measures are expressed as percentages of taxable payroll, as percentages of GDP, or in dollars.

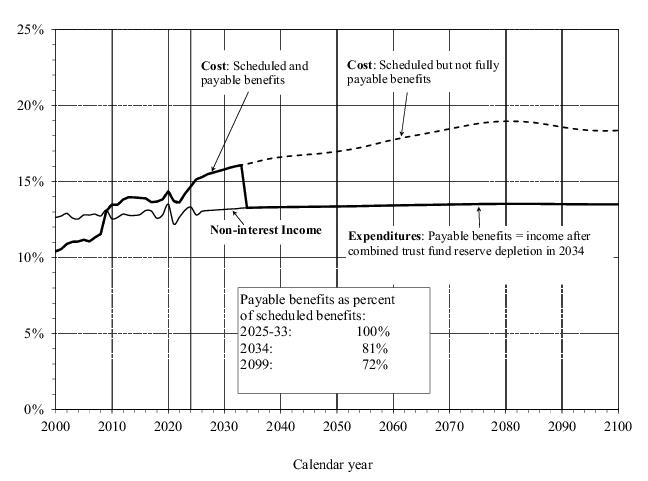

1 Figure II.D2 illustrates the year-by-year relationship among OASDI income (excluding interest), cost (including scheduled benefits), and expenditures (including payable benefits) starting in 2000 and for the full 75-year projection period, which is 2025 through 2099. The figure shows all values as percentages of taxable payroll.

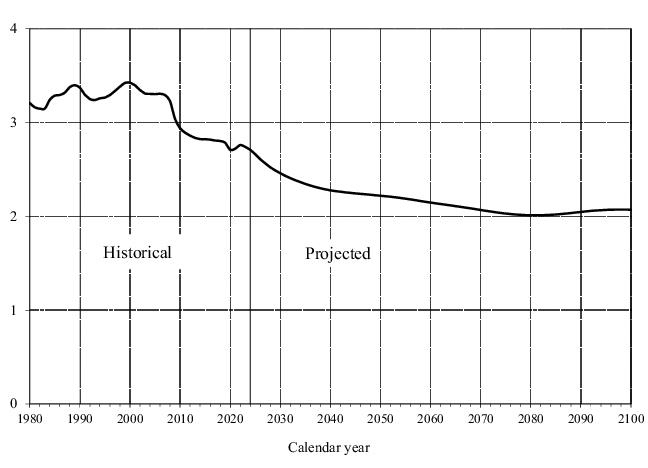

Figure II.D3 shows the estimated number of covered workers per OASDI beneficiary. Figures

II.D2 and

II.D3 illustrate the inverse relationship between cost rates and the number of workers per beneficiary. In particular, the projected future increase in the cost rate reflects a projected decline in the number of covered workers per beneficiary. There were about 2.7 workers for every OASDI beneficiary in 2024.

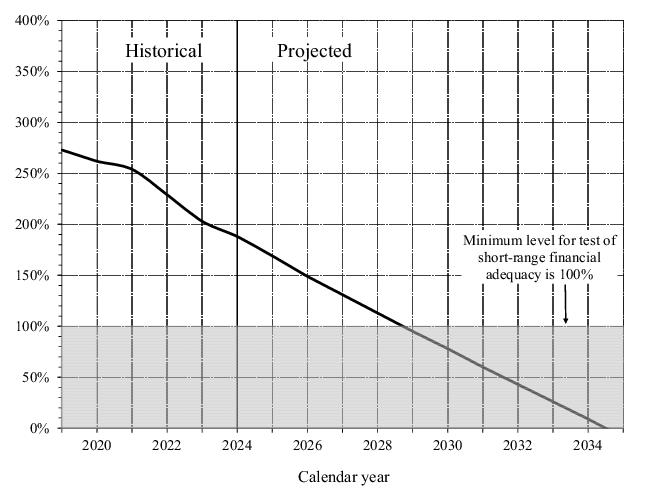

Table II.D1 displays the projected maximum trust fund ratios during the long-range period for the OASI, DI, and combined OASI and DI funds. The table also shows the year of maximum projected trust fund ratio during the long-range projection period (2025 through 2099) and the year of trust fund reserve depletion.

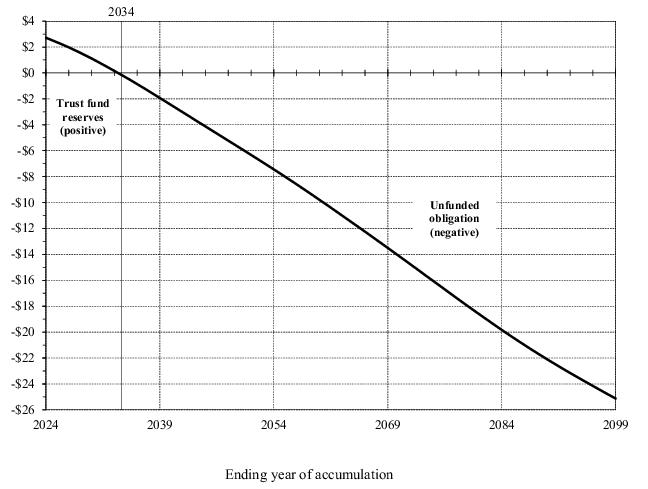

Another way to illustrate the OASDI program’s projected financial shortfall is to examine the cumulative present value of scheduled income less cost. Figure II.D5 shows the present value of cumulative OASDI income less cost from the program’s inception through each of the years from 2024 to 2099. A positive value represents the present value of trust fund reserves at the end of the selected year. A negative value is the unfunded obligation through the selected year.

Figures II.D2,

II.D4, and

II.D5 show that the program’s actuarial status will deteriorate throughout the projection period if current law is not altered. Negative annual balances and increasing cumulative shortfalls toward the end of the 75-year period indicate the additional change that will be needed by then in order to maintain solvency beyond 75 years. Consideration of summary measures alone for a 75‑year period can lead to incorrect perceptions and to policy prescriptions that do not achieve sustainable solvency.

2

Appendix F presents summary measures over the infinite horizon. The infinite horizon values provide an additional indication of Social Security’s actuarial status extending indefinitely into the future, but results are subject to much greater uncertainty. Extending the horizon beyond 75 years increases the measured unfunded obligation. Through the infinite horizon, the unfunded obligation is equivalent to

5.2 percent of future taxable payroll or 1.6 percent of future GDP.

Figure

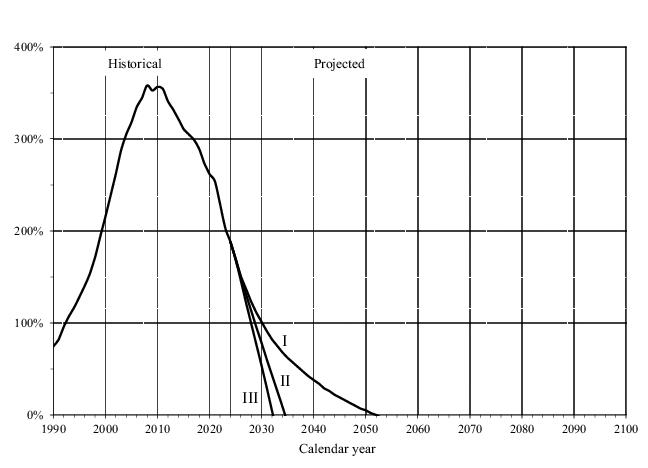

II.D6 shows the projected trust fund ratios for the combined OASI and DI Trust Funds under the intermediate, low-cost, and high-cost assumptions. The figure indicates that the combined trust funds are projected to become depleted in 2034 under the intermediate alternative, in 2051 under the low-cost alternative, and in 2032 under the high-cost alternative.

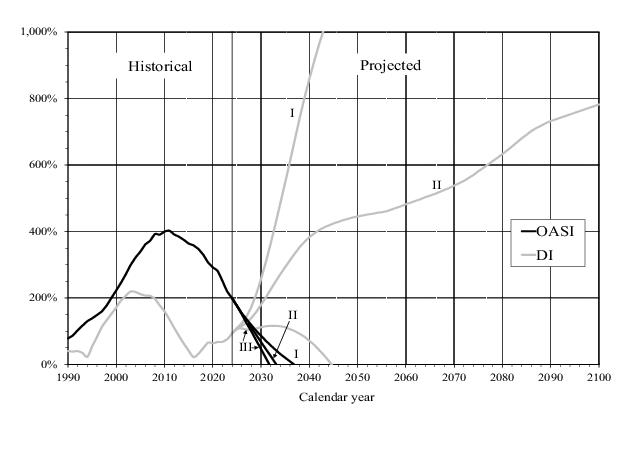

Figure II.D7 shows the projected trust fund ratios separately for OASI and DI Trust Funds under the intermediate, low-cost, and high-cost assumptions. OASI reserves are projected to become depleted in 2033 under the intermediate alternative, in 2036 under the low-cost alternative, and in 2031 under the high-cost alternative. The DI reserves are projected to become depleted in 2044 under the high-cost alternative. They are not projected to become depleted under the low-cost and intermediate alternatives. This figure illustrates that OASI reserves are expected to become depleted much sooner than DI reserves, potentially within the next 10 years.

Appendix D of this report presents a second approach using long-range sensitivity analysis for the OASDI program. By varying one parameter at a time, sensitivity analysis provides a way to illustrate the uncertainty surrounding projections into the future.

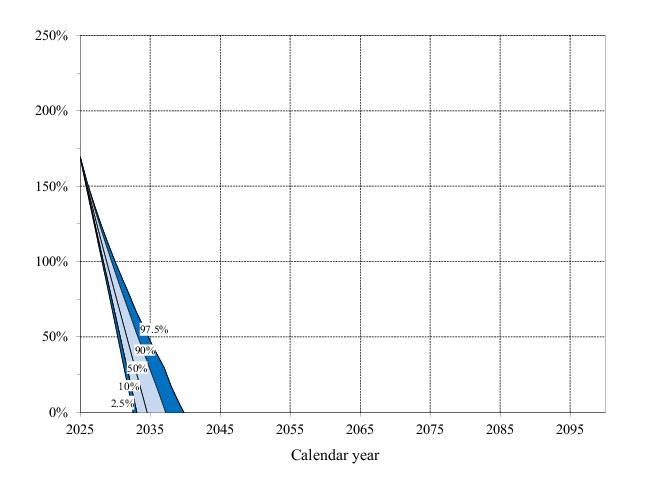

The results of the stochastic simulations, discussed in more detail in appendix E, suggest that trust fund reserve depletion before mid-century is very likely. In particular, figure

II.D8 indicates that for 95 percent of these simulations, the reserve depletion year falls within the range from 2032 to 2039. In last year’s report, this range was from 2032 to 2043.

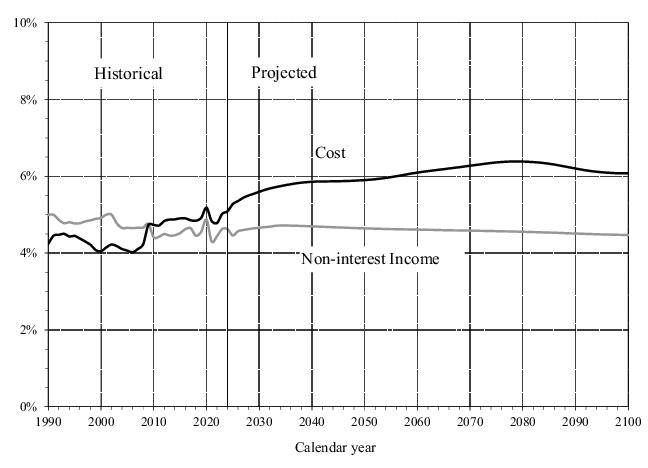

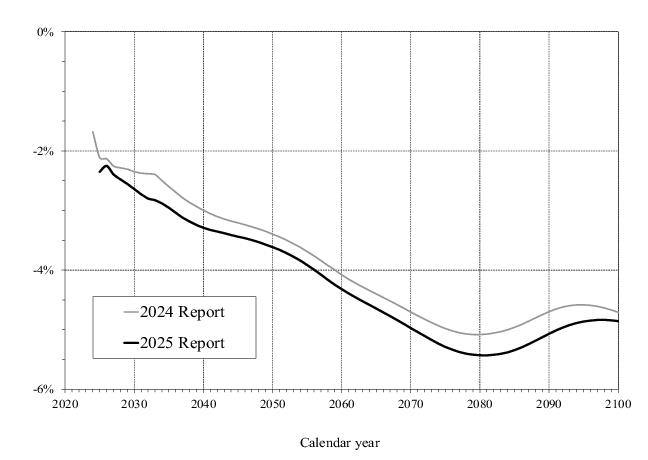

Figure II.D9 compares this year’s projections of annual balances (non-interest income minus cost) to those in last year’s report. The annual balances in this year’s report are lower (more negative) in all projection years. For the full 75-year projection period, the annual balances average 0.28 percentage point lower in this year’s report.