Summarized measures for any period indicate whether projected income is sufficient, on average, for the whole period. Summarized measures can only indicate the solvency status of a fund for the end of the period. The Trustees summarize the total income and cost over valuation periods that extend through 75 years and over the infinite horizon

1. This section presents two summarized measures: (1) the actuarial balance; and (2) the open group unfunded obligation. The actuarial balance indicates the size of any surplus or shortfall as a percentage of the taxable payroll over the period. The open group unfunded obligation indicates the size of any shortfall in present-value dollars.

Table IV.B1 presents a comparison of the estimated annual income rates and cost rates by trust fund and alternative. Table

VI.G8 shows detailed long-range projections of trust fund operations in current dollar amounts.

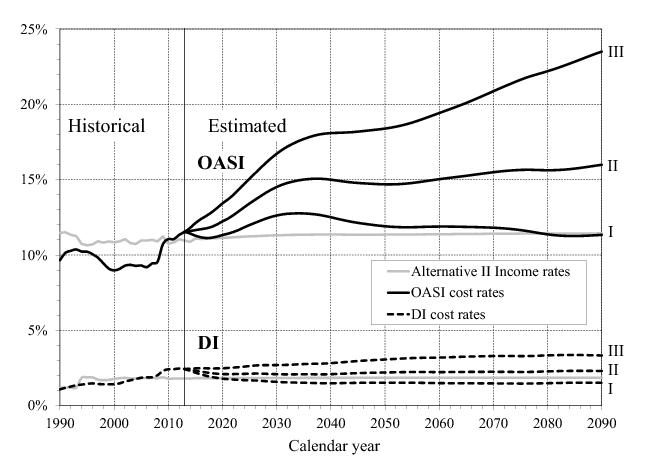

Under the intermediate assumptions, the Trustees project that the OASI income rate will rise at a very gradual rate from 10.87 percent of taxable payroll for 2014 to 11.43 percent for 2088. Income from taxation of benefits causes this increase for two main reasons: (1) total benefits are rising faster than payroll; and (2) the benefit-taxation threshold amounts are fixed (not indexed), and therefore an increasing share of total benefits will be subject to tax as incomes and benefits rise. The pattern of the cost rate is much different. The OASI cost rate is projected to increase relatively slowly from 11.58 percent of payroll for 2014 to 11.86 percent of payroll for 2018, as the economic recovery through this period largely offsets the effects of the aging population. From 2018 to 2035, the cost rate rises rapidly because the retirement of the

baby-boom generation will increase the number of beneficiaries much faster than the number of workers increases, as subsequent lower-birth-rate generations replace the baby-boom generation at working ages. From 2037 to 2051, the cost rate declines because the aging baby-boom generation is gradually replaced at retirement ages by historically low-birth-rate generations born between 1966 and 1989, causing the beneficiary-to-worker ratio to decline. After 2051, the projected OASI cost rate generally rises slowly, reaching 15.88 percent of taxable payroll for 2088, primarily because of projected reductions in death rates.

Figure IV.B1 shows the patterns of the OASI and DI annual cost rates. Annual DI cost rates rose substantially between 1990 and 2010 in large part due to: (1) aging of the working population as the baby-boom generation moved from ages 25-44 in 1990, where disability prevalence is low, to ages 45-64 in 2010, where disability prevalence is much higher; (2) a substantial increase in the percentage of women insured for DI benefits as a result of increased and more consistent rates of employment; and (3) increased disability incidence rates for women to a level similar to those for men by 2010. After 2010, all of these factors stabilize, and therefore the DI cost rate stabilizes also. Annual OASI cost rates follow a similar pattern to that for DI, but displaced 20 to 25 years later, because the baby-boom generation enters retirement ages 20 to 25 years after entering prime disability ages. Figure

IV.B1 shows only the income rates for alternative II because the variation in income rates by alternative is very small. Income rates generally increase slowly for each of the alternatives over the long-range period. Taxation of benefits, which is a relatively small portion of income, is the main source of both the increases in the income rate and the variation among the alternatives. Increases in income from taxation of benefits reflect: (1) increases in the total amount of benefits paid; and (2) the increasing share of individual benefits that will be subject to taxation because benefit taxation threshold amounts are not indexed.

Figure IV.B1 shows the patterns of the annual balances for OASI and DI. For each alternative and for historical data, the magnitude of each of the positive balances, as a percentage of taxable payroll, is the distance between the appropriate cost-rate curve and the income-rate curve above it. The magnitude of each of the deficits is the distance between the appropriate cost-rate curve and the income-rate curve below it. Annual balances follow closely the pattern of annual cost rates after 1990 because the payroll tax rate does not change for the OASDI program, with only small variations in the allocation between DI and OASI. The pattern of the projected OASDI annual balances is important to the analysis of the financial condition of the Social Security program as a whole.

Long-range OASDI cost and income are most often expressed as percentages of taxable payroll. However, the Trustees also present cost and income as shares of gross domestic product (GDP), the value of goods and services produced during the year in the United States. Under alternative II, the Trustees project the OASDI cost to rise from 4.92 percent of GDP for 2014 to a peak of 6.16 percent for 2037. After 2037, OASDI cost as a percentage of GDP declines to a low of 5.96 percent for 2052 and thereafter generally increases slowly, reaching 6.12 percent by 2088. Appendix

G presents full estimates of income and cost relative to GDP.

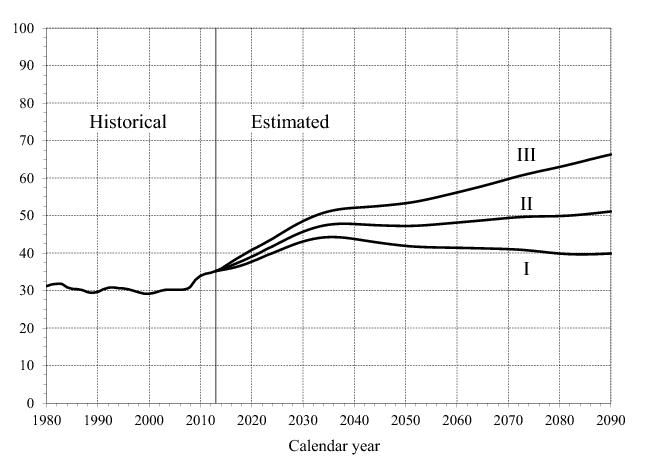

The effect of the demographic shift under the three alternatives on the OASDI cost rates is clear when one considers the projected number of OASDI beneficiaries per 100 covered workers. Compared to the 2013 level of 35 beneficiaries per 100 covered workers, the Trustees project that this ratio rises to 48 by 2035 under the intermediate assumptions because the growth in beneficiaries greatly exceeds the growth in workers. By 2090, this projected ratio rises further under the intermediate and high-cost assumptions, reaching 51 under the intermediate assumptions and 66 under the high-cost assumptions. Under the low-cost assumptions, this ratio rises to 44 by 2035 and then declines, reaching a stable level of about 40 after 2076. Figure

IV.B2 shows beneficiaries per 100 covered workers.

For each alternative, the curve in figure IV.B2 is strikingly similar to the corresponding cost-rate curve in figure

IV.B1. This similarity emphasizes the extent to which the cost rate is determined by the age distribution of the

population. The cost rate is essentially the product of the number of beneficiaries and their average benefit, divided by the product of the number of covered workers and their average taxable earnings. For this reason, the pattern of the annual cost rates is similar to that of the annual ratios of beneficiaries to workers.

Table IV.B2 also shows the number of covered workers per OASDI beneficiary, which was about 2.8 for 2013. Under the low-cost assumptions, this ratio declines to 2.3 by 2035, and then generally rises throughout the remainder of the period, reaching 2.5 by 2090. Under the intermediate assumptions, this ratio declines generally throughout the long-range period, reaching 2.1 for 2035 and 2.0 by 2090. Under the high-cost assumptions, this ratio decreases steadily to 1.5 by 2090.

The trust fund ratio serves an additional important purpose in assessing the actuarial status of the program. If the projected trust fund ratio is positive throughout the period and is either level or increasing at the end of the period, then projected adequacy for the long-range period is likely to continue for subsequent reports. Under these conditions, the program has achieved sustainable solvency.

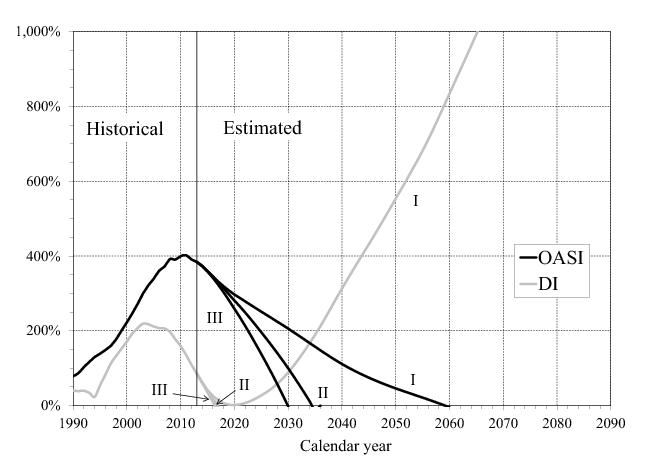

3Table IV.B3 shows the Trustees’ projections of trust fund ratios by alternative, without regard to advance tax transfers that would be effected, for the separate and theoretical combined OASI and DI Trust Funds. The table also shows the years of trust fund reserve depletion and the percentage of scheduled benefits that would be payable thereafter, by alternative.

The test of long-range close actuarial balance for each trust fund requires meeting two conditions: (1) the short-range test of financial adequacy is satisfied; and (2) the trust fund ratios stay above zero throughout the 75-year projection period, allowing scheduled benefits to be paid in a timely manner throughout the period. As discussed in section IV.A, the DI Trust Fund fails the short-range test of financial adequacy under the intermediate assumptions because trust fund reserves become depleted in the fourth quarter of 2016. Under the intermediate assumptions, the OASI trust fund reserves become depleted in 2034, and the combined OASI and DI trust fund reserves become depleted in 2033. Therefore, the OASI, DI, and combined OASI and DI Trust Funds all fail the long-range test of close actuarial balance.

Figure IV.B3 illustrates the trust fund ratios for the separate OASI and DI Trust Funds for each of the alternative sets of assumptions. DI Trust Fund status is more uncertain than OASI Trust Fund status because there is a high degree of uncertainty associated with future disability prevalence. A graph of the trust fund ratios for the combined trust funds appears in figure

II.D7.

Table IV.B4 presents summarized income rates, summarized cost rates, and actuarial balances for 25-year, 50-year, and 75-year valuation periods. Summarized income rates are the sum of the present value of non-interest income for a period (which includes scheduled payroll taxes, the projected income from the taxation of scheduled benefits, and reimbursements from the General Fund of the Treasury) and the starting trust fund asset reserves, expressed as a percentage of the present value of taxable payroll over the period. Under current law, the total OASDI payroll tax rate will remain at 12.4 percent in the future. In contrast, the Trustees expect income from taxation of benefits, expressed as a percentage of taxable payroll, to increase in most years of the long-range period for the two reasons discussed earlier on

page 54. Summarized cost rates are the sum of the present value of cost for a period (which includes scheduled benefits, administrative expenses, net interchange with the

Railroad Retirement program, and payments for vocational rehabilitation services for disabled beneficiaries) and the present value of the cost of reaching a target trust fund of 100 percent of annual cost at the end of the period, expressed as a percentage of the present value of taxable payroll over the period.

The actuarial balance for a valuation period is equal to the difference between the summarized income rate and the

summarized cost rate for the period. An actuarial balance of zero for any period indicates that cost for the period could be met for the period as a whole (but not necessarily at all points within the period), with a remaining trust fund reserve at the end of the period equal to 100 percent of the following year’s cost. A negative actuarial balance for a period indicates that the present value of income to the program plus the existing trust fund is less than the present value of the cost of the program plus the cost of reaching a target trust fund reserve of 1 year’s cost by the end of the period. Generally, a trust fund is deemed to be adequately financed for a period if the actuarial balance is zero or positive, meaning that the reserves at the end of the period are at least equal to annual cost. Solvency is still possible with a small negative actuarial balance where reserves are still positive.

Table IV.B4 contains summarized rates for the intermediate, low-cost, and high-cost assumptions. The low-cost and high-cost assumptions define a wide range of possibilities. Financial outcomes as good as the low-cost scenario or as bad as the high-cost scenario are unlikely to occur.

For the entire 75-year valuation period, the combined OASDI program has actuarial balances between 0.000 and 0.005 percent of taxable payroll under the low-cost assumptions, ‑2.88 percent under the intermediate assumptions, and ‑6.56 percent under the high-cost assumptions. These balances indicate that the combined OASDI program is adequately financed for the 75-year valuation period under only the low-cost assumptions.

However, eliminating the actuarial deficit for the next 75-year valuation period requires raising payroll taxes or lowering benefits by more than is required just to achieve solvency, because the actuarial deficit includes the cost of attaining a target trust fund ratio equal to 100 percent of annual program cost by the end of the period. The actuarial deficit could be eliminated for the 75-year period by increasing revenues in a manner equivalent to an immediate and permanent increase in the combined payroll tax from 12.40 percent to 15.39 percent (a relative increase of 24.1 percent),

4 reducing cost in a manner equivalent to an immediate reduction in scheduled benefits of 18.2 percent, or some combination of approaches could be used.

Under the intermediate assumptions, the OASDI program has large annual deficits toward the end of the long-range period that are increasing and reach 4.90 percent of payroll for 2088 (see table IV.B1). These large deficits indicate that annual cost continues to exceed non-interest income after 2088, so continued adequate financing would require larger changes than those needed to maintain solvency for the 75-year period. Over the period extending through the infinite horizon, the actuarial deficit is 4.1 percent of payroll under the intermediate assumptions.

Table IV.B5 presents the components and the calculation of the long-range (75-year) actuarial balance under the intermediate assumptions. The present value of future cost less future non-interest income over the long-range period, minus the amount of trust fund asset reserves at the beginning of the projection period, amounts to $10.6 trillion for the OASDI program. This amount is the 75-year “open group unfunded obligation” (see row

H). The actuarial deficit (which is the negative of the actuarial balance) combines this unfunded obligation with the present value of the ending target trust fund and expresses the total as a percentage of the present value of the taxable payroll for the period. The present value of future non-interest income minus cost, plus starting trust fund reserves, minus the present value of the ending target trust fund, is ‑$11.1 trillion for the OASDI program. The actuarial balance , expressed as a percentage of taxable payroll for the period, is ‑2.88 percent.

Another measure of trust fund finances, discussed in Appendix F, is the infinite horizon unfunded obligation, which takes account of all annual balances, even those after 75 years. The extension of the time period past 75 years assumes that the current-law OASDI program and the demographic and economic trends used for the 75‑year projection continue indefinitely. This infinite horizon unfunded obligation is estimated to be 4.1 percent of taxable payroll or 1.4 percent of GDP. Of course, the degree of uncertainty associated with estimates increases substantially for years further in the future.

Table IV.B6 shows the effects of changes on the long-range actuarial balance, by category, between last year’s report and this report.

Since the last report, no laws have been enacted that are expected to have significant effects on the long-range cost of the OASDI program. However, the Supreme Court’s decision in the United States v. Windsor case, in June 2013, is projected to have a small but significant effect on the long-range cost of the OASDI program. This decision repealed parts of the Defense of Marriage Act, which affects the payment of federal benefits based on same-sex marriages. The extent to which OASDI benefits based on marriage will be available to same-sex couples is still not completely clear. SSA has issued guidelines, approved by the Department of Justice, for certain benefits for same-sex couples who were legally married when the insured account holder resided in a State or jurisdiction that recognized same-sex marriages at the time of application or death. Expansion of this authority to other same-sex couples and to other benefits is under review at the Department of Justice. For the estimates in this report, the Trustees have assumed that Social Security will expand its guidelines to recognize all auxiliary beneficiaries for such marriages and that same-sex marriages will eventually be recognized in all States. This projected expansion of benefits decreases the long-range OASDI actuarial balance by 0.01 percent of taxable payroll.

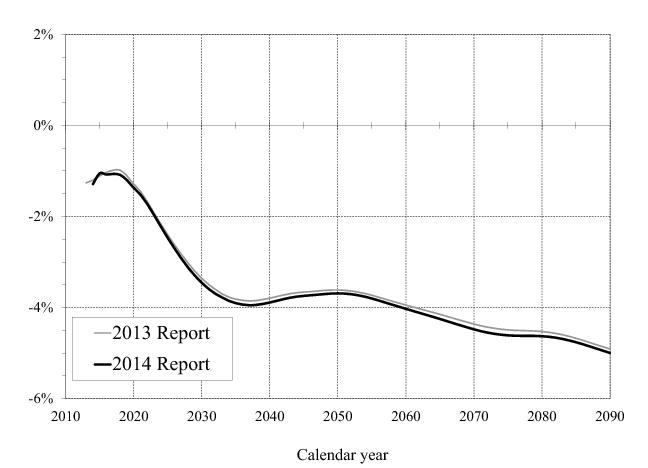

Figure IV.B4 compares the annual cash-flow balances for this report and the prior year’s report for the combined OASDI program over the long-range (75-year) projection period. The figure illustrates the annual effects of the changes described earlier in this section.