|

|

|

|

|

|

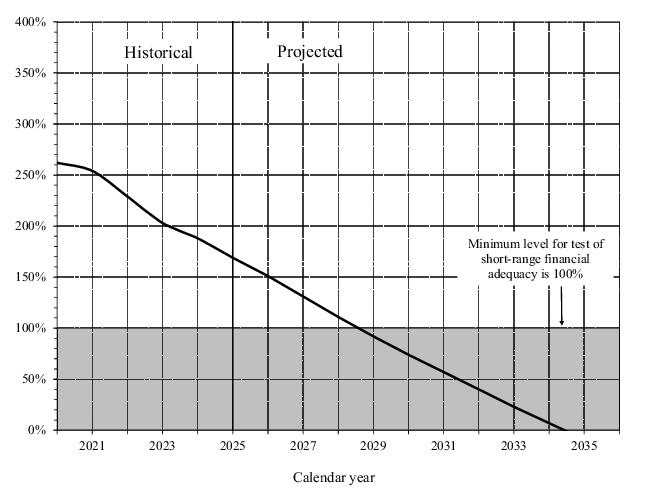

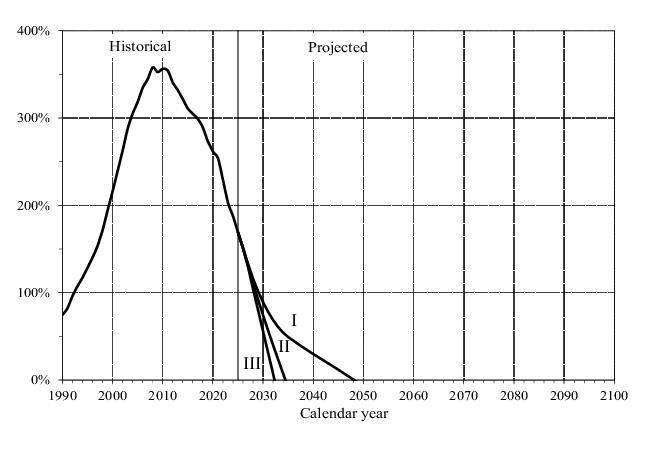

Short-Range Actuarial EstimatesOn a combined basis, OASDI fails the test of short-range financial adequacy because the OASDI trust fund ratio declines to 92 percent by the beginning of 2029 and continues to decline until reserves become depleted in the third quarter of 2034. Figure II.D1 shows that the OASDI trust fund ratio is expected to decline throughout the short-range period, as it has since 2010.

and Trust Fund Reserve Depletion Dates

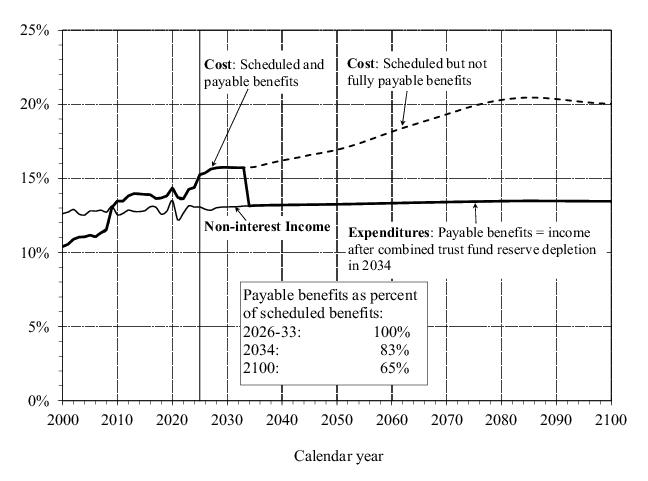

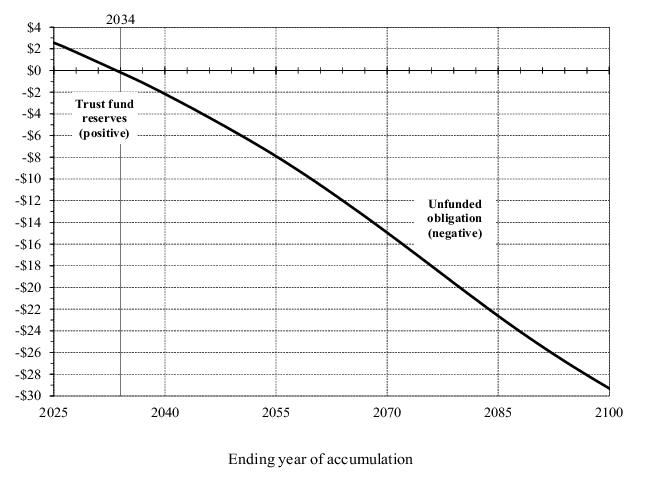

Another way to illustrate the OASDI program’s projected financial shortfall is to examine the cumulative present value of scheduled income less cost. Figure II.D5 shows the present value of cumulative OASDI income less cost from the program’s inception through each of the years from 2025 to 2100. A positive value represents the present value of trust fund reserves at the end of the selected year. A negative value is the unfunded obligation through the selected year.Figures II.D2, II.D4, and II.D5 show that the program’s actuarial status will deteriorate throughout the projection period if current law is not altered. Negative annual balances and increasing cumulative shortfalls toward the end of the 75-year period indicate the additional change that will be needed by then in order to maintain solvency beyond 75 years.

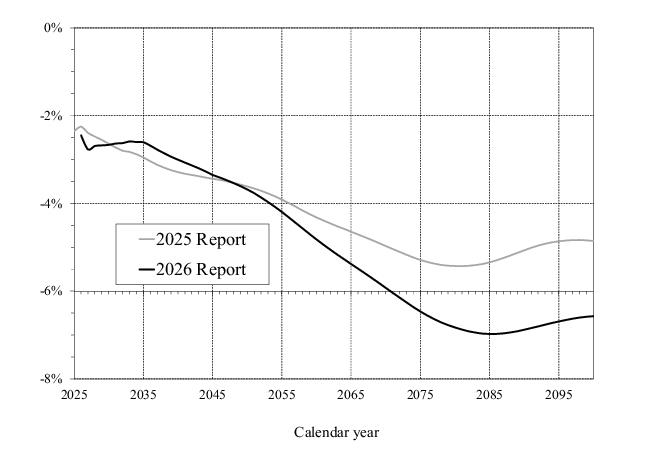

Figure II.D9 compares this year’s projections of annual balances (non-interest income minus cost) to those in last year’s report. The annual balances in this year’s report are lower (more negative) in years 2026 through 2030, higher (less negative) in 2031 through 2047, and lower in 2048 through 2100, with a widening difference between the two lines from 2048 to about 2085. For the 75-year projection period 2026 through 2100, the annual balances average 0.72 percentage points lower in this year’s report.

Appendix F also presents summary measures over the infinite horizon. The infinite horizon values provide an additional indication of Social Security’s very-long-run financial condition.

|

|

|

|

|

|

|

| SSA Home | Privacy Policy | Website Policies & Other Important Information | Site Map | Actuarial Publications | June 9, 2026 | |