Testimony by Jim Borland,

Acting Deputy Commissioner for Communications, Social Security Administration

Special Committee on Aging

January 24, 2018

Chairman Collins, Ranking Member Casey, and Members of the Special Committee:

I am Jim Borland, Acting Deputy Commissioner for Communications at the Social Security Administration (SSA). Thank you for inviting me to discuss how SSA provides information to help workers and their family members decide when to claim Social Security retirement benefits, and when to enroll in Medicare. These decisions are important, and we are mindful of our responsibility to provide information to help our claimants make informed decisions that best fit their individual circumstances.

Overview

We administer the Old-Age, Survivors, and Disability Insurance (OASDI) program, commonly referred to as “Social Security.” Individuals earn coverage for Social Security retirement, survivors, and disability benefits by working and paying Social Security taxes on their earnings. Payroll tax revenues fund the Social Security program. We also administer the Supplemental Security Income (SSI) program, which provides monthly payments to people with limited income and resources who are aged, blind, or disabled. Adults and children under age 18 can receive payments based on disability or blindness. General tax revenues fund the SSI program.

Few government agencies touch the lives of as many people as we do. Social Security pays monthly OASDI benefits to approximately 62 million individuals. During fiscal year (FY) 2017, we paid about $934 billion to Social Security beneficiaries. This included about:

- $793 billion to an average of about 51 million retired workers, the spouses and children of retired workers, and the survivors of deceased workers a month; and

- $141 billion to an average of more than 10 million disabled beneficiaries and their spouses and children a month.1

Medicare is a national health insurance program administered by the Centers for Medicare and Medicaid Services (CMS). It provides health insurance for people age 65 and older, younger disabled workers, and individuals with end stage renal disease. SSA is responsible for enrolling people in Medicare. In FY 2017, we enrolled over five million people in Medicare.

Helping Individuals Understand Social Security Retirement and Medicare

Before individuals apply for and receive Social Security benefits, SSA has an important role to provide objective and clear information that individuals may use to plan for retirement and make informed decisions appropriate for their circumstances. We have a variety of ways to inform individuals about their claiming options before they decide to file for Social Security benefits or enroll in Medicare. These resources are critical because they allow individuals to consider the best age for them to start benefits based on their health, finances, and other personal circumstances. We provide this information using a variety of methods, including the Social Security Statement, our website and publications, outreach, and more.

Social Security Statement

The Social Security Statement (Statement) provides information on lifetime earnings as well as estimates of future benefits workers and their families may receive based on those earnings. Individuals may access their Statement at any time through a personal online my Social Security account. They also receive an annual reminder to check the most recent version of their Statements. Additionally, we currently mail Statements to individuals aged 60 and older who are not receiving Social Security benefits and do not have a my Social Security account.2 In FY 2017, 15.6 million my Social Security users accessed their Statements nearly 46 million times, and we mailed around 13.5 million Statements.

The Statement provides personalized information about an individual’s potential retirement benefits, as well as a detailed record of the individual’s earnings history. Individuals may use the Statement to verify their earnings history and to inform us if their earnings need to be corrected. For retirement benefits, the Statement lists the benefit amounts that an individual is estimated to receive at age 62, at full retirement age (FRA), and at age 70. The Statement describes additional factors an individual should consider before deciding when to apply for benefits. It includes information on how work affects benefits; how a worker’s claiming decision affects survivors benefits; how to avoid a Medicare late-enrollment penalty; and information on average life expectancy. Since we launched my Social Security accounts in 2012, more than 34 million users have registered and more workers are signing up every day. In addition, my Social Security accounts consistently rank among the top 10 in customer satisfaction for all Federal government websites.

Over the next few years, we plan to enhance the online Statement to attract more workers to sign-up, review their personal information, and conduct business with us online.

Publications and Online Tools

We offer a wealth of other information to the public through our publications, website, and other online tools. More than 99 million people visited our website a total of more than 232 million times in calendar year 2017. Numerous publications, webpages, and Frequently Asked Questions explain the effect that earnings, the age at which benefits are claimed, and the receipt of a non-covered pension may have on Social Security benefits.3 Our resources range from providing basic information about benefits, to delving into the details of benefit calculations, factors to consider when filing for benefits, and more.

We offer a variety of online calculators. One of these, the Retirement Estimator, allows an individual to input a few pieces of personal information and receive an estimate of benefits that would be payable if he or she were to claim benefits at age 62, at FRA, at age 70, or at any age in between based upon his or her actual earnings information.4 Based on surveys conducted by Foresee, the Retirement Estimator is one of the highest rated government sites in customer satisfaction. The Retirement Estimator lets individuals enter different future earnings information and expected stop work dates, to help decide the best time to retire. We also offer a Life Expectancy Calculator to aid people with their retirement planning. This calculator allows an individual to see average life expectancy based on individuals with his or her gender and date of birth.5

We also offer substantial information when an individual completes the online application for retirement benefits. Throughout the online retirement application, we provide links that explain why we ask for particular information, and the importance of that information based on an individual’s circumstances. For example, within the online application, when an individual indicates the date they want to start receiving benefits, we inform them that if benefits begin before FRA, their monthly benefits will be permanently reduced. We also provide links to detailed information explaining the effects of receiving benefits before and after FRA. Additionally, we provide a link to the Retirement Estimator, mentioned earlier, that allows claimants to see what their benefit amount would be at various ages. This level of information is important because the majority of retirement claims are filed online (in 2017, about 53 percent of retirement applications were filed online).

Medicare Information

CMS administers the Medicare program, but individuals enroll in Medicare by contacting SSA. Thus, SSA and CMS work in partnership and both agencies maintain and communicate information about how to enroll, what the enrollment options are, and who to contact for more information about enrollment. For example, our publication How to Apply Online for Medicare Only explains how an individual who is not ready to apply for Social Security benefits but does want to enroll in Medicare can do so quickly and efficiently.6

Our publication entitled Retirement Information for Medicare Beneficiaries provides information that can help an individual who has already enrolled in Medicare decide when to apply for Social Security retirement benefits.7

Our website includes helpful information about Medicare, including information about enrolling in Medicare at 65 and delaying retirement benefits until after FRA. Our website also links to the CMS flagship publication, Medicare and You, giving the public instant access to a wealth of information.8

Direct Service to Customers

Our employees are dedicated to providing customers with the information they need to make a well-informed decision about claiming Social Security benefits and enrolling in Medicare. They assist the public in a variety of ways, such as through face-to-face interaction in a field office, by telephone (including our national toll-free number, 1-800- 772-1213), in response to online applications, and by mail.

Employees inform individuals of the benefits for which they and their family members may be eligible; provide monthly benefits amounts at early, full, and delayed retirement ages; and discuss other information the claimant may need to know about Social Security rules, requirements, and benefits. Employees also inform individuals about the Medicare program including information about premiums, deductibles, enrollment periods, the month coverage begins, penalties for declining Medicare Part B when first eligible, as well as the prescription drug plan (Medicare Part D), and where to find help with covering prescription drug costs.

SSA employees provide detailed information about the Social Security and Medicare programs, and how the rules apply to each individual’s situation. However, they do not attempt to persuade individuals regarding whether or when to file for benefits. This is because our employees are not in a position to know about or discuss the personal circumstances––such as financial resources, tax situation, health, and family longevity–– that may be important in deciding which age is best for that person to claim benefits.

Outreach

Public outreach is an essential part of our strategy to educate more Americans on the retirement benefit options. We provide the public with critical information about our programs, benefits, and services. To this end, our field and regional offices are committed to connecting with the public at the local, grass-roots level.

During fiscal year 2017, Social Security employees participated in more than 6,000 events to help the American people better understand Social Security and Medicare benefits. With an estimated audience of more than 3.7 million people, these events ranged from small rural get-togethers in public libraries, senior centers, churches, and veterans’ organizations to large gatherings like county and state fairs, senior expos, and employer group meetings. Whether the attendance is in the tens or the thousands, SSA employees are there to help Americans better understand their benefits.

Among those events, pre-retirement seminars are particularly effective forums to discuss options for claiming Social Security and Medicare. Since 2004, we have helped the National Rural Electric Cooperative Association identify speakers for more than 400 such seminars throughout America’s heartland.

Examples from our regions further illustrate our efforts to ensure rural and remote populations have equal access to Social Security and Medicare information:

Our Seattle Region is experimenting with existing technologies to conduct seminars in the remote and underserved communities in the State of Alaska. In our Philadelphia Region, we have worked closely with the Pennsylvania Department of Labor and Industry to ensure that remote counties like Erie, Crawford, and Franklin are served. Our preretirement seminars in these counties help residents understand their many Social Security options. Our Boston Region has worked with Maine’s Area Agencies on Aging as well as the five federally recognized American Indian Tribes located in extremely remote areas of the state.

In addition to our work in the regions, we also work closely with national organizations, advocacy groups, and other Federal agencies to maximize the reach of our public education and communication efforts.

We continue to strengthen our partnership with CMS to improve our outreach for Americans nearing the Medicare eligibility age. Recently, we have:

- Updated the Statement insert for older individuals to strengthen the message about when to apply for Medicare and to make the information more prominent;

- Included additional language or made existing language about the late enrollment penalty and Medicare clearer in several publications;

- Added additional frequently asked questions to address late enrollment fees, and signing up for Medicare when health insurance through current employment or when VA benefits are involved; and

- Coordinated communications with Medicare beneficiaries about the issuance of new Medicare cards in 2018, including an alert to beware of scams targeting the elderly and disabled.

Choosing When to Claim Retirement Benefits

Choosing when to start receiving Social Security retirement benefits is an important decision that affects the amount that individuals receive for the rest of their lives. Workers can claim full (unreduced) retirement benefits at FRA – currently age 66 and 4 months for people who turn 62 in 2018.9 Social Security also allows individuals to claim benefits as early as age 62 or to allow their benefit amount to grow up to age 70.10

Receiving Social Security benefits before FRA permanently reduces an individual’s monthly retirement benefit – and the earlier benefits begin, the greater the reduction.11 In 2018, retirement benefits claimed at age 62 result in a reduction of up to 26.7 percent, compared to the benefit payable at FRA(66 and 4 months).12

On the other hand, individuals who delay claiming beyond FRA earn “delayed retirement credits” (DRCs) for every month they do not receive benefits after attaining FRA and prior to attaining age 70. For those born in 1943 and later, each month of delay increases the retirement benefit by two-thirds of one percent, or eight percent per year. For a person whose FRA is 66, delaying until 70 would result in a monthly benefit 32 percent higher than the amount that would be payable if claimed at FRA.

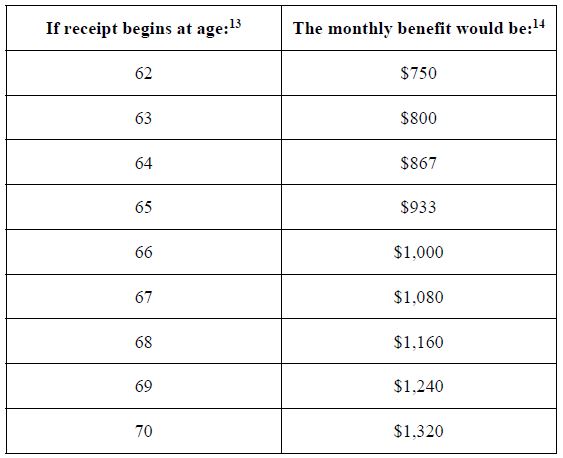

For example, consider an individual eligible for a $1,000 monthly benefit who was born between 1943 and 1954. He or she would have an FRA of 66. As shown in the following chart, if he or she took benefits at age 62, the monthly amount would be permanently reduced by 25 percent to $750. On the other hand, if he or she delayed benefits until age 70, the monthly amount would be permanently increased by 32 percent (eight percent per year from age 66 to 70) to $1,320. Overall, delaying the start of benefits from age 62 to 70 would increase the monthly benefit by 76 percent (from $750 to $1,320), or almost $7,000 a year.

Retirement claiming decisions can also affect the amount of the benefit that the worker’s spouse will receive if he or she outlives the worker. In effect, the same adjustment that applies to the worker’s retirement benefit will apply to survivor benefits paid to the worker’s widow or widower for the rest of his or her life.

Deciding when to claim retirement benefits can be complex, and a person should consider many factors when making his or her decision. In addition to the monthly benefit amount, individuals should consider their personal and family circumstances, including current and future financial resources and obligations, and anticipated health and longevity.

Married couples have two lives to plan for throughout retirement. Married retirees must consider important information about Social Security protection for widowed spouses. A higher-earning partner who delays benefits will receive higher monthly benefits for his or her life. This delay may also result in higher survivor’s benefits for a spouse if the spouse lives longer.

Enrolling in Medicare

We strive to make it as easy as possible for people to get information about how to enroll in Medicare and to complete the enrollment process. It is important that people know their enrollment options in order to avoid delays in the effective date of coverage or increases in their premiums. One of our goals is to help people who are approaching age 65 know that, even though full retirement age is increasing, Medicare eligibility still begins (in most cases) at age 65. Accordingly, for people who are age 55 or older, we include with the Statement a document titled “Thinking of retiring?”, which features a prominent message advising the person to sign up for Medicare at age 65 even if he or she does not plan to receive monthly Social Security benefits at that time.

Current Social Security retirement beneficiaries receive an enrollment package from CMS about 3 months before they turn 65. It tells them that they will be enrolled in Part A. It also tells them they will be automatically enrolled in Part B unless they inform us they do not want the coverage (except in Puerto Rico where, by law, residents must optin if they want Part B coverage). Disability beneficiaries who have been receiving benefits for 24 months are also automatically enrolled in Medicare and receive the same enrollment package.

Individuals who are not receiving Social Security benefits must take action to enroll in Medicare. They can do so in person, by phone, or online during one of the following enrollment periods:

- Initial Enrollment Period - the month the individual turns 65, the three months before, and the three months after;

- General Enrollment Period - January 1 to March 31 of every year; or

- Special Enrollment Period - Individuals who continue to work past age 65 or who have a spouse that works and who have employment-based health insurance may have a special enrollment period (SEP). The SEP allows the individual to file during the eight-month period that begins after the employment-based health insurance ends, without having to pay a penalty in the form of increased premiums.

Many individuals can enroll in Medicare online, even if they do not want to claim their

Social Security benefits. Individuals can use our online Medicare application if they:

- are at least 64 years and 9 months old;

- want to sign up for Medicare but do not currently have any Medicare coverage;

- do not want to start receiving Social Security benefits; and

- are not currently receiving Social Security retirement, disability or survivors benefits.

Conclusion

When Congress passed the Social Security Act in 1935, it did so to provide seniors with benefits based on their earnings to sustain them throughout their retirement. This continues to be one of the program’s core purposes. Currently, program rules allow individuals to claim their retirement benefits and receive different monthly benefit amounts at any time between the ages of 62 and 70, offering individuals flexibility to make decisions based on their individual circumstances. Accordingly, we understand the importance of providing useful information to the public about their choices for retirement. Through interaction with agency employees, the Statement, my Social Security accounts, other online tools, our publications, and our outreach efforts, we provide valuable ways for individuals to learn about how claiming decisions may affect their benefits.

Similarly, when Congress passed Medicare in 1965, it charged the Social Security Administration with the responsibility to enroll people in the program. We take that responsibility very seriously, and we strive to ensure that we, in partnership with the Centers for Medicare and Medicaid Services, provide accurate, useful information that helps ensure people know when and how to contact us to enroll in Medicare, especially when they are not yet receiving Social Security benefits.

Thank you again for inviting me here today. I would be glad to answer any questions.

______________________________________________

1 There were also on average more than 8 million SSI recipients per month in Fiscal Year 2017.

2 Individuals also may request a copy of their Statement at any time.

3 http://faq.ssa.gov/

4 https://www.ssa.gov/retire/estimator.html

5 https://www.ssa.gov/OACT/population/longevity.html

6 https://www.ssa.gov/pubs/EN-05-10531.pdf

7 https://www.ssa.gov/pubs/EN-05-10529.pdf

8 https://www.medicare.gov/medicare-and-you/different-formats/m-and-y-different-formats.html

9 For persons born in years 1943 through 1954, full retirement age is 66. For people who turn 62 in 2018 (born in 1956), full retirement age is 66 and 4 months, 2 months more than it was for those who turned 62 last year. The retirement age will continue to increase by 2 months every year until it reaches age 67 for those who were born in 1960 or later.

10 Workers who are no longer covered under employer-sponsored health insurance and individuals with employers that have fewer than 20 employees must sign up for Medicare when eligible if they wish to avoid a penalty in the form of an increased premium for Medicare Part B coverage. Individuals who are still working or are covered by their or their spouse’s employer’s group health insurance plan, can postpone signing up for Medicare Part B without penalty until they are no longer covered by the group health insurance plan based on current employment, at which time they will have an eight-month Special Enrollment Period in which to sign up. In addition, there is a late enrollment penalty for not signing up for Medicare Part D during the Initial Enrollment Period. However, the penalty may be waived if an individual shows proof of creditable drug coverage.

11 The monthly benefit is reduced by 5/9 of one percent for each month up to 36 months before FRA and then 5/12 of 1 percent for each additional month before FRA.

12 For people born in 1960 or later, choosing

13 See SSA Pub. No. 05-10147, “When to Start Receiving Retirement Benefits” (January 2017), available at https://www.ssa.gov/pubs/EN-05-10147.pdf.

14 These monthly benefit amounts do not account for any benefit increase that may be due to earnings after age 61, nor do they include cost-of-living adjustment (COLA) increases.