Working and Claiming Behavior at Social Security's Early Eligibility Age Among Men by Lifetime Earnings Decile

ORES Working Paper No. 115 (released September 2020)

Using a merged internal research file of administrative data from the Social Security Administration, I examine men's working and retired-worker benefit claiming behavior at and around Social Security's early eligibility age of 62, and disaggregate the results by lifetime earnings decile. I also examine how mortality risk varies among men exhibiting different working and claiming behaviors, before and after controlling for the lifetime earnings decile to which they belong. This paper follows up ORES Working Paper No. 114, which details the study methodology and presents summary findings on men's and women's working and claiming behavior. Both papers find substantial heterogeneity in working and claiming behavior at age 62; in this paper, while differences in men's working and claiming behavior were sometimes observed between lifetime earnings deciles, that heterogeneity in behavior was also observed within each lifetime earnings decile.

When this paper was written, the author was with the Office of Research, Office of Research, Evaluation, and Statistics, Office of Retirement and Disability Policy, Social Security Administration.

Acknowledgments: The author would like to thank Chris Chaplain, John Jankowski, Anya Olsen, David Olson, David Pattison, Katie Sutton, and Elisa Walker for their helpful comments and suggestions.

Working papers are unedited papers prepared by staff in the Office of Research, Evaluation, and Statistics and published on our website as a resource for future research initiatives and to encourage discussion among the wider research community. The findings and conclusions presented in this paper are those of the author and do not necessarily represent the views of the Social Security Administration.

| AIME | average indexed monthly earnings |

| EEA | early eligibility age |

| FRA | full retirement age |

| GAO | Government Accountability Office |

| OASDI | Old-Age, Survivors, and Disability Insurance |

| SSA | Social Security Administration |

Introduction

This working paper, in conjunction with Waldron (2020), provides statistics on working and claiming behavior around Social Security's early eligibility age (EEA) as a supplement and follow up to discussions in Waldron (2013, 2015). Where Waldron (2020) provided a picture of working and claiming behavior disaggregated by sex, this paper explores whether those behaviors differ between and/or within lifetime earnings deciles among men.

This paper also measures the relative mortality risk of workers in those disaggregated working and claiming categories. The mortality risk analysis is intended to provide readers with information on whether the categories into which fully insured men have self-sorted follow correlations between labor force participation and health, and between benefit claiming and mortality risk, that have been observed in the literature (see Waldron 2015 for a review). If the correlations follow that literature, results could be interpreted as strengthening the conclusion reached in Waldron (2020). That paper finds that the lack of homogeneity observed in working and claiming behavior at the EEA means that one cannot rule out the possibility that workers self-select or self-sort into working and claiming categories based on their life circumstances. If the expected correlations with mortality risk do not hold, then that conclusion could be weakened.

As noted in Waldron (2012, 16), differences in hours worked between men and women imply that a woman's own earnings may be less likely to place her into an earnings decile that proxies for her socioeconomic status, relative to her male counterpart. For example, Monk, Turner, and Zhivan (2010) found that among individuals observed in the 1992–2006 Health and Retirement Study, the highest average indexed monthly earnings (AIME) amount (a top 35-year lifetime earnings measure) in the household was a worker's own AIME for 97 percent of married men and only 15 percent of married women. Supporting that result, Waldron (2012) found that while approximately 46 percent of male fully insured workers born in 1945 had an AIME amount greater than the top bend point of the retired-worker benefit formula, only 10 percent of women did.1 That result was driven by differences in the number of market hours worked per week and in differences in years of Social Security–covered earnings between men and women. In addition, even for members of birth cohorts who have not yet reached age 61, hours of work are not equal between men and women because women are more likely to be engaged in non-market work (for example, child care) in the empirical data (Waldron 2012). Because earnings are only reported to the Social Security Administration (SSA) on an individual basis, female workers cannot be placed into categories that one would expect to be analytically equivalent to those of their male counterparts.2 Accordingly, this paper disaggregates working and claiming behavior by earnings decile for men, postponing analysis of female workers for future study.

Following a section that describes the methodology behind this paper's earnings decile analysis, estimates of working and claiming by lifetime earnings decile and estimates of mortality risk by various categories of working and claiming are presented and then discussed in the context of related previous literature. The paper concludes by highlighting the study's main findings and putting those findings in a historical context.

Methodology

For this paper, unless otherwise noted, tabulations are structured to parallel the tabulations reported in Waldron (2020). That paper documents the Social Security administrative data and the methodology used to classify workers into various combinations of working at ages 61 and 63 and claiming or not claiming at age 62. In that paper, which did not disaggregate workers by earnings decile, the denominator for all calculations was the number of men (or women)3 fully insured at age 61 who lived to age 64 and were not disabled-worker beneficiaries. The denominator for each lifetime earnings decile depicted here is the number of fully insured men in each earnings decile who meet those sample restrictions. As such, the proportion of workers in each working and claiming category in aggregate can be directly compared with the proportion in each category by decile. In other words, when the percentages calculated for each earnings decile by working and claiming subgroup are summed, they will equal 100 percent of workers in a given earnings decile.4

The Definition of Lifetime Earnings

This paper defines lifetime earnings as did Waldron (2013), following a measure of socioeconomic status first developed in Waldron (2007). Earnings at ages 45–55 are used to proxy for lifetime earnings. To construct the measure, earnings are observed at ages 45–55 for each birth cohort included in the sample. Those earnings are measured relative to the national average wage index in the observation years (1982–1999 for workers born 1937–1944 at ages 45–55). These relative earnings are then averaged over ages 45–55. To avoid unintended interactions between year of birth and earnings level, the percentile of the earnings distribution in which an individual falls is based on the distribution of average earnings for members of that individual's birth cohort.

Earnings reports for non–Social Security covered workers and earnings over Social Security's Old-Age, Survivors, and Disability Insurance (OASDI) taxable maximum are available beginning in roughly 1982 in SSA's Master Earnings File.5 Because those data are only observable beginning in 1982, a top 35-year measure more comparable to Social Security's AIME amount but including earnings above the taxable maximum cannot be calculated using Social Security administrative data for birth cohorts fully insured for retired-worker benefits at age 61 without substantial imputation of earnings capped at the taxable maximum. Imputation techniques, by their nature, add more uncertainty to the data and are unlikely to achieve the precision needed to divide the earnings distribution into deciles, particularly at the upper end of the distribution and in years when the OASDI taxable maximum was low relative to the average wage. Results could also be sensitive to the choice of imputation technique.

Ages 45–55 were chosen as a proxy for lifetime earnings because on average those ages occur at the peak of the earnings distribution.6 Peak earnings are a strong proxy for lifetime earnings because earnings at the peak will generally capture fulfilled earnings potential. Because the 1937 birth cohort is the oldest one observed, one can calculate a measure that includes non–Social Security covered earnings and Social Security covered earnings over Social Security's taxable maximum, beginning in 1982. This allows one to construct earnings deciles without having to impute earnings amounts over Social Security's taxable maximum. Because this measure includes earnings in non–Social Security employment beginning in 1982, years of zero earnings are included.7 This definition of lifetime earnings is expected to be highly correlated (for men) with the measure of lifetime earnings that SSA uses to calculate retired-worker benefits, which is referred to as Social Security's AIME amount. However, unlike AIME, this measure will assign workers with high peak non–Social Security earnings, and lower Social Security covered earnings earlier in their career, to the more analytically appropriate socioeconomic status category.

Statistical Approaches Used to Illustrate the Data

In aggregate, the shares of men in most earnings and claiming categories were not constant over time, but exhibited either upward or downward statistically significant trends over the observation period. On a disaggregated basis, or by decile, there could be differences in the proportion of men in a particular earnings and claiming category at any particular point in time as well as differing changes in that proportion over time. In addition, because drilling down to the level of working and claiming behavior by decile can create some fairly small subsamples, a particular point-in-time estimate may partially reflect statistical noise.

Accordingly, I took a variety of methodological approaches to ensure that the decile estimates are statistically robust. First, the statistical significance and direction of trends in the percentage of fully insured men in each claiming and earnings category by decile over time were tested. To conduct these tests I ran a regression for each subcategory and decile to see if a trend by year of birth is significant over time.8 Table 1 shows the results. The tests parallel the tests of trends by year of birth in Waldron (2020, Tables 1 and 2).

| Work status | Lifetime earnings decile | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 1 (lowest) | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 (highest) | |

| Claiming at age 62 and 0–2 months | ||||||||||

| Not working at age 61, not working at age 63 | No trend | Downward* | No trend | No trend | No trend | No trend | No trend | Downward** | Downward* | Downward* |

| Working at age 61, not working at age 63 | Downward* | Downward* | Downward* | Downward* | Downward* | Downward* | Downward* | Downward** | Downward* | Downward* |

| Working at age 63 | Downward* | No trend | Downward* | Downward* | Downward* | Downward* | Downward* | Downward* | No trend | Downward* |

| Claiming at age 62 and 3–11 months | ||||||||||

| Not working at age 61, not working at age 63 | No trend | No trend | No trend | No trend | No trend | No trend | No trend | No trend | No trend | No trend |

| Working at age 61, not working at age 63 | Downward* | No trend | No trend | Downward** | No trend | No trend | No trend | Downward** | Downward* | No trend |

| Working at age 63 | Downward* | No trend | No trend | Downward* | Downward** | No trend | Downward* | No trend | No trend | Downward* |

| Not claiming at age 62 | ||||||||||

| Working at age 63 | Downward* | Upward* | Upward* | Upward* | Upward* | Upward* | Upward* | Upward* | Upward* | Upward* |

| Not working at age 63 | Upward* | Upward* | Upward* | Upward* | Upward* | No trend | Upward* | Upward* | Upward* | Upward* |

| SOURCE: Author's calculations using Social Security administrative data (see Waldron 2020). | ||||||||||

| NOTES: Sample is restricted to fully insured workers who lived to age 64 and excludes disabled-worker beneficiaries.

* = statistically significant at the 10 percent level; ** = statistically significant at the 1 percent level; where working and claiming subgroup (y) = year of birth + the unemployment rate at age 62.

|

||||||||||

Next, I ran statistical tests to provide a smoothed snapshot of the differences in the proportion of workers within each working and claiming category by decile. To explore the data in this way, I conducted statistical tests of differences in the odds of men being in each earnings and claiming category by decile. Because of the movement over time observed for these categories in aggregate, performing a statistical test of this snapshot over the entire sample would require specifying a regression that includes interactions with year of birth. Because interactions increase multicollinearity and because the subsamples are fairly small, the regression was instead run on the sample's most recent birth cohorts, 1942–1944. This technique avoids the multicollinearity problem; however, the reader should keep in mind that relationships estimated for the older birth cohorts in the sample could differ.

To produce these estimates, I ran a logit regression for each working and claiming category. The regressions predict the odds that a fully insured man born during 1942–1944 will be in a particular working and claiming category. The explanatory variables include year of birth, the national unemployment rate at age 62, and dummy variables for lifetime earnings deciles 1–9. For example, if a man has earnings in decile 1, then the dummy variable for earnings decile 1 would equal 1, else it would equal zero. The reference variable in each equation for dummy earnings deciles 1–9 is decile 10 (the highest earnings level).

In this paper's next section, I present charts that illustrate the results. Charts 1–3 plot the odds that a man who had lifetime earnings in given decile resides in a particular working and claiming category, relative to a man in earnings decile 10. Error bars (vertical lines) extending from the odds-ratio data points for deciles 1–9 indicate the confidence intervals estimated around those points. If the confidence interval of one decile overlaps that of another, the odds that men in those two deciles are in a particular earnings and claiming category (relative to decile 10) are very close, and there is a statistical chance they are indistinguishable.

This statistical question can also be tested more formally. Accordingly, I repeated the regressions described above and tested to see if the odds that men within a given decile will belong to a particular earnings and claiming category differ with any statistical significance (results not shown). I used those regression results in creating Charts 4–6, which plot trends in each working and claiming category over time by decile, and which combine earnings deciles that were statistically indistinguishable from each other at the 10 percent level.9

Charts 4–6 supplement and magnify the aggregate results presented in Waldron (2020, Charts 2–3 and 5). In other words, one can observe whether the time trends observed for all deciles combined are also observed for each lifetime earnings decile, or whether disaggregation reveals noticeable differences by earnings decile. Charts 4–6 also include a dark blue line that represents the disaggregated trend line from the charts in Waldron (2020).

In Chart 7, the tabulations that underlie Charts 4–6 are rearranged to focus on differences in claiming and working behavior both between and within each lifetime earnings decile. It shows trends in the proportion of workers in each working and claiming category separately for each lifetime earnings decile. Chart 7 is thus designed to show potential deviations from subgroup averages that could be important to risk-averse workers who value the insurance aspects of the EEA option of claiming at age 62.

Finally, in Chart 8, mortality risk is estimated at ages 64–66 and 67–71 for fully insured male workers in various working and claiming categories relative to men who did not claim at age 62 and were still working at age 63. These estimates are shown both before and after controlling for lifetime earnings deciles. For technical details on the regression model, see Waldron (2013).

Differences in Working and Claiming Behavior by Lifetime Earnings Deciles

Waldron (2020) found that fully insured men were distributed among multiple combinations of working and claiming status, rather than being concentrated in one particular working and claiming category. In aggregate, or for all earnings deciles combined, the shares of fully insured workers who either claimed benefits and stopping working around the same time, claimed benefits and continued to work, or stopped work prior to claiming benefits all declined significantly over time. Conversely, the share of fully insured workers who did not claim benefits and continued to work, and the share who did not claim benefits and were not working, both increased significantly over time.

When working and claiming categories were further disaggregated by lifetime earnings decile, differences in working and claiming behavior were found both between and within deciles. Thus, heterogeneity in working behavior in aggregate was not found to be masking homogeneity in working and claiming behavior within particular earnings deciles. Overall, the least heterogeneous decile was decile 10 (the highest earnings level). By the end of the observation period, 70 percent of men in that decile were concentrated in the not claiming, still working category, and that decile also exhibited the greatest increase in the share of workers in that category over time.

This heterogeneity in working and claiming behavior can be seen in Charts 1–6 and is described in the category subsections that follow. Chart 7, described in a subsequent section, is intended to provide a high-level view of the subsections magnified below.

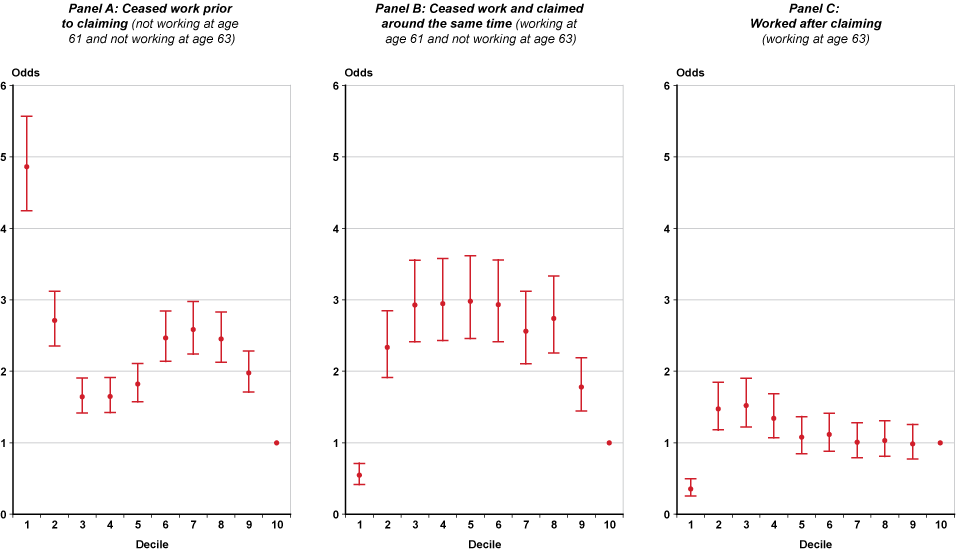

Odds of various work and claiming behaviors, by lifetime earnings decile: Men claiming at age 62 and 0–2 months

| Decile | Point estimate | Confidence interval | |

|---|---|---|---|

| Upper bound | Lower bound | ||

| Panel A: Ceased work prior to claiming (not working at age 61 and not working at age 63) | |||

| 1 | 4.861 | 5.567 | 4.245 |

| 2 | 2.710 | 3.120 | 2.354 |

| 3 | 1.643 | 1.907 | 1.416 |

| 4 | 1.647 | 1.912 | 1.420 |

| 5 | 1.821 | 2.109 | 1.572 |

| 6 | 2.465 | 2.841 | 2.139 |

| 7 | 2.583 | 2.975 | 2.242 |

| 8 | 2.451 | 2.826 | 2.127 |

| 9 | 1.975 | 2.284 | 1.708 |

| 10 | 1.000 | 1.000 | 1.000 |

| Panel B: Ceased work and claimed around the same time (working at age 61 and not working at age 63) | |||

| 1 | 0.544 | 0.713 | 0.414 |

| 2 | 2.332 | 2.846 | 1.910 |

| 3 | 2.929 | 3.555 | 2.412 |

| 4 | 2.946 | 3.577 | 2.427 |

| 5 | 2.980 | 3.616 | 2.455 |

| 6 | 2.930 | 3.557 | 2.413 |

| 7 | 2.561 | 3.119 | 2.103 |

| 8 | 2.740 | 3.332 | 2.254 |

| 9 | 1.778 | 2.187 | 1.446 |

| 10 | 1.000 | 1.000 | 1.000 |

| Panel C: Worked after claiming (working at age 63) | |||

| 1 | 0.354 | 0.492 | 0.255 |

| 2 | 1.475 | 1.845 | 1.179 |

| 3 | 1.522 | 1.901 | 1.219 |

| 4 | 1.341 | 1.683 | 1.068 |

| 5 | 1.076 | 1.366 | 0.848 |

| 6 | 1.115 | 1.412 | 0.880 |

| 7 | 1.007 | 1.282 | 0.791 |

| 8 | 1.030 | 1.310 | 0.810 |

| 9 | 0.984 | 1.255 | 0.772 |

| 10 | 1.000 | 1.000 | 1.000 |

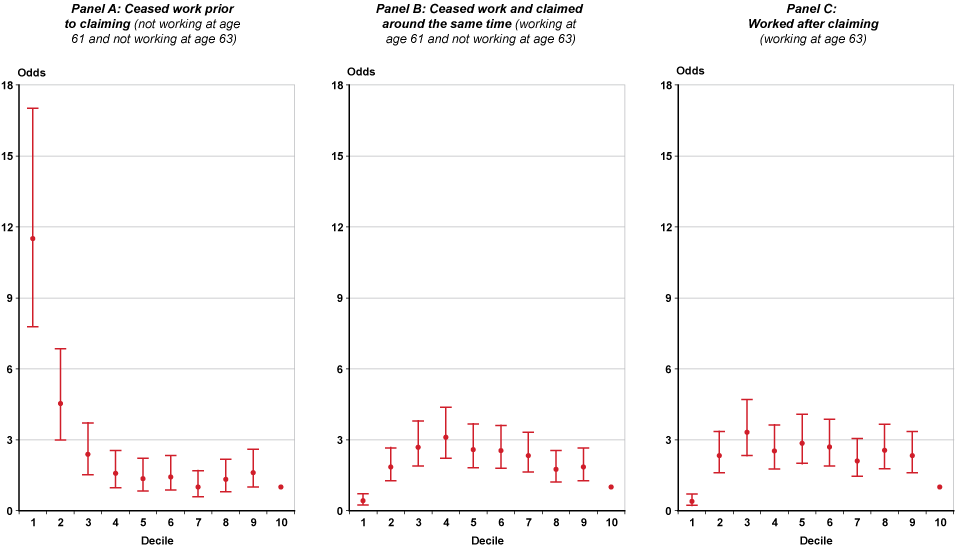

Odds of various work and claiming behaviors, by lifetime earnings decile: Men claiming at age 62 and 3–11 months

| Decile | Point estimate | Confidence interval | |

|---|---|---|---|

| Upper bound | Lower bound | ||

| Panel A: Ceased work prior to claiming (not working at age 61 and not working at age 63) | |||

| 1 | 11.508 | 17.010 | 7.786 |

| 2 | 4.526 | 6.843 | 2.994 |

| 3 | 2.383 | 3.717 | 1.527 |

| 4 | 1.578 | 2.540 | 0.980 |

| 5 | 1.360 | 2.221 | 0.833 |

| 6 | 1.433 | 2.328 | 0.882 |

| 7 | 0.999 | 1.690 | 0.590 |

| 8 | 1.324 | 2.168 | 0.808 |

| 9 | 1.614 | 2.593 | 1.004 |

| 10 | 1.000 | 1.000 | 1.000 |

| Panel B: Ceased work and claimed around the same time (working at age 61 and not working at age 63) | |||

| 1 | 0.419 | 0.717 | 0.244 |

| 2 | 1.844 | 2.661 | 1.277 |

| 3 | 2.684 | 3.797 | 1.897 |

| 4 | 3.113 | 4.376 | 2.214 |

| 5 | 2.590 | 3.671 | 1.828 |

| 6 | 2.543 | 3.607 | 1.793 |

| 7 | 2.331 | 3.320 | 1.636 |

| 8 | 1.751 | 2.536 | 1.209 |

| 9 | 1.843 | 2.660 | 1.277 |

| 10 | 1.000 | 1.000 | 1.000 |

| Panel C: Worked after claiming (working at age 63) | |||

| 1 | 0.402 | 0.707 | 0.228 |

| 2 | 2.325 | 3.353 | 1.613 |

| 3 | 3.311 | 4.698 | 2.334 |

| 4 | 2.526 | 3.627 | 1.759 |

| 5 | 2.854 | 4.074 | 1.999 |

| 6 | 2.702 | 3.867 | 1.888 |

| 7 | 2.100 | 3.046 | 1.449 |

| 8 | 2.551 | 3.661 | 1.777 |

| 9 | 2.325 | 3.352 | 1.612 |

| 10 | 1.000 | 1.000 | 1.000 |

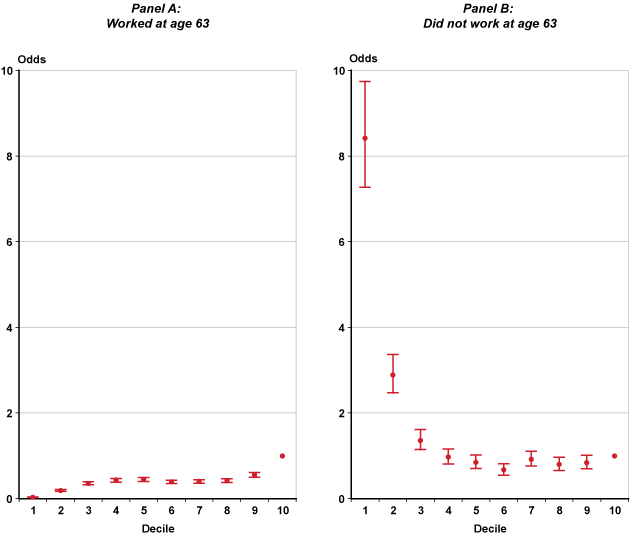

Odds of various work and claiming behaviors, by lifetime earnings decile: Men not claiming at age 62

| Decile | Point estimate | Confidence interval | |

|---|---|---|---|

| Upper bound | Lower bound | ||

| Panel A: Worked at age 63 | |||

| 1 | 0.033 | 0.039 | 0.028 |

| 2 | 0.191 | 0.213 | 0.172 |

| 3 | 0.356 | 0.395 | 0.321 |

| 4 | 0.428 | 0.474 | 0.386 |

| 5 | 0.444 | 0.492 | 0.401 |

| 6 | 0.391 | 0.433 | 0.352 |

| 7 | 0.400 | 0.443 | 0.361 |

| 8 | 0.416 | 0.461 | 0.375 |

| 9 | 0.554 | 0.615 | 0.500 |

| 10 | 1.000 | 1.000 | 1.000 |

| Panel B: Did not work at age 63 | |||

| 1 | 8.418 | 9.744 | 7.272 |

| 2 | 2.884 | 3.367 | 2.470 |

| 3 | 1.359 | 1.612 | 1.146 |

| 4 | 0.970 | 1.164 | 0.808 |

| 5 | 0.848 | 1.023 | 0.703 |

| 6 | 0.672 | 0.819 | 0.550 |

| 7 | 0.919 | 1.105 | 0.764 |

| 8 | 0.798 | 0.966 | 0.660 |

| 9 | 0.839 | 1.013 | 0.695 |

| 10 | 1.000 | 1.000 | 1.000 |

Prevalence of various work and claiming behaviors among fully insured men, by lifetime earnings decile: Men claiming at age 62 and 0–2 months

| Decile | 1937 | 1938 | 1939 | 1940 | 1941 | 1942 | 1943 | 1944 |

|---|---|---|---|---|---|---|---|---|

| Panel A: Ceased work prior to claiming (not working at age 61 and not working at age 63) | ||||||||

| All | 22.453 | 22.337 | 21.750 | 21.488 | 21.765 | 20.896 | 20.833 | 19.858 |

| 1 | 38.072 | 35.915 | 37.661 | 39.418 | 39.016 | 35.143 | 36.910 | 35.833 |

| 2 | 25.958 | 27.380 | 25.731 | 26.652 | 27.462 | 23.928 | 25.162 | 22.395 |

| 3–5 | 17.395 | 17.260 | 16.186 | 15.913 | 17.280 | 17.212 | 16.559 | 15.552 |

| 6–8 | 23.280 | 24.119 | 22.543 | 23.488 | 21.400 | 22.840 | 22.109 | 22.298 |

| 9 | 23.115 | 21.362 | 23.041 | 19.149 | 20.897 | 18.476 | 19.796 | 17.429 |

| 10 | 15.347 | 14.571 | 14.871 | 11.435 | 14.223 | 11.249 | 10.453 | 9.357 |

| Panel B: Ceased work and claimed around the same time (working at age 61 and not working at age 63) | ||||||||

| All | 14.775 | 14.328 | 13.923 | 13.130 | 11.375 | 10.796 | 10.176 | 9.369 |

| 1 | 3.832 | 5.516 | 3.977 | 4.143 | 2.295 | 3.333 | 2.128 | 2.532 |

| 2 | 15.204 | 14.101 | 13.801 | 10.414 | 11.597 | 12.011 | 10.638 | 8.763 |

| 3–6, 8 | 17.384 | 16.960 | 16.472 | 16.248 | 14.461 | 13.208 | 12.710 | 12.271 |

| 7 | 19.778 | 16.549 | 18.267 | 16.013 | 12.459 | 11.905 | 12.766 | 9.445 |

| 9 | 13.968 | 13.146 | 12.398 | 12.542 | 9.409 | 9.429 | 8.048 | 7.108 |

| 10 | 8.045 | 9.166 | 8.431 | 6.951 | 5.689 | 5.243 | 4.625 | 4.483 |

| Panel C: Worked after claiming (working at age 63) | ||||||||

| All | 7.258 | 6.483 | 5.370 | 5.333 | 5.633 | 5.307 | 4.746 | 4.022 |

| 1 | 3.214 | 3.052 | 2.690 | 2.912 | 2.623 | 1.905 | 1.850 | a |

| 2–4 | 8.694 | 7.948 | 7.176 | 6.983 | 7.109 | 6.798 | 6.167 | a |

| 5–10 | 7.214 | 6.322 | 4.914 | 4.911 | 5.397 | 5.129 | 4.517 | 3.799 |

Prevalence of various work and claiming behaviors among fully insured men, by lifetime earnings decile: Men claiming at age 62 and 3–11 months

| Decile | 1937 | 1938 | 1939 | 1940 | 1941 | 1942 | 1943 | 1944 |

|---|---|---|---|---|---|---|---|---|

| Panel A: Ceased work prior to claiming (not working at age 61 and not working at age 63) | ||||||||

| All | 2.090 | 2.114 | 2.293 | 2.039 | 2.297 | 2.611 | 2.202 | 2.259 |

| 1 | 9.394 | 10.446 | 11.228 | 6.271 | 7.104 | 9.619 | 9.898 | 8.471 |

| 2 | 4.326 | 3.643 | 3.509 | 2.912 | 4.267 | 3.908 | 3.515 | 4.284 |

| 3 | 0.989 | 1.526 | 1.754 | 1.906 | 2.516 | 2.476 | 1.943 | 1.850 |

| 4–9 | 0.845 | 0.861 | 0.897 | 1.438 | 1.367 | 1.493 | 0.971 | 1.217 |

| 10 | 1.114 | 0.353 | 1.054 | 0.673 | 0.875 | 1.144 | 0.833 | 0.682 |

| Panel B: Ceased work and claimed around the same time (working at age 61 and not working at age 63) | ||||||||

| All | 3.091 | 3.206 | 3.744 | 3.294 | 2.964 | 3.049 | 2.664 | 2.737 |

| 1 | 1.731 | 1.174 | 1.053 | 1.008 | 0.328 | 0.762 | 0.648 | 0.389 |

| 2–9 | 3.369 | 3.597 | 4.256 | 3.809 | 3.500 | 3.502 | 3.122 | 3.177 |

| 10 | 2.225 | 2.113 | 2.339 | 1.457 | 1.313 | 1.714 | 1.018 | 1.558 |

| Panel C: Worked after claiming (working at age 63) | ||||||||

| All | 4.142 | 3.523 | 3.498 | 3.518 | 3.194 | 2.830 | 2.951 | 2.863 |

| 2–9 | 4.497 | 3.817 | 3.905 | 4.019 | 3.705 | 3.311 | 3.446 | 3.348 |

| 1, 10 | 2.721 | 2.349 | 1.872 | 1.513 | 1.148 | 0.905 | 0.971 | 0.925 |

Prevalence of various work and claiming behaviors among fully insured men, by lifetime earnings decile: Men not claiming at age 62

| Decile | 1937 | 1938 | 1939 | 1940 | 1941 | 1942 | 1943 | 1944 |

|---|---|---|---|---|---|---|---|---|

| Panel A: Worked at age 63 | ||||||||

| All | 37.438 | 39.119 | 39.628 | 40.309 | 41.562 | 43.068 | 44.459 | 45.462 |

| 1 | 10.136 | 11.385 | 9.591 | 9.071 | 8.306 | 8.381 | 6.475 | 5.648 |

| 2 | 27.194 | 25.969 | 27.719 | 27.660 | 27.133 | 29.457 | 30.157 | 29.309 |

| 3 | 37.824 | 39.671 | 39.883 | 42.265 | 37.527 | 43.905 | 43.848 | 44.206 |

| 4–5 | 40.445 | 42.161 | 44.061 | 43.473 | 46.364 | 45.879 | 50.046 | 51.096 |

| 6–8 | 38.978 | 40.838 | 42.005 | 40.926 | 45.097 | 46.125 | 46.438 | 48.458 |

| 9 | 44.623 | 46.948 | 46.784 | 49.048 | 51.094 | 52.667 | 55.689 | 56.670 |

| 10 | 56.807 | 60.400 | 58.197 | 65.359 | 63.567 | 66.158 | 69.010 | 71.248 |

| Panel B: Did not work at age 63 | ||||||||

| All | 8.754 | 8.890 | 9.793 | 10.890 | 11.211 | 11.444 | 11.970 | 13.430 |

| 1 | 31.768 | 30.634 | 32.865 | 36.058 | 39.563 | 40.571 | 41.351 | 45.570 |

| 2 | 15.822 | 15.041 | 15.556 | 18.253 | 17.287 | 18.398 | 19.056 | 23.272 |

| 3 | 8.405 | 9.155 | 9.708 | 9.978 | 10.175 | 9.333 | 10.546 | 12.171 |

| 4, 5, 7–9 | 4.303 | 5.049 | 5.289 | 6.319 | 6.299 | 6.593 | 6.938 | 7.908 |

| 6 | 4.326 | 3.525 | 5.497 | 5.487 | 5.580 | 5.624 | 5.088 | 6.037 |

| 10 | 5.693 | 5.288 | 7.845 | 7.511 | 7.987 | 7.531 | 8.973 | 7.700 |

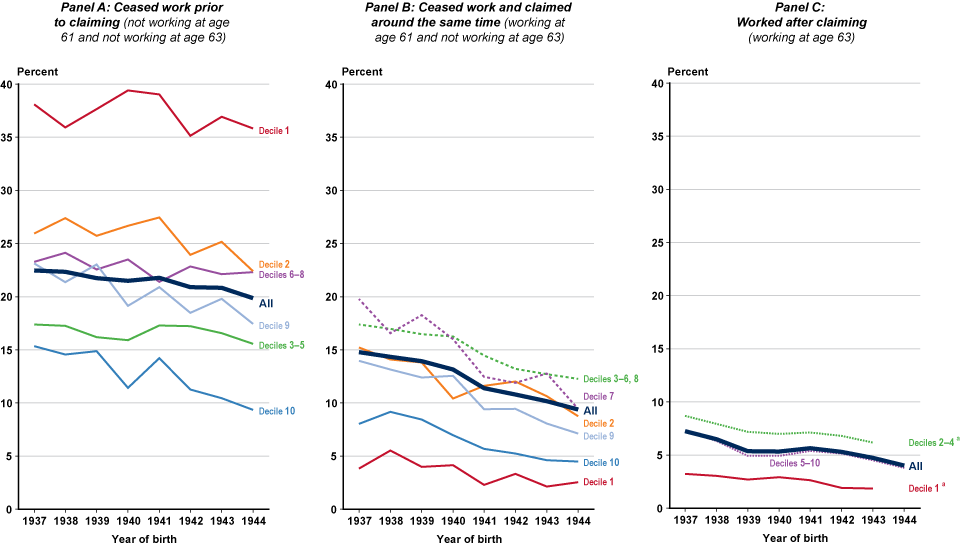

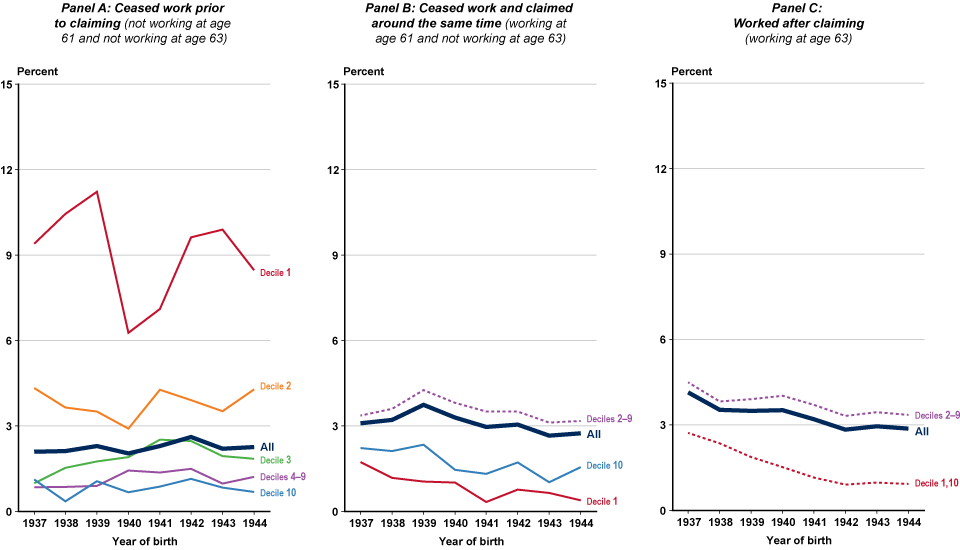

Category 1: Ceased Work Prior to Claiming at Age 62

This category is highlighted in Panel A of Charts 1–2 and Charts 4–5. Among work and claiming categories, men who ceased work prior to claiming represented the largest proportion of men who claimed on reaching age 62 (that is, at 62 and 0–2 months)—at about 20 percent of fully insured workers at the end of the observation period (Waldron 2020, Table 1 and Chart 2). When disaggregated, this category displayed sizable heterogeneity by lifetime earnings decile.

For example, for birth year 1944, the share of fully insured decile-1 earners in this category was 36 percent, while the share of decile-10 earners was 9 percent. In addition, the odds of being in this category were lower for workers in deciles 3–5 than for those in deciles 6–8, and the odds for decile 9 were close to those for decile 5, relative to decile 10 (Chart 1). Consequently, the difference in the shares of workers in this category between deciles 9 and 10 was a somewhat sizable 7–8 percentage points over the observation period.

The heterogeneity by decile in this category may be partially reflective of a group of workers who have withdrawn from substantial gainful activity prior to claiming for a wide variety of reasons. For example, Waldron (2004) found that men who claimed before full retirement age (FRA) and had pension income in the top half or top quarter of the earnings distribution were generally equal to age-65 retirees in the odds of self-reporting good health. Speculatively, some of these workers could appear in this category in the middle to upper deciles. On the other hand, also speculatively, support for this result might also be found in the discussion of the literature on physically demanding jobs in Waldron (2015, 12–14). For example, Rho (2010) found that substantial proportions of men holding physically demanding jobs were in higher wage quintiles than those traditionally included in hardship measures. Some of these workers may constitute part of the ceased-work-prior-to-claiming group in the data.

Compared to the slight downward trend in the share of fully insured workers in this category observed in aggregate (the dark blue line in Chart 4), trends in the proportion of men in this category have differed by decile, but not necessarily in expected ways. For example, the shares of fully insured workers in decile 1 and deciles 3–8 who were in this category were flat over the observation period, while the shares in deciles 2, 9, and 10 declined across the 1937–1944 birth cohorts (Chart 4 and Table 1).

If not for decile 2, one might be tempted to consider the role of health in the declining shares in this category in the upper deciles, as there is known to be a positive correlation between higher socioeconomic status categories and better health that has been generally widening over time. However, decile 2 had approximately the same downward slope on the year-of-birth variable as decile 9. With that said, none of these declines by decile, excluding that in decile 10, were very large.

The share of decile-2 workers also declined in the ceased work and claimed around the same time group. In contrast, the shares of decile-2 workers in the not claiming, still working group and the not claiming, not working group both increased. One possibility—not provable—that would explain the puzzle would be that some workers in poor health in decile 2 switched from the ceased work prior to claiming category to the not claiming, not working category. Speculatively, such a switch could occur in response to the statutory increases in the FRA for successive birth cohorts, which reduced the monthly benefit available to workers in later birth cohorts who claimed on reaching age 62.

Among men claiming later at age 62 (that is, at age 62 and 3–11 months), workers were most likely to be in this category, relative to decile 10, if they were in lifetime earnings deciles 1 and 2. Men in decile 3 were slightly more likely than men in decile 4 to be in this category, and statistically, men in deciles 4–10 were roughly indistinguishable.10 The proportion of men who claimed later at age 62 exhibited no trend over time for all 10 deciles (Charts 2 and 5 and Table 1).

One might question why any worker in this category would choose to claim at age 62 and 3–11 months rather than on reaching age 62 (to the last day of 62 and 2 months), given that these men had stopped working by age 61. While the reasons are unknown, it is important to keep in mind that in aggregate, of fully insured men born in (for example) 1944, only 2.3 percent were in this category.

Category 2: Ceased Work and Claimed Around the Same Time at Age 62

This category is highlighted in Panel B of Charts 1–2 and Charts 4–5. Overall, the share of fully insured men who both ceased work and claimed on reaching age 62 declined over time, and was under 10 percent by the end of the observation period (Chart 4). While the size of that decline over time has not been exactly the same across all the earnings deciles,11 the shares of men in this category who claimed on reaching age 62 have declined significantly in all deciles over time (Table 1). As shown in Chart 1, workers in the middle of the earnings distribution had the statistically highest odds of being in the group that ceased work and claimed around the same time, relative to decile 10. In terms of the size of those shares, most deciles were within 3 percentage points of the aggregate share, although the bottom and top of the distribution, or deciles 1 and 10, were further below that aggregate share.

It is important to keep in mind that this category is measuring fully insured workers who were working at age 61 and not working at age 63, and smaller shares of workers in deciles 1 and 2 were working at age 61 (for example, only 10.3 percent of decile-1 workers born in 1944; Appendix Chart A-1). In Appendix Chart A-2, Panel B shows the recalculated share of men in this category by decile, after restricting the denominator of each decile to men who were working at age 61. Comparing Panels A and B shows that among men in deciles 1–2 who were still working at age 61, the recalculated percentage who were potentially timing their claim to coincide with the cessation of substantial gainful activity moved from below to above the all-deciles average (around 19 percent for the 1944 birth cohort). With Panel B's more restricted denominator, deciles 1–2 contained the greatest proportion of individuals in this working and claiming category, followed by deciles 3–8. Deciles 9 and 10 contained a smaller-than-average proportion, with the difference between decile 9 and 10 narrowing over the observation period.

Patterns for workers in this group who claimed later at age 62 generally look similar to those of men who claimed on reaching age 62 although confidence intervals were larger, possibly because of this group's smaller sample size (Chart 2).

Category 3: Worked After Claiming at Age 62

This category is highlighted in Panel C of Charts 1–2 and Charts 4–5. Overall, the proportion of men who worked after claiming either on reaching age 62 or later at age 62 was small and declined over time (Charts 4 and 5). A downward trend was observed across most deciles for workers in this category who claimed on reaching age 62 and the trend was either downward or flat for men who claimed later at age 62 (Table 1). For men who claimed on reaching 62, decile-1 earners were the least likely to be in this category and those in deciles 2–4 were the most likely, relative to decile 10 (Chart 1).

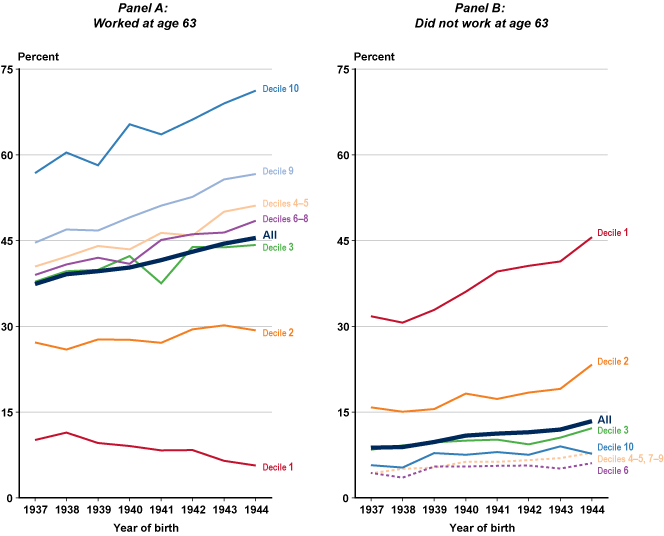

Category 4: Did Not Claim at Age 62, Still Worked at Age 63

This category is highlighted in Panel A of Charts 3 and 6. Overall, the percentage of fully insured workers who did not claim at age 62 and who were working at age 63 increased from 2000 through 2007 (that is, across birth years 1937–1944). When disaggregated by earnings decile, the share of workers in decile 1 who were in this category declined over time, while the shares in deciles 2–10 increased over time (Chart 6).

However, as seen on the chart, shares did not increase by the same amount over the 8-year period for deciles 2–10. While in aggregate the shares in this category increased by around 8 percentage points from birth cohort 1937 to birth cohort 1944, the share of decile-9 and decile-10 workers increased by 12 percentage points and 14 percentage points, respectively. Conversely, the increase in the share of decile-2 workers in this category was a statistically significant but modest 2 percentage points. The increase in shares for the middle of the earnings distribution hewed most closely to the size of the all-deciles increase, although deciles 4–5 were closer to the size of the decile 9 increase, at 11 percentage points.

Of all the working and claiming combinations, this category had the widest spread in the share of workers by lifetime earnings decile. By the end of the observation period, there was a 66 percentage-point difference in the shares of decile-10 and decile-1 workers in this category and a 27 percentage-point difference in the shares of decile-9 and decile-2 workers. The gap between decile 10 and the middle of the earnings distribution may also be noteworthy. The share of workers in deciles 4–8 in this category was approximately 21 percentage points lower than that of decile 10 by the end of the observation period. In addition, the odds of being in this category came closest to following a classic ladder-like gradient—that is, the higher the earnings decile, the more likely that a man did not claim at age 62 and was working at age 63. On the other hand, the middle of the earnings distribution (for example, deciles 4–8) was fairly flat relative to a ladder-like pattern (Chart 3).

While the EEA literature often stresses health differences between workers, the results for this category could also highlight differences in the demand for older workers in the labor market across lifetime earnings deciles (that is, at different wage levels). However, as the retirement literature has found, it is difficult to disentangle potential labor demand effects from potential labor supply effects, and is not attempted here.

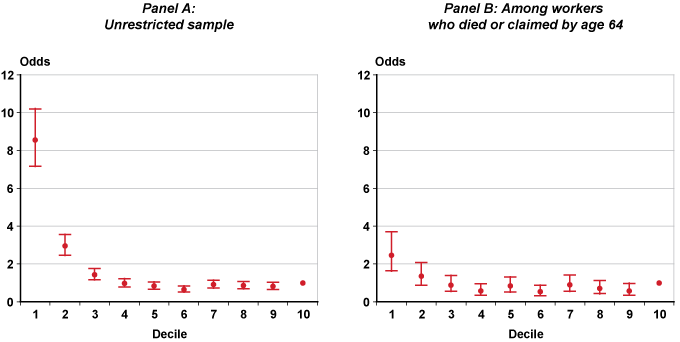

Category 5: Did Not Claim at Age 62 and Did Not Work at Age 63

This category is highlighted in Panel B of Charts 3 and 6. Overall, the share of fully insured workers not claiming at age 62 and not working at age 63 increased across birth years 1937–1944 and reached about 13 percent by the end of the observation period. When disaggregated by earnings decile, the share of men in this category in every earnings decile—except decile 6—increased significantly over time (Chart 6). Both the greatest share and the greatest increase over time were for the first decile.

While the all-decile average increased by about 5 percentage points from the beginning to the end of the observation period, decile 2 increased by about 7 percentage points and decile 1 rose by 14 percentage points. The differences in levels were starker. About 46 percent of men born in 1944 with lifetime earnings in the first decile were in this working and claiming category, followed by men with earnings in the second decile at 23 percent and the third decile at 12 percent. The remaining deciles were at around 8 percent by the end of the observation period.

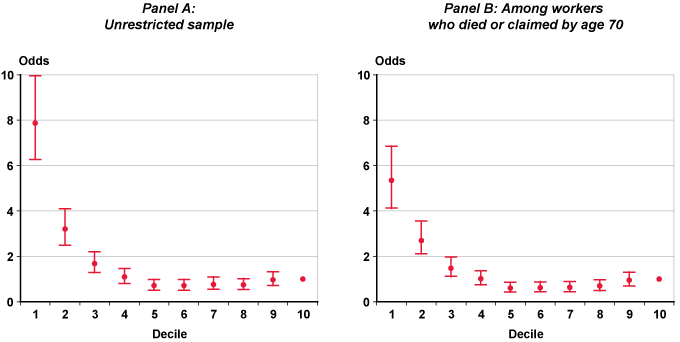

However, potential sensitivity concerns are raised by death reports possibly missing from the data, as the share of workers born in 1937 and 1938 in decile 1 decreased by 10 percentage points when the sample was restricted to workers who had either died or claimed by age 70 (see Appendix Chart B-1). Thus, the reader is cautioned that one cannot be sure of the precision of these estimates—with the possibility that the estimated shares of workers in this category are biased upward.

To further investigate this category of workers, Table 2 sums the percentage of workers in each decile who were in the not claiming, not working group for birth years 1942–1944. Then the shares of these men who claimed at age 63 or 64 were calculated. The share that had ceased work by age 61 and the share that was working at age 61 but not working at age 63 are also tabulated.

| Decile | Claimed at— | Total claiming through age 64 | Not working at age 63 and— | Total not working at age 63 | ||

|---|---|---|---|---|---|---|

| Age 63 | Age 64 | Not working at age 61 | Working at age 61 | |||

| 1 | 13 | 17 | 30 | 95 | 5 | 100 |

| 2 | 18 | 23 | 41 | 80 | 20 | 100 |

| 3 | 20 | 23 | 43 | 66 | 34 | 100 |

| 4 | 18 | 24 | 42 | 63 | 37 | 100 |

| 5 | 26 | 26 | 52 | 65 | 35 | 100 |

| 6 | 24 | 20 | 44 | 65 | 35 | 100 |

| 7 | 10 | 23 | 33 | 66 | 34 | 100 |

| 8 | 7 | 23 | 30 | 61 | 39 | 100 |

| 9 | 6 | 23 | 29 | 61 | 39 | 100 |

| 10 | 4 | 21 | 25 | 56 | 44 | 100 |

| SOURCE: Author's calculations using Social Security administrative data (see Waldron 2020). | ||||||

| NOTE: Sample excludes disabled-worker beneficiaries. | ||||||

In aggregate, the majority of men in this category were not working at age 61. When broken down by decile, those in decile 1 were the most likely to have ceased work by age 61. Because lower deciles dominate this working and claiming category, they drive the all-decile average. However, note that while the majority of men in the higher deciles also ceased work by age 61, the result is less stark. That is, while 95 percent of men in decile 1 and 80 percent of men in decile 2 ceased work in the year they turned age 61, the percentages were only 65 percent for decile 5 and 56 percent for decile 10.

Thus, men in the lower deciles appear to have postponed claiming for longer periods than did men in many of the higher earnings deciles. Also note that the shares who had claimed by age 64 were most similar between decile 1 and deciles 7–9. Of course, Table 2 does not solve the potential problem of missing deaths—in this case, if there are missing deaths in the denominator, then the shares claiming by age 64 will be underestimated. In addition, if deaths are more likely to be unreported at low earnings levels, there is an analytical mismatch when trying to compare shares across deciles. Nevertheless, the evidence presented here suggests that lower earners appear not to be any less able to delay the immediate gratification of the monthly benefit amount that can be obtained from a retired-worker benefit claim at age 62 than are men with higher lifetime earnings.

Summary of Differences in Claiming and Working Behavior Between and Within Lifetime Earnings Deciles

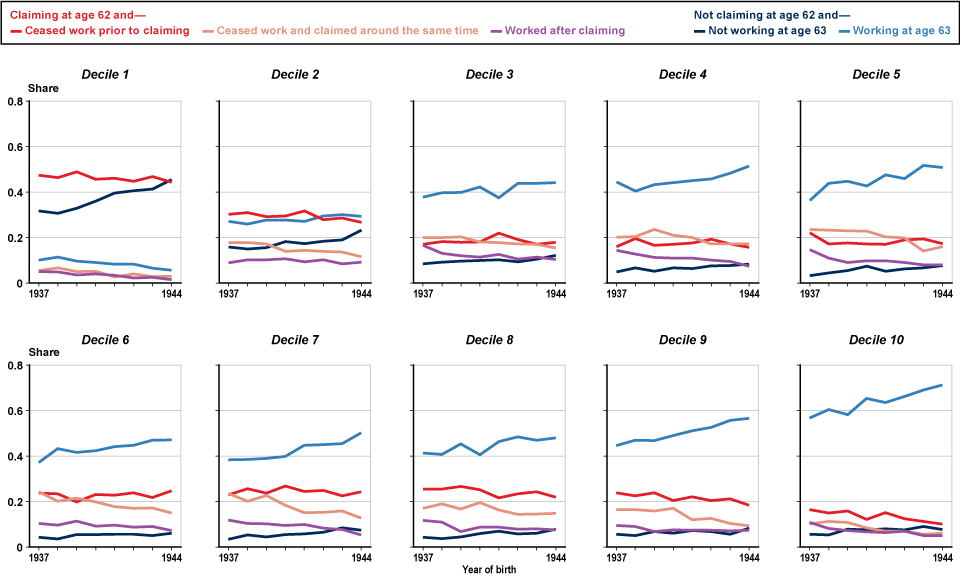

Chart 7 shows the year-by-year distribution of workers in each lifetime earnings decile by working and claiming category. Within each lifetime earnings decile depicted in the chart, the distribution of workers by category adds up to 1. Two main points are readily apparent. First, fully insured workers exhibit substantial heterogeneity in working and claiming behavior within lifetime earnings deciles 1–9. No one earnings and claiming category can be said to dominate any particular earnings decile. The decile that comes closest to being homogenous is decile 10, although even there, about 30 percent of the workers split among disparate working and claiming categories at the end of the observation period.

Distributions of fully insured men by working and claiming category and year of birth: Each lifetime earnings decile

| Category | 1937 | 1938 | 1939 | 1940 | 1941 | 1942 | 1943 | 1944 |

|---|---|---|---|---|---|---|---|---|

| Decile 1 | ||||||||

| Claiming at age 62 and— | ||||||||

| Ceased work before claiming | 0.475 | 0.464 | 0.489 | 0.457 | 0.461 | 0.448 | 0.468 | 0.443 |

| Ceased work and claimed around the same time | 0.056 | 0.067 | 0.050 | 0.052 | 0.026 | 0.041 | 0.028 | 0.029 |

| Worked after claiming | 0.051 | 0.049 | 0.036 | 0.040 | 0.034 | 0.022 | 0.026 | 0.016 |

| Not claiming at age 62 and— | ||||||||

| Not working at age 63 | 0.318 | 0.306 | 0.329 | 0.361 | 0.396 | 0.406 | 0.414 | 0.456 |

| Working at age 63 | 0.101 | 0.114 | 0.096 | 0.091 | 0.083 | 0.084 | 0.065 | 0.056 |

| Decile 2 | ||||||||

| Claiming at age 62 and— | ||||||||

| Ceased work before claiming | 0.303 | 0.310 | 0.292 | 0.296 | 0.317 | 0.278 | 0.287 | 0.267 |

| Ceased work and claimed around the same time | 0.178 | 0.177 | 0.172 | 0.139 | 0.144 | 0.140 | 0.136 | 0.116 |

| Worked after claiming | 0.089 | 0.102 | 0.103 | 0.106 | 0.094 | 0.103 | 0.085 | 0.092 |

| Not claiming at age 62 and— | ||||||||

| Not working at age 63 | 0.158 | 0.150 | 0.156 | 0.183 | 0.173 | 0.184 | 0.191 | 0.233 |

| Working at age 63 | 0.272 | 0.260 | 0.277 | 0.277 | 0.271 | 0.295 | 0.302 | 0.293 |

| Decile 3 | ||||||||

| Claiming at age 62 and— | ||||||||

| Ceased work before claiming | 0.171 | 0.182 | 0.180 | 0.182 | 0.219 | 0.191 | 0.171 | 0.179 |

| Ceased work and claimed around the same time | 0.200 | 0.200 | 0.204 | 0.182 | 0.178 | 0.171 | 0.171 | 0.154 |

| Worked after claiming | 0.167 | 0.130 | 0.120 | 0.114 | 0.126 | 0.105 | 0.114 | 0.103 |

| Not claiming at age 62 and— | ||||||||

| Not working at age 63 | 0.084 | 0.092 | 0.097 | 0.100 | 0.102 | 0.093 | 0.105 | 0.122 |

| Working at age 63 | 0.378 | 0.397 | 0.399 | 0.423 | 0.375 | 0.439 | 0.438 | 0.442 |

| Decile 4 | ||||||||

| Claiming at age 62 and— | ||||||||

| Ceased work before claiming | 0.161 | 0.196 | 0.166 | 0.170 | 0.176 | 0.193 | 0.172 | 0.157 |

| Ceased work and claimed around the same time | 0.201 | 0.204 | 0.235 | 0.211 | 0.200 | 0.172 | 0.172 | 0.172 |

| Worked after claiming | 0.143 | 0.128 | 0.112 | 0.110 | 0.109 | 0.101 | 0.095 | 0.074 |

| Not claiming at age 62 and— | ||||||||

| Not working at age 63 | 0.049 | 0.067 | 0.053 | 0.067 | 0.063 | 0.076 | 0.077 | 0.083 |

| Working at age 63 | 0.445 | 0.404 | 0.433 | 0.442 | 0.451 | 0.459 | 0.484 | 0.514 |

| Decile 5 | ||||||||

| Claiming at age 62 and— | ||||||||

| Ceased work before claiming | 0.220 | 0.173 | 0.177 | 0.172 | 0.171 | 0.190 | 0.194 | 0.173 |

| Ceased work and claimed around the same time | 0.235 | 0.234 | 0.230 | 0.229 | 0.204 | 0.198 | 0.141 | 0.161 |

| Worked after claiming | 0.147 | 0.110 | 0.090 | 0.099 | 0.098 | 0.090 | 0.080 | 0.080 |

| Not claiming at age 62 and— | ||||||||

| Not working at age 63 | 0.033 | 0.045 | 0.055 | 0.074 | 0.051 | 0.063 | 0.068 | 0.078 |

| Working at age 63 | 0.364 | 0.439 | 0.448 | 0.427 | 0.476 | 0.459 | 0.517 | 0.508 |

| Decile 6 | ||||||||

| Claiming at age 62 and— | ||||||||

| Ceased work before claiming | 0.237 | 0.234 | 0.199 | 0.232 | 0.229 | 0.238 | 0.218 | 0.247 |

| Ceased work and claimed around the same time | 0.244 | 0.202 | 0.215 | 0.198 | 0.177 | 0.170 | 0.172 | 0.149 |

| Worked after claiming | 0.104 | 0.096 | 0.115 | 0.092 | 0.096 | 0.088 | 0.090 | 0.072 |

| Not claiming at age 62 and— | ||||||||

| Not working at age 63 | 0.043 | 0.035 | 0.055 | 0.055 | 0.056 | 0.056 | 0.051 | 0.060 |

| Working at age 63 | 0.372 | 0.432 | 0.416 | 0.423 | 0.442 | 0.448 | 0.469 | 0.471 |

| Decile 7 | ||||||||

| Claiming at age 62 and— | ||||||||

| Ceased work before claiming | 0.230 | 0.257 | 0.237 | 0.268 | 0.245 | 0.250 | 0.225 | 0.242 |

| Ceased work and claimed around the same time | 0.235 | 0.202 | 0.227 | 0.184 | 0.151 | 0.152 | 0.159 | 0.128 |

| Worked after claiming | 0.119 | 0.103 | 0.102 | 0.095 | 0.099 | 0.083 | 0.077 | 0.054 |

| Not claiming at age 62 and— | ||||||||

| Not working at age 63 | 0.033 | 0.053 | 0.044 | 0.055 | 0.058 | 0.065 | 0.085 | 0.074 |

| Working at age 63 | 0.383 | 0.385 | 0.390 | 0.399 | 0.447 | 0.450 | 0.454 | 0.502 |

| Decile 8 | ||||||||

| Claiming at age 62 and— | ||||||||

| Ceased work before claiming | 0.255 | 0.255 | 0.267 | 0.252 | 0.217 | 0.235 | 0.243 | 0.219 |

| Ceased work and claimed around the same time | 0.171 | 0.190 | 0.167 | 0.195 | 0.163 | 0.144 | 0.145 | 0.148 |

| Worked after claiming | 0.117 | 0.109 | 0.068 | 0.087 | 0.088 | 0.078 | 0.080 | 0.075 |

| Not claiming at age 62 and— | ||||||||

| Not working at age 63 | 0.043 | 0.038 | 0.044 | 0.059 | 0.069 | 0.058 | 0.061 | 0.078 |

| Working at age 63 | 0.414 | 0.408 | 0.454 | 0.406 | 0.464 | 0.485 | 0.470 | 0.480 |

| Decile 9 | ||||||||

| Claiming at age 62 and— | ||||||||

| Ceased work before claiming | 0.239 | 0.225 | 0.239 | 0.204 | 0.221 | 0.205 | 0.212 | 0.183 |

| Ceased work and claimed around the same time | 0.164 | 0.164 | 0.158 | 0.170 | 0.120 | 0.127 | 0.104 | 0.093 |

| Worked after claiming | 0.095 | 0.090 | 0.068 | 0.075 | 0.074 | 0.074 | 0.071 | 0.074 |

| Not claiming at age 62 and— | ||||||||

| Not working at age 63 | 0.056 | 0.050 | 0.068 | 0.060 | 0.073 | 0.068 | 0.056 | 0.083 |

| Working at age 63 | 0.446 | 0.469 | 0.468 | 0.490 | 0.511 | 0.527 | 0.557 | 0.567 |

| Decile 10 | ||||||||

| Claiming at age 62 and— | ||||||||

| Ceased work before claiming | 0.165 | 0.149 | 0.159 | 0.121 | 0.151 | 0.124 | 0.113 | 0.100 |

| Ceased work and claimed around the same time | 0.103 | 0.113 | 0.108 | 0.084 | 0.070 | 0.070 | 0.056 | 0.060 |

| Worked after claiming | 0.108 | 0.081 | 0.073 | 0.066 | 0.063 | 0.070 | 0.051 | 0.050 |

| Not claiming at age 62 and— | ||||||||

| Not working at age 63 | 0.057 | 0.053 | 0.078 | 0.075 | 0.080 | 0.075 | 0.090 | 0.077 |

| Working at age 63 | 0.568 | 0.604 | 0.582 | 0.654 | 0.636 | 0.662 | 0.690 | 0.712 |

Second, there are also differences between lifetime earnings deciles in the share of workers occupying various working and claiming categories. Chart 7 indicates that it would be empirically incorrect to characterize the middle of the earnings distribution as similar to the top of the distribution in terms of working and claiming behavior at the EEA. It appears that on average, the lowest earners generally exhibit a different mix of behaviors from those in the middle of the earnings distribution, who in turn exhibit a different mix from those at the top. At the same time, a significant share of men in any particular earnings decile share work and claiming behaviors with workers in lifetime earnings deciles both lower and higher than their own.

Mortality Risk by Working and Claiming Category

Although the set of variables available in SSA data is limited, it is possible to link earnings and benefit data with death data. One would expect mortality risk and underlying health to be correlated.12 As such, a significant correlation between increased risk of death and claiming at age 62 could indicate that an age-62 claim correlates with difficulty or disadvantage in the labor market (Waldron 2015 reviews links between early claiming and poor health). Conversely, a lack of correlation between working and claiming behavior and mortality risk in SSA data, or a correlation that moves in an unexpected direction, would weaken the conclusion reached in Waldron (2020) that one cannot rule out that at least some workers self-sort or self-select into working and claiming categories based on their life circumstances.

For the proceeding discussion, one note of caution concerns the reference variable used—the category of not claiming at age 62 and still working at age 63. In Waldron (2001), comparing age-62 retired-worker claimants to all other retired-worker claimants attenuated the risk of death for men who claimed at the earliest ages versus men claiming later. This is because—when disaggregated—men claiming at age 63 were found to have higher risk of death than those claiming at age 64, and those claiming at age 64, in turn, had a higher risk of death than those claiming at age 65. Waldron (2001, 2002, 2004) also found that men claiming on reaching age 62 had higher risk of death than men claiming later at age 62. As shown in the regression results in Appendix Tables C-1 and C-2, for the sample used in this paper, that result is reversed—men claiming later at age 62 had higher odds of death relative to those not claiming at age 62 and still working at age 63 than did men retiring on reaching age 62. The sample used in this paper is younger, smaller, and compares men claiming on reaching age 62 and later at age 62 to a different reference variable throughout a smaller range of ages at death. For those reasons, it cannot be determined here whether older findings regarding differences in mortality risk within the age-62 category have been fully overturned in more recent birth cohorts; for that, more research is needed.

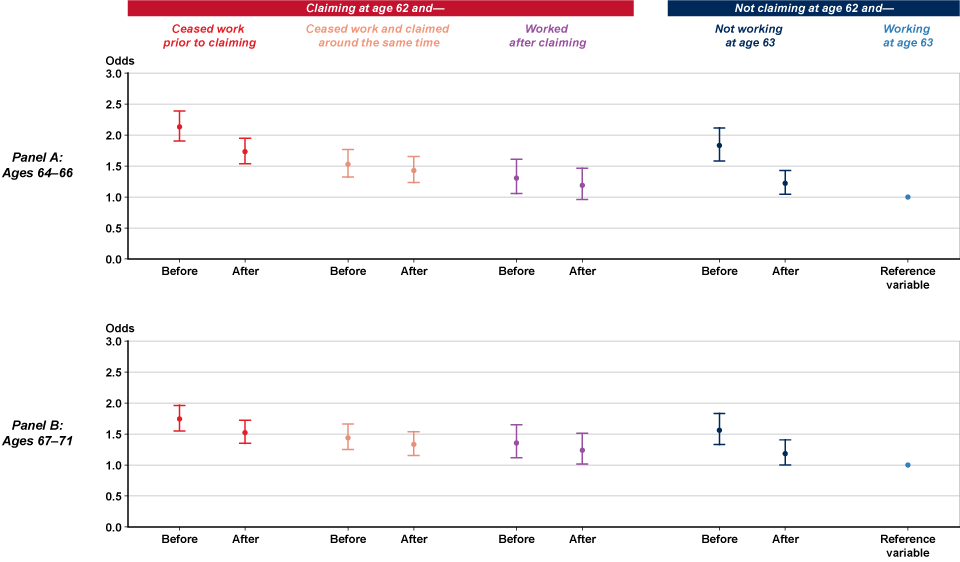

Chart 8 plots the odds of dying at ages 64–66 and 67–71 for fully insured men in various working and claiming categories relative to fully insured men not claiming at age 62 and still working at age 63. Appendix Tables C-1 and C-2 contain the accompanying regressions and Waldron (2013) contains technical details concerning the type of regression model specified.

Odds of dying at ages 64–66 and 67–71 for fully insured men in various working and claiming categories, before and after controlling for lifetime earnings

| Category | Before controlling for lifetime earnings decile | After controlling for lifetime earnings decile | ||||

|---|---|---|---|---|---|---|

| Point estimate | Confidence interval | Point estimate | Confidence interval | |||

| Upper bound | Lower bound | Upper bound | Lower bound | |||

| Panel A: Ages 64–66 | ||||||

| Claiming at age 62 and— | ||||||

| Ceased work before claiming | 2.133 | 2.389 | 1.905 | 1.732 | 1.950 | 1.539 |

| Ceased work and claimed around the same time | 1.529 | 1.769 | 1.322 | 1.430 | 1.655 | 1.235 |

| Worked after claiming | 1.306 | 1.611 | 1.059 | 1.189 | 1.468 | 0.964 |

| Not claiming at age 62 and— | ||||||

| Not working at age 63 | 1.832 | 2.119 | 1.584 | 1.222 | 1.430 | 1.044 |

| Working at age 63 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| Panel B: Ages 67–71 | ||||||

| Claiming at age 62 and— | ||||||

| Ceased work before claiming | 1.746 | 1.966 | 1.551 | 1.527 | 1.726 | 1.351 |

| Ceased work and claimed around the same time | 1.443 | 1.664 | 1.252 | 1.335 | 1.541 | 1.157 |

| Worked after claiming | 1.359 | 1.654 | 1.118 | 1.242 | 1.512 | 1.021 |

| Not claiming at age 62 and— | ||||||

| Not working at age 63 | 1.564 | 1.835 | 1.333 | 1.188 | 1.409 | 1.002 |

| Working at age 63 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

Chart 8 shows odds ratios before and after controlling for lifetime earnings deciles. Relative to men in the not claiming, still working group, and before controlling for earnings, the odds of dying at ages 64–66 were 2.13, 1.53, and 1.31 times greater for men ceasing work prior to claiming, ceasing work and claiming around the same time, and working after claiming, respectively. Before controlling for earnings, the odds of dying at ages 64–66 for men in the not claiming, not working group were 1.83 times greater than those for men in the not claiming, still working group. Odds of dying at ages 67–71 for age-62 claimants and non-claimants who had ceased work relative to non-claimants who were still working followed a similar pattern.

Waldron (2020) found that the majority of workers in the not claiming, not working group were not working at both ages 61 and 63. Thus, before controlling for lifetime earnings decile, the highest odds of death observed were for workers not working at both age 61 and age 63 and claiming at age 62, or ceasing work prior to claim (2.13), relative to those in the not claiming, still working group. The next highest odds observed (1.83) were for workers in the not claiming, not working group (that is, where the majority were not working at age 61 and 63 and not claiming at age 62). This result is consistent with the strong correlation between labor force participation and health that is often observed in the public health and economics literature.13 This result also seems to highlight heterogeneity in life circumstances in the underlying population in that one sees some workers who ceased work prior to age 62 choosing to claim and others in the same situation choosing to postpone claiming.

In addition, note that all observed claiming categories had statistically significant higher odds of death than the group of workers one would presuppose to be the healthiest: those who did not claim at age 62 and who were working at age 63. Thus, results are consistent with both the public health literature (via the negative correlation between working at age 63 and subsequent mortality risk) and the adverse selection literature (via the negative correlation between age of claim and subsequent mortality risk). This suggests that we cannot rule out the possibility that at least some workers self-selected or self-sorted into working and claiming categories based on their life circumstances.

However, recall that, relative to the top earnings decile, workers in both the lower and middle deciles were both more likely to be out of the labor force prior to claiming (Chart 1) and to exhibit higher mortality risk at ages 63–66 and 67–71 (Waldron 2013). In addition, workers in the middle earnings deciles were more likely to cease work and claim simultaneously, relative to the top decile.

If the reason workers in these working and claiming categories exhibited higher mortality risk is that they were more likely to have lower earnings, then the correlation between claiming and mortality risk should not hold after controlling for lifetime earnings. Chart 8 shows that the odds of death were still higher for men in these categories relative to men not claiming and still working even after controlling for lifetime earnings, at 1.73, 1.43, and 1.19, respectively. This result suggests an independent positive correlation between these working and claiming behaviors and risk of death.14

The category of workers who did not claim at age 62 but who were also not working at age 63 is the most strongly affected by including the earnings deciles in the regression. This result is undoubtedly driven by the fact that this category is dominated by workers in the bottom two earnings deciles, for which the odds of death have been observed as the highest, relative to the top decile (Waldron 2013). After controlling for earnings decile, the odds of dying for men in this working and claiming category dropped from 1.83 to 1.22 and from 1.56 to 1.19 at ages 64–66 and 67–71, respectively. One might hypothesize that this category would consist of healthy and wealthy men choosing not to work (that is, following what economists sometimes refer to as a positive “income effect”). However, even after controlling for a man's position in the lifetime earnings distribution for his year of birth, there appears to be some correlation with greater morality risk, although the lower confidence interval is close to 1.

One hypothesis could be that individuals in the not claiming at age 62 and not working at age 63 category wait to claim to increase the size of their monthly benefit when they do claim. In other words, some workers facing the prospect of receiving a small monthly benefit amount may find it more utility maximizing to postpone claiming to increase the monthly benefit amount, in spite of an elevated risk of death or poor health. This hypothesis would be consistent with the domination of this category by men in earnings deciles 1 and 2 (Chart 3, Panel B). Other workers (such as some of those ceasing work prior to claiming) may find that their liquidity constraints at age 62 or health prospects outweigh the higher monthly benefit amount that could be obtained by forgoing benefits at age 62.

Additionally, some workers may consider the effect of their claim on spouse and survivor benefit entitlements based on the worker's record, and may postpone claiming for that reason. Some workers may rely on support from friends and family, while others may not have that option. Some may consider the impact of claiming on other income such as means-tested cash or in-kind benefits outside the scope of OASDI, such as state welfare payments. An important caveat to this speculative discussion is that some workers who obtained their earnings credits early in their careers could be unaware of their benefit eligibility.15 More research could explore this category of workers.

While the confidence intervals of the three working and claiming categories overlap to some extent, the qualitative pattern of risk of death after controlling for earnings decile is nevertheless striking in that it seems to track correlations between labor force participation and health that have long been observed in the literature. That is, those out of the labor force prior to claiming have the highest odds of dying, followed by those who time their withdrawal to coincide with their claim, followed by those who claim and continue to work. In this way, one cannot rule out the possibility that at least some workers self-select or self-sort into working and claiming categories based on their life circumstances.

Empirical Results in the Context of Previous Literature

This paper is not the first study to explore heterogeneity in working and claiming behavior. Previous work spans 50 years and includes Epstein (1966) observing men entitled at age 62 in 1963, Sherman (1985) observing Social Security beneficiaries who had retired-worker benefits first payable from June 1980–May 1981, Pattison (2014) observing the male native-born 1930 birth cohort (age 62 in 1992), Government Accountability Office (GAO) (2014) observing workers born from approximately 1938 through 1948 (age 62 from 2000 through 2010), and Bosworth, Burtless, and Zhang (2016) observing birth cohorts 1943–1945 (age 62 in years 2005–2007). All these papers found that working and claiming behavior was not homogenous at age 62.16

Epstein (1966) used an earlier version of the Social Security earnings data used here, and found substantial heterogeneity among the Social Security–covered worker population. When considering Epstein's results, it is important to be aware that the early Continuous Work History Sample file that Epstein used recorded only covered earnings, and excluded earnings exceeding the Social Security taxable maximum. This means that some workers recorded in Epstein's data as not working in covered employment could have worked in non-covered employment. Therefore, Epstein's estimates are not directly comparable to this paper's estimates. This paper counts earnings in non-covered employment as work because non-covered earnings are available in more recent Social Security earnings data. The fact that Social Security coverage was much less common for the birth cohorts observed by Epstein exacerbates this non-comparability. However, in spite of these limitations, Epstein (1966) is an important historical study—both for its methodological approach and for the light it sheds on the underlying heterogeneity in the fully insured population that may have been present when the EEA option was first adopted by Congress in 1961.

For example, Epstein (1966) found that 31 percent of men entitled at age 62 in 1963 had no covered earnings recorded in the preceding year (compared with 20 percent of men entitled at age 65). She also found that men entitled at age 62 had a lower level of average earnings than men entitled at age 65, and that men not working in the year before age-62 entitlement had a lower level of earnings when last employed and showed more of a decline between their peak year of earnings and their last year of earnings. However, she also found that 18 percent of male workers claiming at age 62 had strong labor force attachment prior to claiming and earnings at or above the taxable maximum in at least one year prior to claiming.

Using workers' self-reported current employment status and time since leaving their last job, Sherman (1985, Table A) found 32.3 percent of male beneficiaries and 52.5 percent of female beneficiaries entitled at age 62 with retired-worker benefits first payable June 1980–May 1981 had stopped work 13 or more months prior to claiming. An additional 9.1 percent of men and 6.2 percent of women had stopped working 7–12 months prior to claiming.17 Further, 18.4 percent of men and 9.1 percent of women stopped working 1–6 months before claiming; 9.6 percent of men and 4.5 percent of women stopped working in the month of first benefit receipt; and 5.9 percent of men and 4.9 percent of women stopped working in the 1–6 months after first benefit receipt. Only 2.5 percent of male and 1.3 percent of female age-62 claimants reported eligibility for Social Security benefits as the reason they left their last job (Sherman 1985, Table B).

Pattison (2014) found that about half of the male native-born 1930 birth cohort that claimed at age 62 and 0–1 months had already stopped working (with “working” defined as having earnings above one-third of the average wage) by age 60. In addition, Bosworth, Burtless, and Zhang (2016) found that 23 percent of men and 35 percent of women in the 1943–1945 birth cohorts had ceased work 2 years before making a retired-worker benefit claim. That finding, that the largest share of age-62 claimants ceased work prior to claiming, is roughly consistent with this paper's results.

Also consistent with my results, several studies have observed the presence of workers who appeared to have ceased work, but who had not yet claimed, even though they were eligible (Epstein 1966; Coile and others 2002; Pattison 2014). Using data self-reported to the Health and Retirement Study survey by workers born from 1938 through 1948 (age 62 in 2000–2010), GAO (2014) found that respondents in the lowest income and wealth quartiles were more likely to delay claiming than were those with moderate income and wealth. Among men entitled at age 65 in 1963 who had ceased work in covered employment before 1962, Epstein (1966, 8) found that a large share had relatively low earnings (55.7 percent), while a smaller share of workers who ceased work but waited to claim had high earnings (4 percent).18 In this paper, the shares of workers in deciles 1 and 2 who did not claim at age 62 but who also did not work at age 63 were above 20 percent at the end of the observation period, while the shares in deciles 4–10 were all below 10 percent.

GAO (2014, 20 and Figure 6) found that men in the middle wealth quartiles were more likely to claim early (either prior to the FRA or at age 62 when estimates from quartiles 2 and 3 are averaged together), after controlling for other factors, than workers in the lowest and highest wealth quartiles. Among the factors GAO controlled for were education and self-reported health, type of occupation, and type of labor force status at an age between 60 and 62 (GAO 2014, Table 4). The Social Security administrative data used in this paper do not allow controls for the factors observed by GAO; however, even without those controls, I find that a relatively sizable group of men in the middle of the earnings distribution claimed at age 62. Workers in the middle deciles were also the most likely to be in the (relatively small) cease work and claim around the same time category.

Pattison (2014) examined working and claiming patterns for the 1930 native-born male birth cohort in all deciles combined, by claiming age (62 and 0–1 months, 62 and 2–11 months, 63, 64, and 65). With a broader range of entitlement ages than this paper's, he found that about one-third stopped working (with “working” defined as having earnings at one-third or more of the average wage) before they claimed, about one-third were still working a year after claim, and about one-third were working a year before claiming and no longer working a year after claim.

Pattison also found that the cease work and claim around the same time category was a smaller proportion of men who claimed at ages 62 and 0–1 months and 65 (the FRA for that birth cohort) and a larger proportion of men who claimed at ages 62 and 2–11 months, 63, and 64. (At age 65, men who both claimed and continued to work constituted the largest proportion.)

Bosworth, Burtless, and Zhang (2016) also focused on a broader range of entitlement ages than does this paper. Defining retirement (or the cessation of work) as beginning when a worker last reported earnings (defined as earnings below the 2005 minimum wage multiplied by 1000 hours), they found that the distribution of the age at which work ceased was wider than the distribution of the age of a retired-worker benefit claim. For example, for birth years 1943–1945 (workers aged 62 in 2005–2007), they found that 42 percent of male and 39 percent of female retired-worker beneficiaries worked at least 2 years after the year they claimed benefits. The authors also found that 23 percent of men and 35 percent of women had ceased work 2 years before claiming a retired-worker benefit, as noted previously.

In this paper, the proportion of men not claiming at age 62 and working at age 63 generally followed a gradient by lifetime earnings decile (that is, the higher the decile, the more likely that a worker was in this working and claiming category). An intriguing study by Palmore (1964) suggests that this gradient with respect to substantial labor force participation at older ages may not necessarily be new. Under the heading “Higher-Paid Men Less Likely to Retire,” Palmore discussed the results of a 1963 Survey of the Aged in which “retirement” was defined as not working at a regular, full-time job within the past 5 years, and a variety of occupations proxied for a variety of wage levels. For men aged 65 or older, he found that less than one-third of professional or technical workers had stopped working full time in 1962, but about two-thirds of craftsmen and foremen had done so. He further noted that similar findings were reported in a 1952 study of the aged. In addition, when looking across the 11 occupational categories in his study (Table 2), one sees a gradient across the occupations in terms of the share of workers who were retired at age 65. Professional and technical workers had the lowest share, at 31 percent; the shares for managers, officials, and proprietors were 43 percent; for clerical and sales workers, 53 and 54 percent, respectively. The highest shares were for operators, other laborers, and craftsmen and foremen, at 60, 61, and 65 percent, respectively.

Palmore further noted, “The pattern probably results from a combination of factors. The higher-paid men, in general, have less physically demanding work, their jobs are more interesting and more rewarding, they have better health, and their retirement is less likely to be compulsory” (1964, 4). Other than the mention of compulsory retirement, Palmore's observation seems to suggest continuity over time, as these same factors appear in much more recent literature.

A small body of empirical literature estimates the correlation between length of life and retired-worker benefit claiming age. This literature resides within a larger body of adverse-selection literature concerned with private insurance markets (Heidler, Leifels, and Raffelhüschen 2006 provide a review and theoretical discussion). Using Social Security administrative data, Wolfe (1983), Duggan and Soares (2001), and Waldron (2001, 2002, 2004) all found that male workers who claim benefits early die sooner, on average, than male workers who claim benefits later. Wolfson and others (1993) observed the same link between claiming age and mortality risk for Canadian workers.

The correlations between mortality risk and benefit claiming at age 62 found in this paper are consistent with that adverse-selection literature. In addition, Waldron (2004) found that men in the top quartile of the lifetime earnings distribution who claimed benefits at age 62 were more likely to die sooner than men claiming later, even among men claiming later in lower lifetime earnings quartiles. In other words, even workers in the top lifetime earnings quartile were not homogenous with regard to mortality risk. The fact that claiming at age 62 was still correlated with heightened mortality risk, even after controlling for a man's position in the lifetime earnings distribution for his birth cohort, was consistent with that finding. These results suggest that a man's lifetime earnings decile may not always proxy for his exposure to a heightened risk of adversity in old age.

In summary, empirical analyses of claiming and retirement behavior that look for heterogeneity and complexity often find it, and the heterogeneity does not appear to be limited to any one historical period or group of birth cohorts. A logical extension of this paper would be to try to extend backward the observation period for working and claiming behavior, to shed more light on the previous literature.

Conclusion

At both levels of disaggregation—that is, by sex for all earnings deciles combined, in Waldron (2020); and for men by lifetime earnings decile, in this paper—fully insured workers were distributed among multiple working and claiming categories, rather than being concentrated in one particular working and claiming category. The least heterogeneous decile was decile 10. By the end of the observation period, 70 percent of workers in that earnings decile were concentrated in the not claiming, still working category, and that decile also exhibited the greatest increase in the share of workers in that category over time.

Overall, the best way to describe working and claiming behavior at the EEA in the SSA data would be to say that it was heterogeneous, but on average, it was also found to follow patterns that would have been predicted from the public-health and adverse-selection literature. In this paper, on average, the lowest lifetime earners generally had a different mix of working and claiming experiences than workers in the middle of the earnings distribution, and those in the middle generally had a different mix than those at the top. At the same time, a significant proportion of men in any particular earnings decile shared work and claiming behaviors with workers in lifetime earnings deciles both lower and higher than their own. In addition, the correlation between mortality risk and any age-62 claiming category, relative to men not claiming at age 62 and still working at age 63, remained; and it was in the expected direction, even after controlling for a fully insured man's position in the lifetime earnings distribution. To the extent that some of the working and claiming behaviors observed can proxy for a hazard or an adverse event of some kind, one cannot rule out potential exposure to that hazard for a worker at any level of the earnings distribution.

One way to interpret the results presented here would be to say that current-law equality in the option to claim at age 62 by career earnings level provides insurance value for workers who experience a hazard or vicissitude at or before age 62. There appears to be some evidence in the SSA data to suggest that some workers at the middle and top end of the lifetime earnings distribution may be making use of that insurance.

The observation that workers at any earnings decile may be exposed to adversity is not new. For example, Lyman (1928), speaking at the first National Conference on Old-Age Security, noted,

The very fact of this conference indicates that something is going to be done about the industrial classes. In the meanwhile there is the problem of the professional and business men. Well along in life, through some misfortune due to no fault of their own, they are suddenly swept from security into destitution…Here in New York City, the matter is being considered from the point of view of various churches, but the problem requires broader treatment. My suggestion is that this conference take into consideration this vital problem of old age dependency among these professional classes.

This observation was echoed in the 1935 Report of the Committee on Economic Security (https://www.ssa.gov/history/reports/ces.html), which provided the foundation for current law Old-Age Insurance (OAI), or the retired-worker benefit. The report noted that “it is to be expected that some people from higher income groups will come to financial grief and dependence in old age.”

Appendix A: Additional Information on Workers Who Ceased Work and Claimed Around the Same Time at Age 62

This appendix provides additional information on the cease work and claim category, when the base, or denominator, consists of those who were still working at age 61.

The main text gives readers a rough gauge of the share of the fully insured population in each earnings decile who ceased work and claimed benefits around the same time at age 62. However, the shares of men in this category may be lower for some lifetime earnings deciles because the bulk of workers in those deciles were not working at age 61.

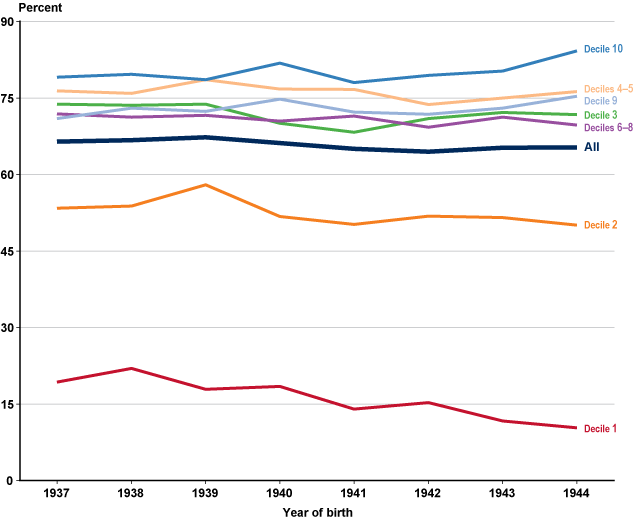

For example, decile 1 had the lowest share of fully insured workers who ceased work and claimed around the same time, with only 2.5 percent of workers in the 1944 birth cohort. Yet that birth cohort and earnings decile combination also had the lowest share of men who were working at age 61 (10.3 percent; Chart A-1). Shares of men in decile 2 who were working at age 61 were also lower than the all-decile average in all years observed, while the shares in deciles 3–10 were above the all-decile average in all years observed. Decile 10 always had the highest proportion working at age 61, and those in deciles 3–9 were fairly close, particularly toward the end of the observation period.

Percentage of fully insured men working at age 61, by lifetime earnings decile and year of birth

| Decile | 1937 | 1938 | 1939 | 1940 | 1941 | 1942 | 1943 | 1944 |

|---|---|---|---|---|---|---|---|---|

| All | 66.481 | 66.753 | 67.263 | 66.177 | 65.044 | 64.450 | 65.227 | 65.329 |

| 1 | 19.283 | 21.948 | 17.895 | 18.477 | 13.989 | 15.238 | 11.656 | 10.321 |

| 2 | 53.399 | 53.819 | 58.012 | 51.736 | 50.219 | 51.859 | 51.526 | 50.049 |

| 3 | 73.795 | 73.592 | 73.801 | 70.067 | 68.271 | 70.952 | 72.155 | 71.762 |

| 4–5 | 76.376 | 75.925 | 78.584 | 76.751 | 76.654 | 73.749 | 74.977 | 76.279 |

| 6–8 | 71.858 | 71.222 | 71.607 | 70.463 | 71.491 | 69.250 | 71.230 | 69.685 |

| 9 | 70.952 | 73.005 | 72.398 | 74.804 | 72.210 | 71.810 | 72.988 | 75.365 |

| 10 | 79.084 | 79.671 | 78.571 | 81.839 | 78.009 | 79.409 | 80.296 | 84.211 |